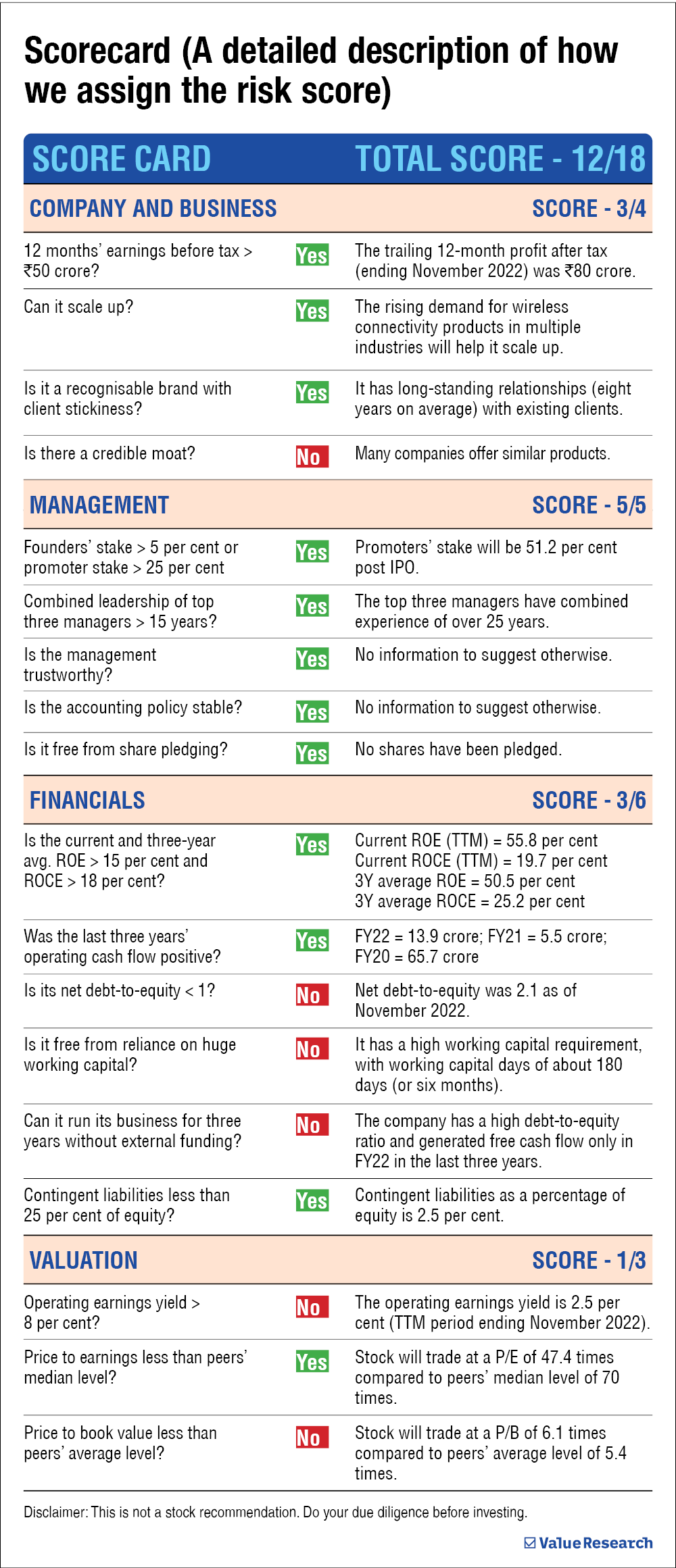

In a nutshell

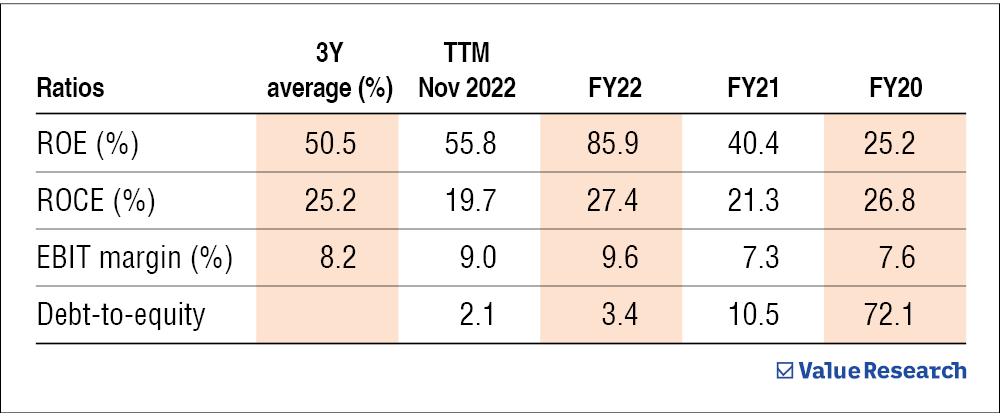

- Quality: Its three-year average ROE and ROCE are 50.5 and 25.2 per cent, respectively. It also commands a higher net profit margin than its peers and has maintained healthy operating cash flows in the past three years.

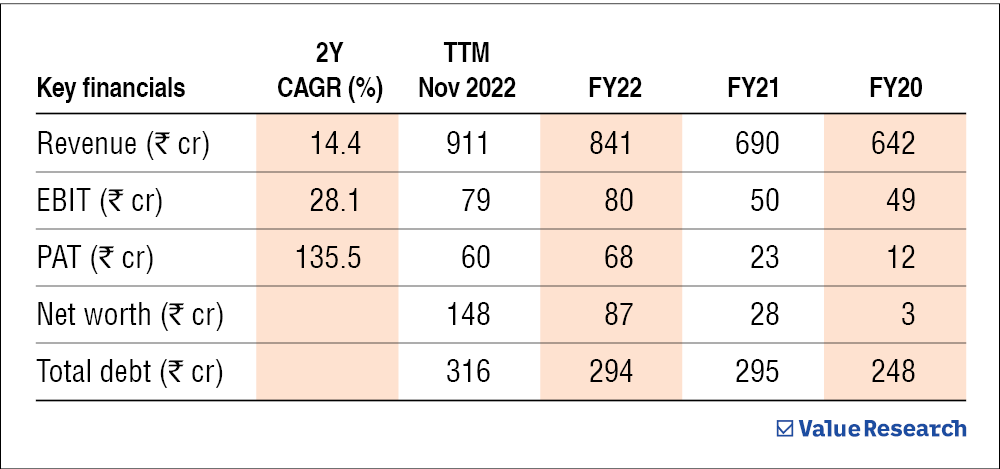

- Growth: In the last three years, Avalon Technologies grew its topline and PAT at 14 and 136 per cent per annum, respectively. Rising demand for wireless connectivity in various industries and higher per capita electronics consumption augurs well for its growth.

- Valuation: The stock will be priced relatively lower than its peers in terms of its P/E.

- Overview: Avalon Technologies stands to gain from the current digitisation trend and the rising demand for wireless connectivity in various industries. As 60 per cent of its revenue comes from its global operations, it is highly susceptible to macro factors.

About the company

Avalon Technologies provides electronic manufacturing services (EMS). It designs and manufactures electronic components and printed circuit boards (PCBs) used in the production of various electronic products. It primarily caters to clean energy, mobility, industrial, communication and medical industry.

Strengths

- Avalon Technologies has successfully maintained long-standing relationships (more than eight years) with its top clients accounting for 80 per cent of its revenue (as of the eight months ending November 2022).

- Only Indian EMS company with a full-fledged manufacturing facility in the USA.

Weaknesses

Its top five clients accounted for nearly 50 per cent of its revenue in FY22. If any of these clients decide to jump ship, it will significantly impact the company's financials.

Disclaimer: This is not a stock recommendation. Do your due diligence before investing.

Suggested read: Six parameters to look for in a company before investing

Ask Value Research ![]()