In simple terms, margins mean the amount of revenue a business can turn into profits. Suppose a business earns Rs 10,000 crore in revenue. But it has to spend around Rs 8,000 crore on operating expenses, interest payments, taxes, etc. That means, of that Rs 10,000 crore, it can count only Rs 2,000 crore as profits and has a margin of 20 per cent (Rs 2,000 / Rs 10,000).

So, high margins mean an efficient business, and low margins mean the business deserves the inefficient tag. Right?

Well, not quite so. Efficiency is important, and as an investor, you should be a stickler for both when picking your stocks. But margins are often dependent on industry dynamics. In some industries, low margins does not equate to a bad investment.

Take the example of the retail segment. Discount, sale, off, there's a reason retailers have these words plastered in front of their stores. Consumers will always flock to the retailer that sells a product at the lowest price.

So should a retailer lose business and sell products at a higher cost just to have the bragging rights for higher margins? Surely, that can't be a sign of a good business.

If you can generate more revenue consistently by lowering your margins and boosting your sales, does it really matter if you have low margins? At the end of the day, the lifeline of a business is consistent profits, not high margins.

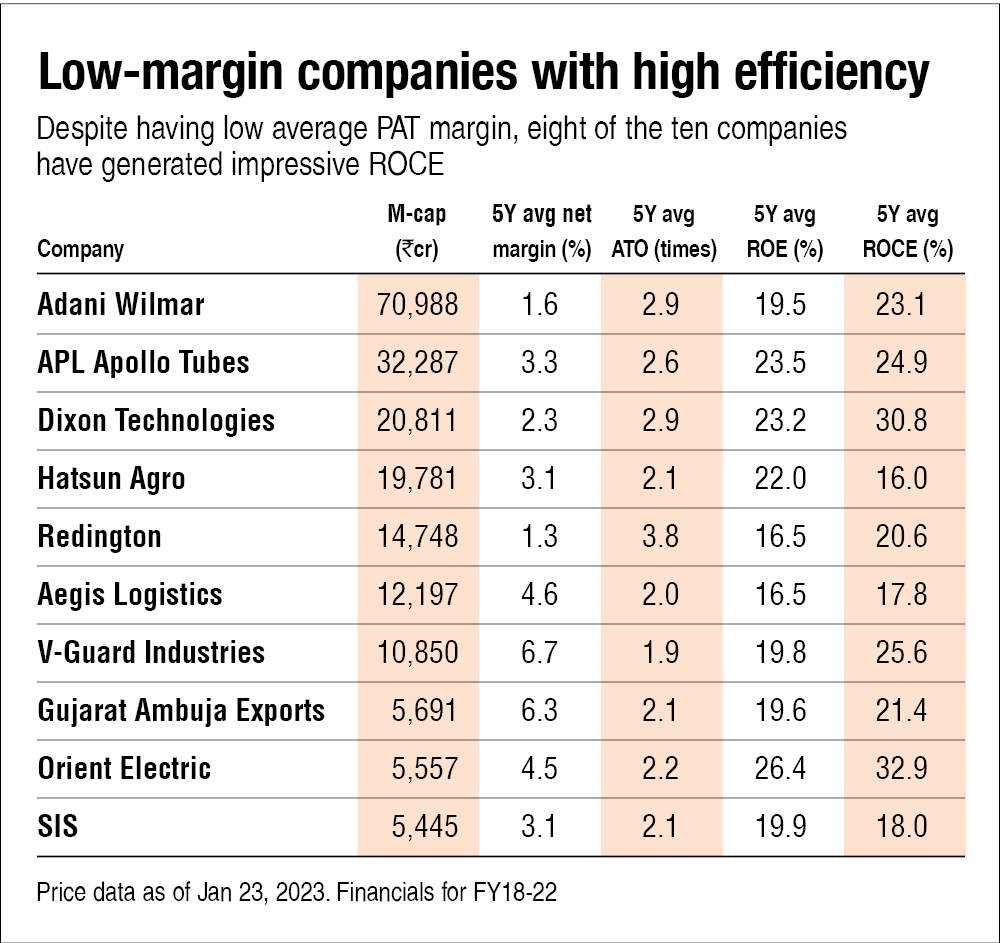

Walmart is an excellent example of this. Its five-year average net margin is just 2.2 per cent. But because it has a high average asset turnover of 2.4 times (ATO; the amount of revenue or sales a business generates using its assets) and high bargaining power over its suppliers, it was able to maintain a healthy ROE of 15.5 per cent.

Here are some other companies with low margins, high asset turnover, high ROE and ROCE.

Investors should note that we are not saying margins are not important. Efficiency and profitability should always go hand in hand. But judging a company solely on its margins is not advisable. As we have mentioned above, industry dynamics drive margins more than efficiency. In a segment like retail, where sales volume is far more important than high margins, margins should not be used to gauge efficiency and profitability. Similarly, other sector-specific factors, such as higher taxes imposed on certain segments, also play a key role in how much margin a business can sustain.

So next time you encounter a business with low margins, ask yourself these.

- What kind of a sector does the business operate in?

- Is it a sector that historically had low margins (such as retail)?

- Does it have a consistent record of efficiently using its assets to generate high revenue or sales ( high average asset turnover)?

- Does it have a history of generating wealth for its investors (high ROE and ROCE)?

If a business ticks all the above boxes, it may deserve a few more hours in your stock-picking exercise.

Suggested read: Don't invest solely based on P/E

This article was originally published on January 25, 2023.

Ask Value Research ![]()