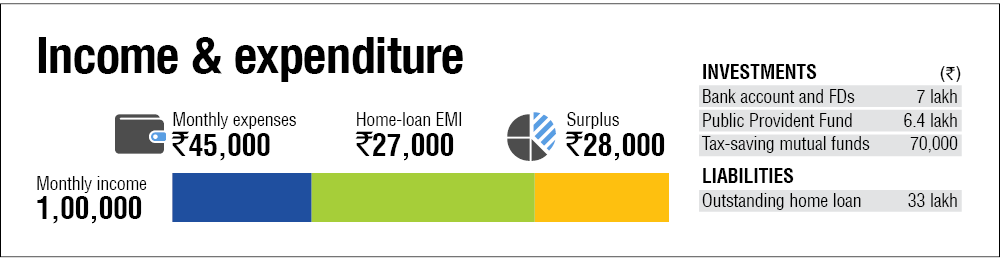

Paritosh (37) works for a pharmaceutical company. His in-hand monthly salary is close to Rs 1 lakh. He wants to start investing for his five-year-old daughter's higher education and his own retirement but is confused about whether this is the right time to start, given the ongoing economic uncertainty. He also wants to know if he should invest in equity or gold. He has a lump sum of Rs 2 lakh ready to be invested. Here is a plan for Paritosh.

Start investing now

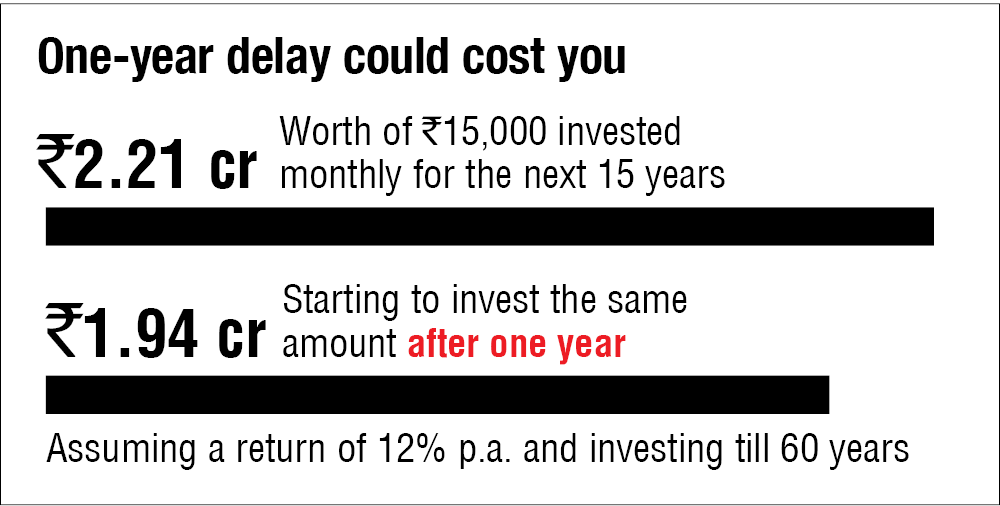

There is no good or bad time to start investing. What matters is that you choose the right investment avenue and invest systematically. It is essential to formulate a good financial plan and stick to it through thick and thin to achieve your financial goals. Market and economic uncertainties seldom go away. If one event is over, another arrives. Hence, don't focus on the short-term picture. Keep a long-term outlook. If you delay investing, that may result in opportunity loss, as illustrated below.

Don't think of gold as an investment

Gold rises whenever there is economic uncertainty, but it is not a productive asset. Its value is derived not from some economic fundamentals but from perception. See gold not as an investment but as a consumer good.

Still, if you must invest in gold, allocate not more than 5-10 per cent of your portfolio to it. To invest in gold, Sovereign Gold Bonds (SGBs) are the best option. On maturity, these bonds are redeemed for the prevailing gold prices and they also pay 2.5 per cent as interest during their holding period.

The right way to choose an investment avenue

Your choice of an investment avenue should be based on the time for which you want to invest the money, the purpose for which you are investing and your risk appetite. So, make sure that you define your goal first and then choose where to invest.

Equity funds are ideal if your goals are more than five years away. If your goals are three to five years away, then you should opt for short-duration debt funds. For short-term goals, those that are due in one-two years, opt for liquid funds or ultra short- duration funds.

Investing a lump sum

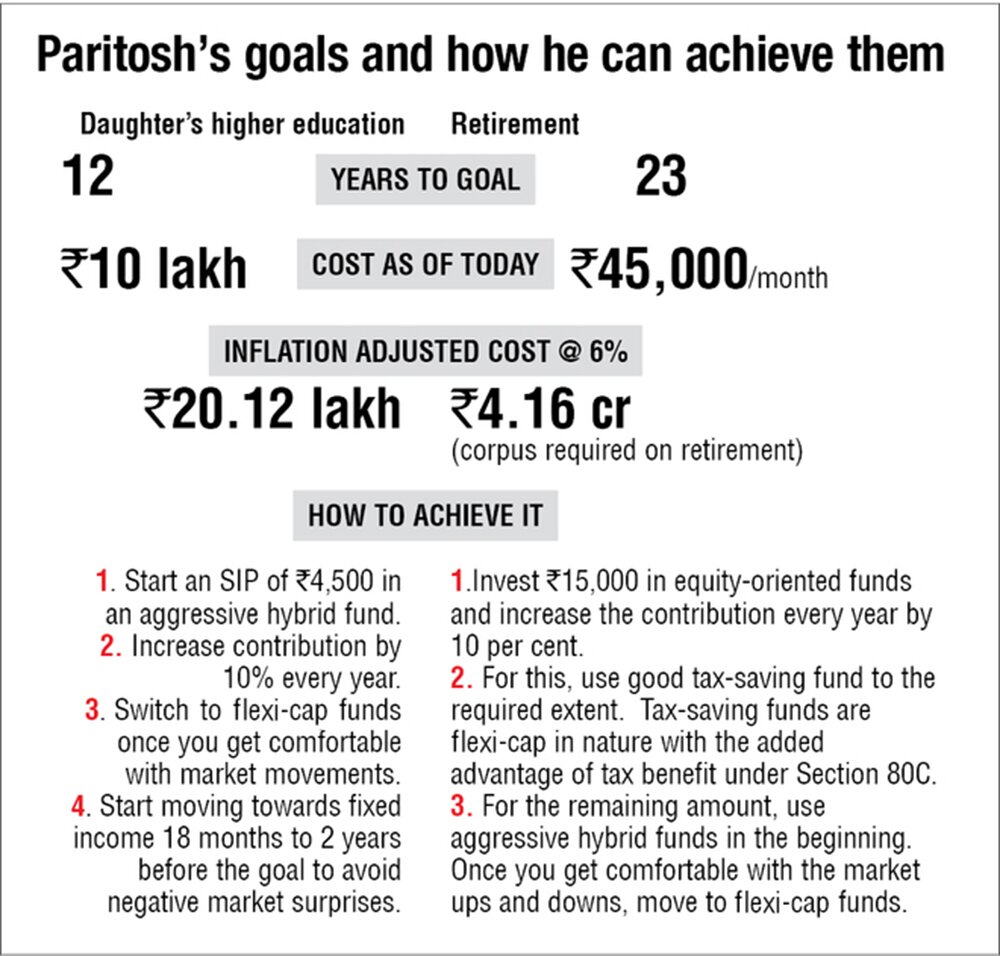

Paritosh has a lump sum of Rs 2 lakh which he wants to invest for his goals. Both his long-term goals - retirement and daughter's higher education - are at least 10 years away.

He should invest this amount in an aggressive hybrid fund. These funds are ideal for beginners as thanks to their debt exposure, they are less volatile than pure equity funds. Once he gets comfortable with market volatility, he can shift to flexi-cap funds.

However, this amount should not be invested at one go. Instead it should be spread over the next six months. Staggering the investment in equity reduces the risk of entering the market at the wrong level and helps you average your purchase cost.

Don't ignore these

- Emergency fund: Maintain an emergency fund equivalent to at least six months' expenses. It can be kept in a combination of liquid funds and a sweep-in fixed deposit. Given the ongoing crisis, a higher emergency fund than you would normally need is desirable.

- Life insurance: Buy adequate term life insurance to financially protect your loved ones in your absence. Ideally, the life cover should be at least 10-12 times of your annual income. Purchase it before you start investing for any other goal.

- Health insurance: An unforeseen medical emergency can derail your financial plan. Buy health insurance that adequately covers all your family members.

This article was originally published on December 22, 2021, and last updated on September 07, 2022.

Ask Value Research ![]()