These days, people are well aware of the importance of life insurance. Despite that, India still ranks among the countries with the lowest penetration rate in life insurance. According to the latest annual report of the Insurance Regulatory and Development Authority (IRDA), the penetration rate of life insurance in India is only 2.82 per cent.

With the growing popularity of various e-commerce platforms, it is now possible to buy a life-insurance policy directly from the company without any agent or broker, that too at the comfort of your home. Also, buying insurance policies online is a cost-effective option, with their premiums being 5 to 10 per cent lesser than those purchased through insurance agents. This is because the company saves on the commission. Besides, it is better to avoid the agent route, as most agents lure their customers to buy expensive products so that they can earn higher commissions. Even at the time of buying a policy online, you may receive calls from the company's marketing team as soon as you enter your contact details. But be careful and do not get swayed by their sales pitch.

Here we help you through a buyer's experience and the most important questions that you would encounter while buying a life-insurance policy online.

Choosing an insurance product

The simplest answer is to go with a pure term plan. While going through various products, you will come across many types of insurance policies, such as an endowment plan, a money-back plan, a unit-linked insurance policy (ULIP) and so on. Broadly, all insurance policies can be divided into two categories. In the first category, the insured receives some amount of money either during the policy term or at the end of the policy term. In the second category, the insured does not receive any money even on maturity. Only the nominee receives the sum assured on the death of the insured. This is what we call a pure term plan and indeed the cheapest form of a life cover. Term plans provide you with a good sum assured at a nominal cost.

Choosing an insurer

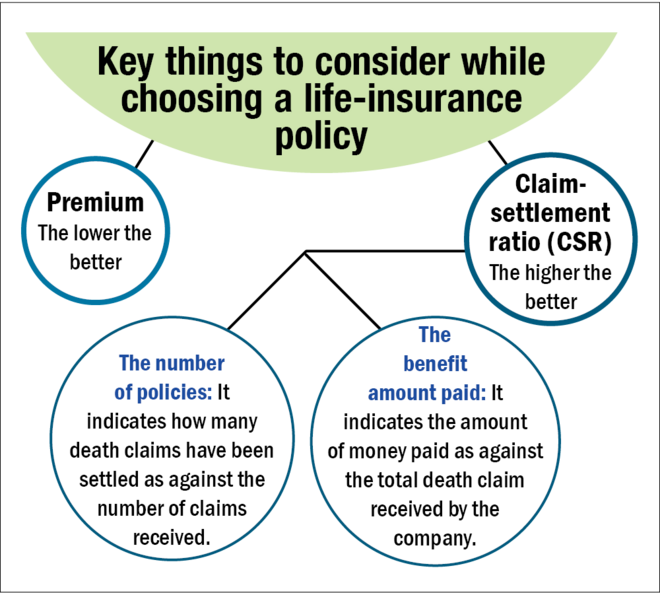

There are 24 life insurance companies in the market and it can be quite confusing to choose among them. To keep things simple, go by the following most important factors:

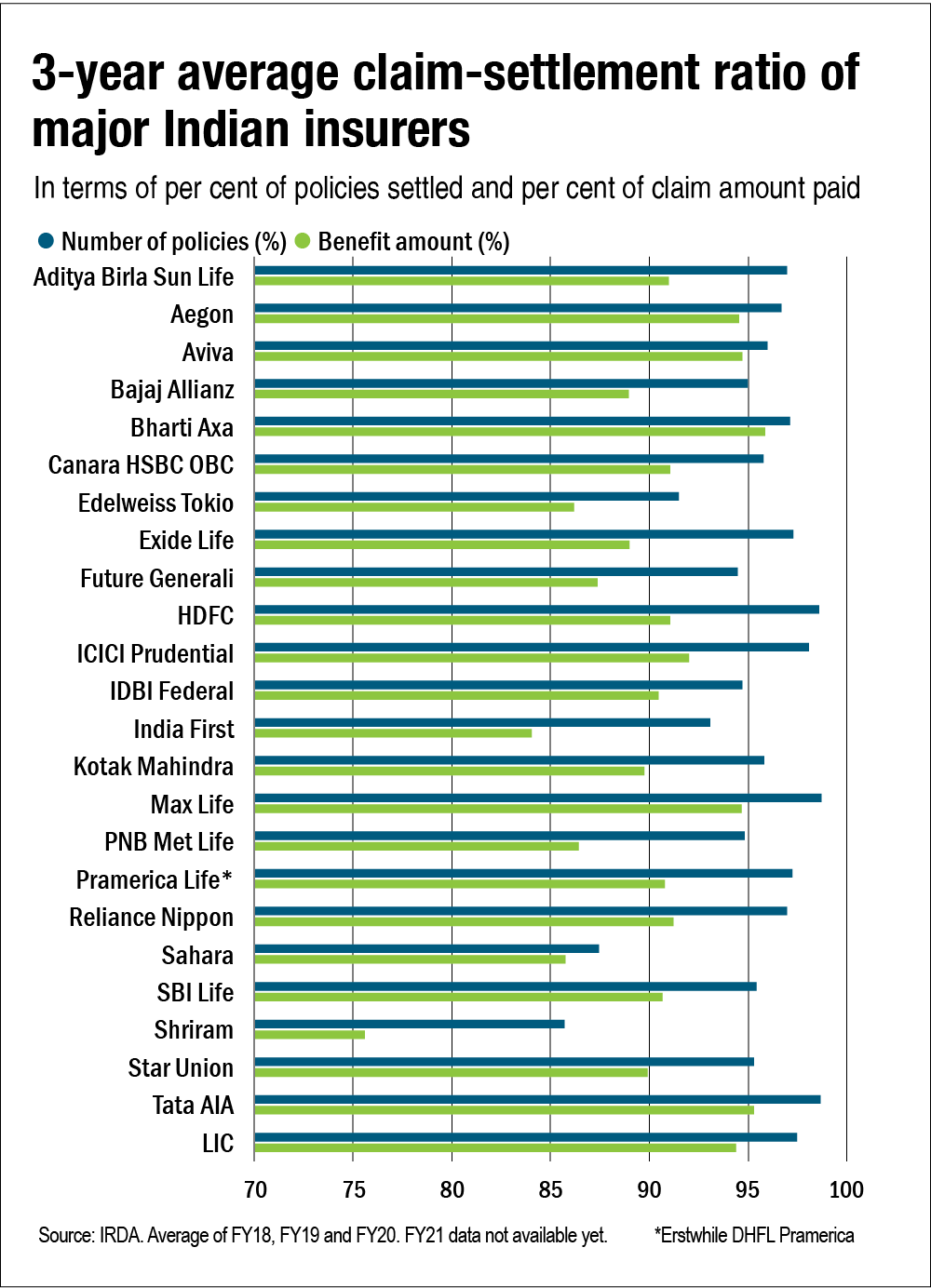

The CSR in terms of policy numbers indicates how many death claims have been honoured by the insurance company out of the total claims received. For example, a CSR of 95 per cent indicates that the insurance company settled 95 death claims out of 100 received by it during the relevant financial year. Likewise, a CSR in terms of benefit amount paid tells the total amount of money that has been paid by the insurance company as against the total claim received. For example, a CSR of 90 per cent indicates that Rs 90 has been paid against a death claim of `100. This can be a useful input to assess how the insurance company reacts when the death claim of a higher amount is made.

Although the websites of insurance companies and some aggregators mention the CSR in terms of the number of policies settled, they do not display the CSR in terms of the benefit amount paid. The easiest and the most trustworthy way to access this information is by visiting the 'annual reports' section on the website of the insurance regulator IRDA. Here, you will get the CSRs of all insurance companies on a historical basis.

The sum to be assured

Most insurance-company websites will pre-populate this on the basis of some algorithm. To calculate the ideal amount, multiply the annual expenses of your dependents by 20. Add to it any outstanding loans and the costs of any crucial financial goal for which your dependents may need money over and above the regular living expenses, for example, the costs of your children's higher education. Reduce the worth of your financial assets that you have already accumulated. Revisit the amount periodically.

The tenure of the policy

Most people prefer to run their life-insurance policy till their retirement age, i.e., till the time they plan to earn and financially contribute to the family. This need not necessarily be till the age of 60-65 years but can well be less than that for someone who plans to retire early, say at the age of 45.

Premium payment term

Most life-insurance companies would encourage you to fast-track the premium payments and would suggest a much shorter premium payment term than the policy term. However, in most cases, it is not recommended to do so. You lose the flexibility to change the insurer at a later date or to end the policy before the stipulated term. You may decide to end the policy much before the stipulated term if you have accumulated enough wealth or your need to have a life cover ceases. In that case, you can simply stop paying the annual premium and the policy would lapse. But if you fast-track your premium payments and pay all of them in advance, the insurance company would hardly refund it. Also, by paying the entire premium in one go, you forego your option to claim tax deduction under Section 80C in the subsequent years.

Rider or no rider

It is an add-on feature that can be added to the policy by paying a little extra premium. The two most common riders are the 'accidental-death-benefit rider' and the 'critical-illness rider'. The first rider doubles the sum assured only if the insured dies due to an accident. It is especially useful to someone who is in a travelling job. The critical-illness rider pays the insured a predefined lumpsum amount on the diagnosis of certain dreadful diseases like cancer, organ failure, etc. This can be a useful add-on. Think of a situation where the insured falls seriously ill and is unable to earn money because of it. The benefit under the life-insurance policy won't kick in, as the insured is still alive. In such a situation, getting some financial assistance through this rider can be quite helpful.

Lump-sum investments or monthly income?

Some insurance companies provide various payout options to choose from in the event of the insured's death. These options range from a one-time lump-sum payout to a staggered monthly income and even a combination of both. Unless you are extremely unsure about the money-management skills of the nominee, it is better to go for the traditional lump-sum payout option. Even RBI's floating-rate bond, which is almost risk-free, fetches 7.15 per cent a year. This translates into a monthly return of close to Rs 60,000 on a deposit of Rs 1 crore. Someone with basic money-management skills may be able to earn much more by investing the lump-sum amount in comparison to the benefit passed on by the insurance company on choosing a staggered payout option.

Married Women's Property (MWP) Act

In some cases, the insurance company may ask whether you want to purchase the life-insurance policy under the MWP Act. If you tick the check box, the insurance money can be utilised only by the wife or the children. Such policies cannot be attached to a court case or to any liability of the deceased. However, one nuance that you need to be aware of is that the nominee under such a policy cannot be changed at a later date, even in the subsequent case of a divorce.

Besides, some other questions asked by the insurance company would mostly pertain to your lifestyle habits and medical history. There could be a temptation to give a false answer in order to get a lower premium. But you should be absolutely truthful in answering them. This is because any misrepresentation here may lead to a claim rejection in the future, thereby putting the future of your loved ones at risk.

This article was originally published on October 14, 2021.

Ask Value Research ![]()