Adobe Stock

Adobe Stock

Summary: India’s defence sector has a powerful long-term growth story driven by rising military spending, import substitution and export ambitions, but picking the right defence stock is far harder than the sector narrative suggests. We check why a broader index-based approach may be a more effective way to participate in a sector where execution, timing and policy shifts can dramatically reshape winners and losers.

Every few years, a sector comes along where the big picture is so obvious and well-supported by data and policy that investors feel a rare sense of certainty. Indian defence is one such sector today and for good reason.

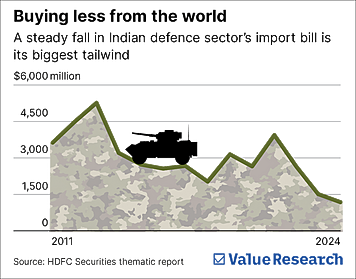

The sector’s budget allocation for FY27 is Rs 7.8 lakh crore, up 15 per cent from last year and making up for nearly 15 per cent of the Union Budget. Of this, around Rs 2.2 lakh crore has been set aside for capital expenditure: fighter aircraft, submarines, drones, missiles and radar systems. The government has also imposed a phased import embargo on over 1,000 weapon and platform categories, pushing the armed forces to buy domestically what they previously imported.

Defence exports, once negligible, have surged 34-fold since FY14, from Rs 700 crore to Rs 23,400 crore in FY25. The target is Rs 50,000 crore by FY29 as military expenditure worldwide rises sharply amid global wars, Europe’s rearmament and an accelerating US-China rivalry.

India, now the world’s fourth-largest defence spender, sits at the centre of this transformation. And a few sectors have such a long structural case for investors today.

The natural next step is finding the right companies, buying them and waiting. But that next step is harder than it looks.

The problem with picking defence stocks

Defence is one of the most execution-dependent sectors in any economy. Orders are awarded years before revenue is recognised. Production timelines slip. Technology programmes get redesigned mid-course. A company can carry an order book worth several times its annual revenues, as Hindustan Aeronautics currently does, and still deliver earnings growth that disappoints. Converting orders into deliveries and deliveries into cash is where defence companies most frequently stumble. Meanwhile, valuations across the sector already reflect years of future growth, leaving investors little margin for error when execution lags.

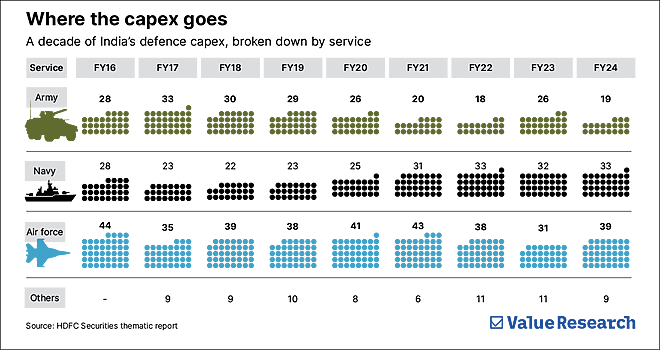

The sector’s complexity compounds this. India’s defence value chain spans integrators building complete platforms, electronics companies supplying subsystems, private-sector manufacturers of components and ordnance and a fast-expanding ecosystem of startups developing drones, avionics and electronic warfare systems. Each segment has different revenue drivers, margin profiles and execution risks. A company perfectly positioned in one spending cycle, say naval shipbuilding, may be entirely bypassed in the next as spending pivots to air power or space.

This is the dilemma that defence investing presents. You can be completely right about the sector and still be wrong about your portfolio because you backed the wrong company, or the right company at the wrong valuation, or misjudged the pace at which a particular order would translate into earnings. The sector story is sound. The stock-picking problem is real.

A better way to own the story

This is precisely the problem that the Nifty India Defence Index addresses. It holds a basket of listed companies with meaningful defence revenues from large PSUs like Bharat Electronics and Hindustan Aeronautics to private-sector names across the value chain. Rather than concentrating risk in a handful of names, it spreads exposure across the sector.

And its construction is self-correcting: companies are weighted by market capitalisation, so a business that executes well sees its weight rise automatically. One that stumbles sees its weight shrink as the market prices in disappointment. Performance is rewarded and poor execution is penalised, not by a fund manager’s judgment but by the market’s.

Index funds and ETFs that track this index give investors a straightforward way to own it. Both hold the same underlying basket. An ETF trades on the exchange like a share; an index fund is bought at end-of-day NAV and works well for SIP investors. The choice between them is mostly one of convenience. What investors should pay attention to is tracking error and expense ratio, which directly determine how faithfully their returns mirror the index.

The self-correcting mechanism does work with a lag. A heavyweight going through a rough patch will drag the index until its weight falls to reflect its diminished standing. This means real pain for investors before the logic reasserts itself. But for anyone whose conviction is at the sector level, which in a domain this technically complex and policy-driven describes most investors, this remains the structurally sounder approach than stock-picking.

What you will be signing up for

Owning this index is not owning a safe bet. It is still a one-sector concentrated bet. And the sector has already had an extraordinary run, with several defence stocks delivering multibagger returns over the past three to four years. Valuations reflect significant optimism about future order execution. A budget disappointment, a procurement delay, or a broader market correction could compress the index sharply and a tracking fund will participate fully in any such decline.

What the index offers is the cleanest possible exposure to a genuine, multi-decade opportunity: the transformation of India from the world’s largest arms importer into a credible domestic manufacturer and eventually, a meaningful exporter. The policy framework is in place. The order pipeline is real. Which companies will benefit most is not fully clear yet and some that look obvious today may disappoint. But the index does not require you to know which is which. It asks only that you believe in the sector and let the market work out the rest.

This article was originally published on June 01, 2026.

Ask Value Research ![]()