Vinayak Pathak/AI-Generated Image

Vinayak Pathak/AI-Generated Image

Summary: India is in the midst of the most sustained infrastructure buildout in its history, and investors are pouring into infra-themed funds to get a stake in it. But two indices promise the same ‘infrastructure exposure’ while being built on sharply different logic. A look at why the choice between them is itself an investment decision.

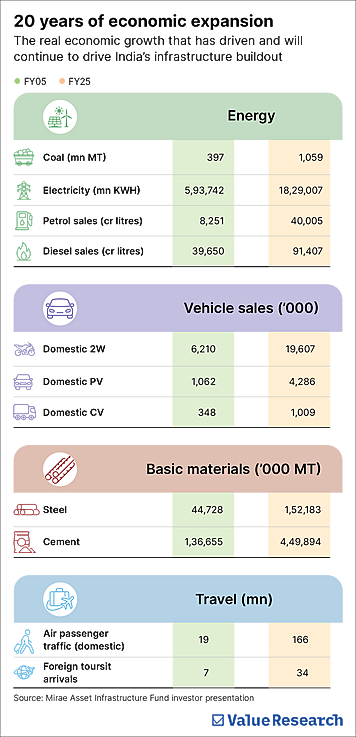

India is in the midst of the most sustained infrastructure buildout in its history. Expressways that did not exist five years ago. Power transmission towers spreading across landscapes that sat dark a decade ago. Ports that cut turnaround times from more than a week to just a few days.

The numbers bear it out: combined central and state government capital expenditure has climbed from just 3.9 per cent of GDP in FY19 to 6.1 per cent in FY25. So who benefits most directly from this boom? The listed infrastructure space and investors seeking a stake in India’s next phase of growth have been pouring into infrastructure-themed investments in steadily increasing numbers.

The indices tracking India’s infra story

ETFs and index funds in India track two main infrastructure indices: the Nifty Infrastructure Index and the Nifty India Infrastructure & Logistics Index. Both promise ‘infrastructure exposure’, but their construction differs sharply.

The Nifty Infrastructure Index, the older of the two, holds 30 stocks. Its top 10 holdings account for 70 per cent of the index, with the single largest carrying a 17 per cent weight and the next two adding another 28 per cent between them. In effect, just three companies decide nearly half the outcome of an investment made in the name of India’s entire infrastructure story.

The Nifty India Infrastructure & Logistics Index is built on a different logic. It comprises 100 stocks drawn from the Nifty 500. No single stock may exceed 5 per cent of the index by free-float market capitalisation, and no single industry may exceed 20 per cent. Its top 10 stocks together account for 41 per cent, less than the weight that just three stocks command in the Nifty Infrastructure Index.

It also spans the entire infrastructure value chain in a way its peers do not. At the top sit large-cap anchors such as NTPC, Larsen & Toubro, Bharti Airtel, Bharat Electronics, UltraTech Cement and Power Grid Corporation, businesses with established earnings, strong balance sheets and direct exposure to the largest government programmes.

Alongside, the index holds mid- and small-cap companies in their expansion phase, riding specific sub-themes such as naval shipbuilding, power equipment exports and renewable energy infrastructure.

In 2024, India’s logistics market was valued at $228 billion and is expected to grow at 6.5 per cent annually through 2033. A highway creates value only when goods move efficiently along it. A port earns returns only when supply chains connect it seamlessly to factories and consumers. By including logistics, this index lets the investor participate not just in the building of infrastructure but in its monetisation, a distinction other infrastructure indices miss entirely.

The concentration problem

When an investor invests in the Nifty Infrastructure Index, they are placing a 17 per cent bet on a single conglomerate and hoping it outperforms. Should that company have a bad year, whether from a regulatory development, a business-specific setback or simply a valuation correction, the index feels it sharply, no matter what is happening in railways, renewable energy or logistics.

The Nifty India Infrastructure & Logistics Index caps that risk by design. Large caps make up 61.2 per cent of the portfolio, providing stability and earnings predictability. Mid caps, at 26.3 per cent, supply the growth engine, while small caps, at 12.5 per cent, offer exposure to the emerging names that will become tomorrow’s mid caps. The balance is deliberate, and it mirrors what India’s infrastructure ecosystem actually looks like.

The risks you should be mindful of

A less concentrated index does not make infrastructure investing risk-free. The sector still leans heavily on government spending, so any fiscal consolidation, budget reallocation or slowdown in tendering activity would be felt across the index. Private capital, expected to complement public spending, has yet to materialise as anticipated.

Valuations across infra stocks have also re-rated significantly after years of strong returns. The cement, capital goods and power equipment segments in particular continue to trade well above their historical averages. Such levels embed considerable optimism about future earnings, and infrastructure companies have a long record of delivering on eventual demand while disappointing on timelines.

Before you invest

India’s infrastructure growth story will play out over decades, not quarters. The direction, then, is not in question. What remains is which index to track in order to capitalise on that growth. That choice deserves the same deliberate attention active investors give to stock selection, because in a sector this broad, where time and patience are rewarded, getting the index right is itself an investment decision.

This article was originally published on July 01, 2026.

Ask Value Research ![]()