Vinayak Pathak/AI-Generated Image

Vinayak Pathak/AI-Generated Image

Summary: FMCG has long been the default choice for investors who want low volatility, reliable dividends and brands India has trusted for decades. But over the past decade, that comfort has carried a steep, measurable cost. A look at what an FMCG index investor has actually given up and why it isn't a blip.

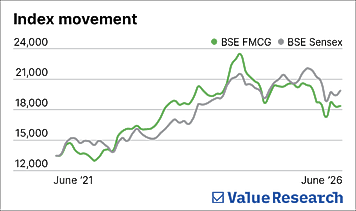

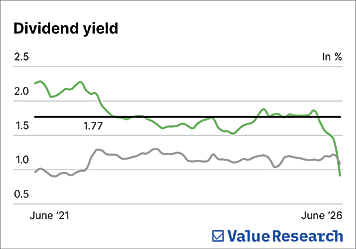

Among Indian equity indices, few have the reputation of the BSE FMCG index. With reliable cash flows, consistent dividends and brands that Indian households have trusted for decades, the sector has long been the default choice for investors seeking equities with relatively low volatility. The problem is that over the past decade, this comfort has come at a steep cost.

Even after including dividends, the BSE FMCG TRI has returned about 10 per cent per annum over the last ten years. The BSE 500 TRI returned 14 per cent over the same period. The Sensex TRI returned 12 per cent. That is a gap of four percentage points every year relative to the broader market. The five-year picture tells a similar story. This is not a blip. It is a structural trend.

A sector that grew up

FMCG’s early promise was well-founded. A generation ago, penetration of everyday goods across India (soaps, shampoos, biscuits, packaged foods) was genuinely low. Strong brands had enormous, underpenetrated markets ahead of them. Volume growth came easily, and earnings reflected that.

Today, that story is largely over. Penetration in most categories is close to saturation. What remains is mostly replacement demand: consumers buying the same products they have always bought. Future growth ties largely to population growth and a gradual rise in incomes among lower-income households. Neither can replicate the volume expansion that once defined FMCG earnings. The urgency with which these companies are diversifying into new verticals, such as health supplements, premium categories, direct-to-consumer channels, signals how limited organic growth has become, not a sign of renewed ambition.

Valuations that took time to adjust

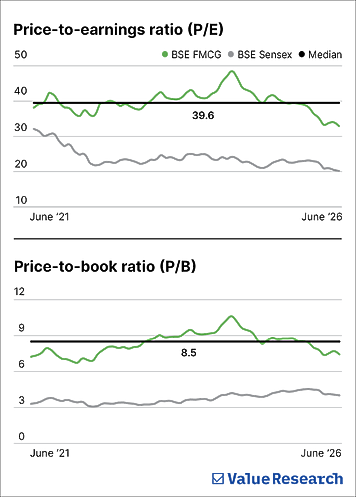

Growth expectations fell, but valuations did not follow at the same pace. Investors continued to pay for stability long after the high growth that once justified that premium had faded. At their peak, FMCG companies traded at around 43 times earnings. The P/E of the BSE FMCG index now stands at around 33 times.

That is meaningful compression. But it still raises a question: Is 33 times earnings the right price for a sector whose earnings growth is now in the low-to-mid double digits? The businesses themselves remain formidable. FMCG’s large companies generate free cash flow that rivals the market capitalisation of several mid-cap peers. The concern is not business quality; it is whether the valuation still reflects a growth story that has largely played out.

The honest trade off

The FMCG index offers something real: stable income, low volatility and reliable dividends. What it has not offered, at least over the past decade, is returns that keep pace with the broader market.

For an index investor, the question is simple. If stability and income are the goal, the FMCG index is built for that. If the goal is capital appreciation in line with, or ahead of the broader market, the evidence of the last 10 years says otherwise. No index is inherently wrong. But every index has a price. In FMCG’s case, the price of stability has been returns.

This article was originally published on July 01, 2026.

Ask Value Research ![]()