Aprajita Anushree/AI-Generated Image

Aprajita Anushree/AI-Generated Image

Summary: You own a Nifty 50 fund, a Nifty 500 fund and a Nifty Total Market fund. That feels like diversification across 50, 500 and 750 stocks. Most of your money is in the same companies in all three. The breadth is real. The diversification isn't.

Passive investing has earned its stripes. It is simple, low cost and free of worries about fund manager discretion. You simply buy the index, stay invested and let the market do its job.

But there is a big problem investors building passive portfolios tend to overlook. As more index funds become available, many assume that owning more of them automatically means better diversification. That feels sensible at first. A Nifty 50 fund gives you 50 stocks. A Nifty 500 fund gives you 500. A Nifty Total Market fund gives you 750. So adding them together should spread your money wider. That, however, is not the case. Even though these broad indices substantially differ in the number of their holdings, they still suffer from a serious overlap that makes them more similar than different. Here’s how:

Bigger indices, same anchors

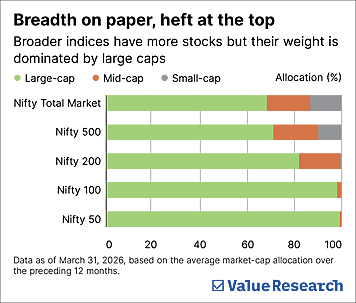

Due to being weighted by market capitalisation, most broad indices end up being heavily tilted towards large-cap stocks. On a market-cap weightage basis, the bigger the company is, the larger the weight it takes in an index. So in any broad market index, the larger stocks have bigger weightage and thus bigger influence on its performance. This is why the Nifty 200, despite having 100 mid-cap stocks, had an average large-cap weightage of 82 per cent in the 12 months through March 2026.

Even the Nifty 500 and the Nifty Total Market indices, which majorly include mid- and small-cap stocks, remain largely influenced by the top 100 companies with large caps making up the bulk of their weight. See chart: Breadth on paper, heft at the top. So even though the number of stocks increases as you go broader, most of your money, in effect, still gets invested in the same large companies.

The diversification mirage

If broad indices are all tilted towards the same large companies, owning a variety of them does not diversify your portfolio. It simply duplicates it.

Consider an investor holding both the Nifty 200 and the Nifty Total Market index. At first glance, this seems reasonable. The Total Market index has 750 stocks, so this means there are 550 stocks that are not in the Nifty 200.

But these extra stocks carry very little weight. The Total Market index still derives about 83 per cent of its weight from the same 200 stocks already covered by the Nifty 200. In other words, there is an 83 per cent overlap between the two. So the investor has two indices without any meaningfully different exposure. It is the same portfolio with a thin layer of extras. This pattern shows up across all other combinations, too. The indices change. The underlying exposure barely does. See chart: Overlap in disguise.

The return gap stays narrow

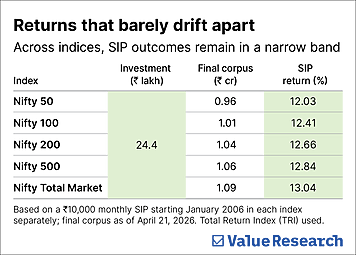

One could still argue that even a small non-overlapping portion may improve returns over time. So that was tested next. Assume a monthly SIP of Rs 10,000 starting in January 2006, invested separately in each of the broad indices and tracked until April 21, 2026. The results are unsurprising.

The Nifty 50 delivered an annual SIP return (calculated as XIRR) of 12.03 per cent. The Nifty 100, Nifty 200, Nifty 500 and Nifty Total Market clustered in a narrow range above that. The difference between most of them was less than one percentage point. So the number of stocks increased sharply, but the return experience did not. See chart: Returns that barely drift apart.

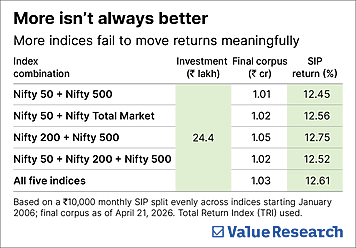

The same pattern holds when indices are combined. A 50:50 split between the Nifty 50 and the Nifty Total Market, the pair with the lowest overlap among those tested at 57 per cent, delivered 12.56 per cent. That is just about 0.5 percentage point higher than the Nifty 50 alone. Even combining all five indices produced a return of 12.61 per cent per annum, not materially different from any other set. So adding more of these indices still gives almost the same outcome. See chart: More isn’t always better.

What should you do then?

Start by having clarity on what you want to achieve before picking funds. If you want a simple, low-risk passive portfolio, a single large-cap index fund can be enough. If you want one fund with broader market exposure, a Nifty 500 index fund is a good option. It will be large-cap heavy but still offer decent exposure to mid- and small caps in a single place.

But if you want meaningful diversification beyond large caps, consider equal-weight indices instead of market-cap weighted ones. They spread money more evenly across stocks. The Nifty 500 Equal Weight index, for instance, has roughly 20 per cent weight in large caps, 30 per cent in mid caps and nearly 50 per cent in small caps. Pairing it with the Nifty 50 brings the overlap down to around 10 per cent from 59 per cent when paired with the market-cap weighted Nifty 500.

This is the true test. Not how many index funds you own, but how much of your portfolio they actually change. If the answer is very little, you have not diversified. Every index fund, therefore, must earn its place in your portfolio. If it does not bring fresh exposure, it does not belong there.

This article was originally published on May 20, 2026.

Ask Value Research ![]()