Yogesh Sharma/AI-generated image

Yogesh Sharma/AI-generated image

Summary: Pharma has outperformed the broader market by nearly 15 percentage points over the past year. The defensive demand story gets the credit. The rupee's 10 per cent slide against the dollar deserves more of it. And understanding that distinction changes how you think about what you're actually buying.

When the broader market is under the weather, the Nifty Pharma index tends to be healthier. Take the last one year (as of June 1, 2026), during which the Nifty 500 TRI gave a paltry -0.7 per cent while the Nifty Pharma TRI was up nearly 14 per cent. Part of the reason is defensive demand: people may postpone buying a new phone or taking a foreign trip, but not their medicines. But the bigger reason boosting the sector is the weakening rupee. The last one-year outperformance coincides with the rupee depreciating by roughly 10 per cent against the US dollar.

Why weak rupee is good news

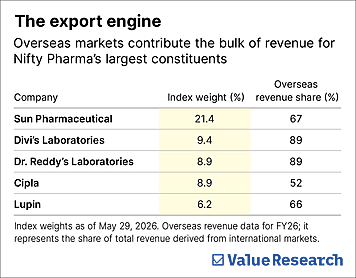

A weak rupee is a shot in the arm for India’s pharma industry, where most heavyweights collect the bulk of revenue from outside India. If a firm books most of its sales in US dollars and the dollar strengthens, those same dollars convert into more rupees, and reported income gets a lift. The reverse is true for businesses that import most of their raw materials, since their bills go up. For the export-heavy pharma pack, currency weakness usually lands on the right side of the ledger and lifts returns as well. This has held over its long history in the market.

The currency lift in the past

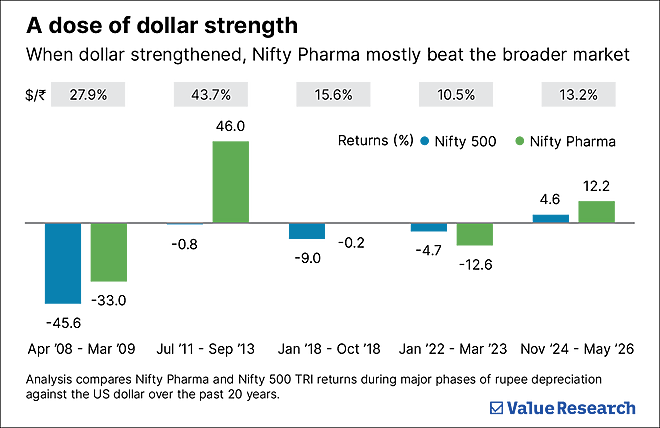

In four out of five periods, when the dollar sharply appreciated against the rupee during the past 20 years, the pharma index decisively outperformed the Nifty 500.

The long stretch from July 2011 to September 2013 stands out when the dollar climbed nearly 44 per cent against the rupee. The Nifty 500 limped to a -0.8 per cent over that period, while the pharma index delivered a striking 46 per cent. The other phases were comparatively less dramatic but told a similar story.

A sharp fall in the rupee, thus, tends to flatter pharma’s books for a few quarters and burnish its defensive reputation at the same time, a neat combination. But no health check is complete on short-term vitals alone. Let’s look at the long-term record.

The long-term diagnosis

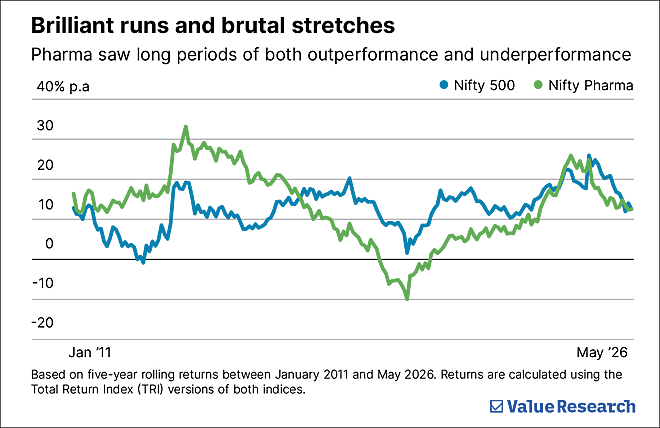

Of all five-year rolling periods over the last 15 years, the pharma index has beaten the Nifty 500 in 46 per cent of them. The Nifty 500 came out on top the other 54 per cent of the time. There’s not a dominant one-way winner of the two over long periods. The broader market, though, has mostly remained ahead.

The pharma index still has given 13.1 per cent annually on average when held for five years, slightly ahead of the Nifty 500’s 12.7 per cent.

How can an index that outperforms less often still deliver a higher average return? The answer is in where most of its returns lie.

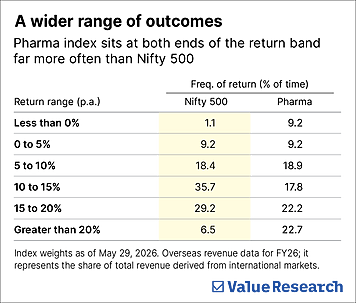

The pharma index has a habit of going to extremes. It gave 20 per cent-plus returns far more often than the Nifty 500 did. The broad index, meanwhile, has clustered in the 10 to 15 per cent return range, roughly twice as often as pharma. The pharma index also gave losses more frequently in 9 per cent of periods against just 1 per cent for the Nifty 500.

In short, the pharma index’s returns show up at both ends with far more chances of both losses and sharp gains than the broader market. That is the signature of higher volatility, and the standard deviation confirms it: 9.2 per cent for the pharma index versus 5.3 per cent for the Nifty 500 on average over five-year rolling periods.

Prescription for investors

When rupee weakens against the dollar, pharma companies tend to benefit as overseas earnings translate into more rupees. Combined with the sector’s defensive appeal, this can fuel strong runs, much like the one we are seeing now.

But our data makes the limits of this trade clear. The pharma index has gone through prolonged periods of underperformance and has, in fact, lagged the broad market more often than it has beaten it. Its higher average return came not from steady outperformance but from occasional sharp bursts, paired with losses that the Nifty 500 almost never delivered. Entry timing, therefore, matters enormously, and predicting currency moves consistently is easier said than done.

Sectoral indices are best treated as satellite holdings rather than the foundation of a portfolio.

The core is better served by a diversified index or fund that does not depend on one sector staying in favour or one currency moving in the right direction.

This article was originally published on June 20, 2026.

Ask Value Research ![]()