Anand Kumar/AI-Generated Image

Anand Kumar/AI-Generated Image

Summary: PSU stocks have made a remarkable comeback, but not every way of investing in them is the same. Here's how the four passive options differ, and what investors should know before picking one.

PSU stocks spent much of the last decade under investors' radar, trailing the broader market. That changed in 2021, when the sector staged a sharp rally. Since then, PSU stocks have consistently delivered positive returns, making them difficult for the market to ignore.

For investors looking to capture this theme passively, there are four options: the Nifty CPSE, Bharat 22, Nifty PSE and BSE PSU indices. While they may appear to offer similar exposure, each slices the public-sector universe differently, ranging from a concentrated 11-stock basket to a broad 60-stock index.

The four routes to PSUs

The different ways by which passive investors can ride the PSU wave

| Index | Number of funds tracking the index (including ETFs & FoFs) | Total AUM (Rs cr) | Average expense ratio (%) |

|---|---|---|---|

| Nifty CPSE | 1 | 20,959 | 0.07 |

| BSE Bharat 22 | 2 | 13,370 | 0.10 |

| BSE PSU | 1 | 85 | 0.48 |

| Nifty PSE | 4 | 52 | 0.38 |

| AUM and expense ratio data as of May 2026 | |||

Before deciding which index to choose, it is important to understand its composition that is, what it actually owns.

What's under the hood?

The four indices vary widely in the number of stocks and concentration

| Index | Which companies does the index track? | Number of companies | Median market cap | Top 5 stocks weight (%) | Top three sectors |

|---|---|---|---|---|---|

| Nifty CPSE | Central public sector enterprises (CPSEs); created to support the Government's CPSE ETF disinvestment programme | 11 | 79,175 | 86.6 | Energy & Utilities (62.7%), Industrials (22.8%), Materials (14.6%) |

| BSE Bharat 22 | 22 companies included in the Government's Bharat 22 disinvestment programme | 22 | 1,40,143 | 56.9 | Energy & Utilities (34.4%), Industrials (20.6%), Financial (19.2%) |

| BSE PSU | Listed public sector undertakings (PSUs) | 60 | 64,016 | 44.9 | Financial (37.3%), Energy & Utilities (33%), Industrials (18.6%) |

| Nifty PSE | Public sector enterprises with majority government ownership | 20 | 1,28,277 | 51.9 | Energy & Utilities (52.8%), Industrials (26.6%), Materials (10.7%) |

| Source: Respective factsheets as of June 2026. Market-cap data as of May 2026. Sectors as per Value Research classification. | |||||

The table highlights how differently these indices are constructed. While the Nifty CPSE tracks just 11 stocks, the BSE PSU holds 60.

The Nifty CPSE is also by far the most concentrated. Its top five holdings account for 86.6 per cent of the index, while energy and utilities alone make up 62.7 per cent. All four indices have a heavy tilt towards energy, utilities and industrials. Only the broader BSE PSU and Bharat 22 indices have a meaningful allocation to financials.

One important distinction is that Bharat 22 is not a pure PSU index. Alongside public-sector companies, it also holds three private-sector names: Axis Bank, ITC and Larsen & Toubro, which came into government ownership through SUUTI, the entity that inherited the erstwhile Unit Trust of India portfolio. Their combined weight is far from insignificant, standing at 36.8 per cent as of May 2026, and averaging around 39.2 per cent since the launch of the index fund. Investors using Bharat 22 as a proxy for PSUs should therefore recognise that a substantial part of the portfolio is invested outside the PSU universe.

Despite these differences, the four indices are far from independent portfolios. Their average portfolio overlap, shown below, makes that clear.

Different names, similar portfolios

The four PSU indices have a high portfolio overlap among them

| Index | Nifty CPSE | Nifty PSE | BSE Bharat 22 | BSE PSU |

|---|---|---|---|---|

| Nifty CPSE | - | 54.5 | 35.4 | 34.8 |

| Nifty PSE | 54.5 | - | 45.6 | 59.4 |

| BSE Bharat 22 | 35.4 | 45.6 | - | 53.0 |

| BSE PSU | 34.8 | 59.4 | 53.0 | - |

| Average overlap computed using portfolio holdings at six-month intervals from May 2024 to May 2026 | ||||

The overlap is substantial, ranging from 34.8 per cent to as high as 59.4 per cent. Put simply, whichever route investors choose, they are likely to end up owning many of the same stocks.

But has this high overlap translated into similar performance? Let's find out.

Recent returns remain impressive

On a trailing five-year basis (as of July 8, 2026), the four indices delivered annualised returns of roughly 20 to 26.5 per cent, with the Nifty CPSE leading the pack. By comparison, the Nifty 500 returned 11.2 per cent annualised over the same period, making the outperformance difficult to ignore.

Those eye-catching numbers, however, tell only part of the story. Most of the outperformance is surprisingly recent.

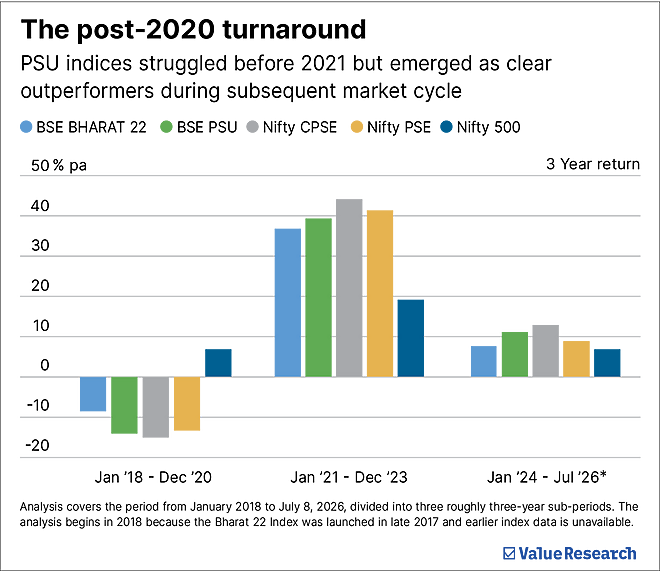

PSU stocks did most of their heavy lifting after 2020. The chart below compares the PSU indices with the broader Nifty 500 from January 2018 to June 2026, split into three roughly three-year periods. The analysis begins in 2018 because the Bharat 22 Index was launched only in late 2017, making earlier data unavailable.

Analysis covers the period from January 2018 to July 8, 2026, divided into three roughly three-year sub-periods. The analysis begins in 2018 because the Bharat 22 Index was launched in late 2017 and earlier index data is unavailable.

From January 2018 to December 2020, PSU indices lagged the Nifty 500. They then reversed course, delivering strong outperformance from January 2021 to December 2023 and maintaining that lead thereafter.

Several factors are commonly credited with this post-2020 revival: rock-bottom starting valuations after years of underperformance that left room for a sharp re-rating; the government's capex and infrastructure push, which boosted PSU order books; sustained balance-sheet repair and deleveraging across large PSU companies; generous dividend payouts that attracted income-seeking investors; and renewed optimism around disinvestment and value unlocking.

The long game paints a lukewarm picture

Stretch the time horizon, however, and the picture becomes less flattering. Looking at five-year rolling returns from 2011 to 2026 shows how these indices have behaved across complete market cycles rather than during a single favourable phase. Bharat 22 is excluded because its history begins only in late 2017, but the remaining three indices are sufficient to capture the broader PSU theme.

The long-term story looks sombre

Five-year return distribution shows PSU indices lagging the broader market and posting negative returns far more often

| Return range (% p.a.) | Nifty CPSE | BSE PSU | Nifty PSE | Nifty 500 |

|---|---|---|---|---|

| Less than 0 | 23.8 | 37.0 | 33.7 | 1.7 |

| 0 to 5 | 22.7 | 35.9 | 28.7 | 12.2 |

| 5 to 10 | 22.7 | 7.2 | 17.7 | 21.5 |

| 10 to 15 | 12.2 | 2.8 | 2.2 | 38.1 |

| 15 to 20 | 2.2 | 1.1 | 1.1 | 22.1 |

| More than 20 | 16.6 | 16.0 | 16.6 | 4.4 |

| Average | 8.1 | 4.7 | 5.7 | 11.5 |

| Based on five-year rolling price returns from June 2011 to June 2026. Figures represent the percentage of observations falling within each annualised return range. | ||||

The rolling-return distribution paints a much less flattering picture. On average, the PSU indices have delivered lower returns than the broader market, while negative five-year periods have been far more common. In contrast, the Nifty 500 has rarely produced negative five-year rolling returns.

The distribution of returns is equally revealing. The Nifty 500 spent most of its time generating annualised returns between 10 and 20 per cent, a range the PSU indices seldom occupied. Instead, PSU returns have been far more polarised, swinging between long periods of weak performance and occasional bursts of exceptional gains.

The bottom line

The recent report card of PSU indices is undeniably impressive. Their long-term record is far less so. That tension defines the category.

Several structural characteristics make PSU investing inherently cyclical: government ownership and policy-driven decision-making, heavy exposure to energy and other cyclical sectors, the persistent overhang of disinvestment and regulation, and returns that are closely tied to the capex cycle. For investors who are bullish on the PSU theme, that makes a strong case for treating PSU index funds as satellite holdings around a diversified core portfolio, rather than as its centrepiece.

That said, if you are still unsure of whether to invest in PSU funds or equity funds having allocation to PSU stocks, consider subscribing to Value Research Fund Advisor. Here, you can get personalised, in-depth guidance on your portfolio, helping you invest your money smartly over time.

Ask Value Research ![]()