Aprajita Anushree/AI-Generated Image

Aprajita Anushree/AI-Generated Image

Summary: A long-awaited recovery has driven strong gains in a key sector, supported by multiple growth triggers. But as optimism builds, valuations are beginning to reflect high expectations. The piece explores what happens when markets price in too much of the future.

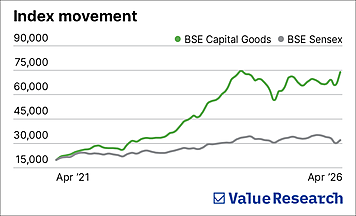

To understand why capital goods rewarded patient investors so handsomely, you have to first understand why it punished them for so long. The index peaked in early 2008, riding the wave of India’s infrastructure and construction boom. What followed was a collapse that took years to fully play out.

By 2014, the index had shed roughly 40 per cent from that peak, even as the Sensex recovered and moved higher. Infrastructure developers and power companies had overinvested through the mid-2000s boom and were now drowning in debt. Banks had stopped lending. GDP growth, which had touched 9 per cent, halved to around 4.5 per cent. New projects dried up. The government, paralysed by coalition politics and a cascade of policy controversies, could not step in to fill the gap.

For capital goods manufacturers, this was particularly brutal. Companies that make turbines, transformers, cables, and defence equipment cannot pivot to another product when demand falls. Their entire business model depends on large, lumpy orders arriving with reasonable regularity. When those orders stopped, profitability collapsed, and valuations followed. Many of these companies spent years simply surviving rather than growing.

This is what makes the subsequent recovery so dramatic. The sector was not just growing from a normal base. It was recovering from a prolonged trough, which meant that when the cycle turned, earnings did not grow incrementally. They snapped back.

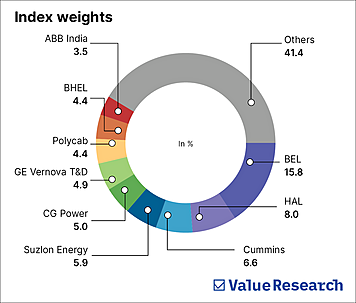

The turn came from multiple directions at once. The government’s infrastructure push across highways, railways, airports and metro rail created direct demand for engineering and construction equipment. The energy transition added another layer, as India’s renewable energy ambitions meant rebuilding the transmission grid to carry that power to consumers.

Grid upgrades require transformers, switchgear and high-voltage equipment that had seen almost no fresh investment for years. Demand surged precisely when domestic capacity to meet it was constrained. Defence added a third engine, as indigenisation redirected orders that had historically gone to foreign suppliers towards domestic manufacturers, bringing with them multi-year order cycles and revenue visibility the sector had not enjoyed in a long time.

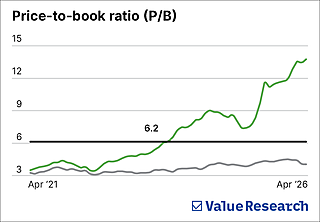

None of these appeared to be passing trends, and the market priced that in. Investors were willing to pay more for every rupee of earnings than before. When both earnings and valuations rise together, the returns compound in ways that can look, from the outside, almost effortless.

But that is precisely the risk sitting in the index today. Government capex, which has been the backbone of this entire cycle, is not guaranteed to grow at the same pace indefinitely.

Private investment, which was expected to pick up the baton as the cycle matured, has been slower to arrive. Any disappointment in order inflows or a shift in fiscal priorities could quickly expose how much optimism has already been built into prices.

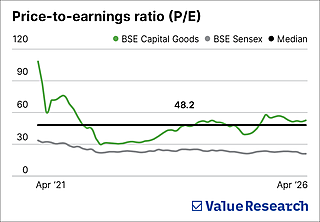

More importantly, even after accounting for genuine earnings growth, the index trades at a price-to-earnings (P/E) ratio of over 50 times. That is not the valuation of a sector where good news is still to be discovered. It is the valuation of a sector where a great deal of good news has already been priced in. At these levels, the margin for error is thin.

This article was originally published on May 01, 2026.

Ask Value Research ![]()