Vinayak Pathak/AI-Generated Image

Vinayak Pathak/AI-Generated Image

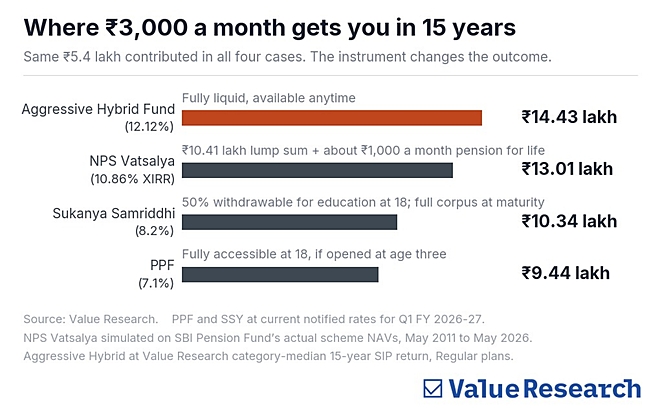

Summary: After PFRDA revised NPS Vatsalya rules this year, a Rs 3,000 monthly SIP over 15 years shows mutual funds delivering the highest corpus at Rs 14.43 lakh, followed by NPS Vatsalya, PPF and Sukanya Samriddhi. While mutual funds win on returns, the lock-ins in the other three schemes act as guardrails against premature withdrawals. The right choice depends less on which product returns the most and more on which one you can commit to leaving untouched until your child turns 18.

Every week, the same question lands in our reader mail: Should I open an NPS Vatsalya account for my child? After PFRDA rewrote the rules earlier this year, the answer needs to be revisited.

Four reasonable places exist to save in your child’s name: NPS Vatsalya, the Public Provident Fund (PPF), the Sukanya Samriddhi Yojana (SSY) and a plain mutual fund. They look similar in the brochure. They behave very differently when you actually need the money.

What changed in NPS Vatsalya

The Pension Fund Regulatory and Development Authority (PFRDA) revised the NPS Vatsalya rules earlier this year. Three changes from PFRDA matter.

Lump sum at 18. If your child’s corpus stays below Rs 8 lakh, the entire amount can be withdrawn. Above that, your child takes up to 80 per cent as a lump sum; the remaining 20 per cent buys an annuity from a registered insurer.

Asset allocation. January’s guidelines set an equity band of 50 to 75 per cent. A February follow-up allows Pension Funds to design their own pattern, with equity permitted up to 100 per cent.

The decision window. From ages 18 to 21, your child must complete new Know Your Customer (KYC) checks, then choose to continue in NPS, exit under the rules above, or shift to the All Citizen NPS model. Inaction by 21 auto-shifts the account to a high-risk variant.

The numbers

Consider a parent who saves Rs 3,000 a month for 15 years. Rs 5.4 lakh contributed in all. PPF and SSY use the current notified rates. NPS Vatsalya is a real 15-year SIP at SBI Pension Fund’s actual scheme NAVs from May 2011 to May 2026, with around 65 per cent invested in equities. The aggressive hybrid uses our category median 15-year SIP return for regular plans: 12.12 per cent.

Two findings stand out. The aggressive hybrid mutual fund gives Rs 14.43 lakh, fully in your child’s hands at 18, about Rs 4 lakh more than the NPS Vatsalya lump sum and Rs 5 lakh more than PPF. NPS Vatsalya is no longer disadvantaged: the 80 per cent rule makes it broadly competitive with PPF and SSY in terms of accessible money, while equity exposure lifts returns.

So why not simply pick the mutual fund?

Returns and discipline

Because returns are only half the story. The other half is whether the money is still there when the goal arrives.

A mutual fund SIP demands behavioural discipline that most savers struggle to muster. The corpus is always accessible, which also makes it available for a car in year seven, a panic sale during a sharp correction or a drawdown for an urgent household expense. In March 2020, equity fund redemptions and SIP stoppages spiked, including from accounts saving for long-horizon goals.

PPF, SSY, and NPS Vatsalya have lock-ins that may seem restrictive but serve as commitment devices in life. The corpus survives because you cannot touch it.

The honest question is not which gives the best return. It is which is the best return you will actually keep.

The small print

NPS Vatsalya tax. The Income Tax Act exempts only 60 per cent of the NPS lump sum at exit. PFRDA has raised the limit you can withdraw to 80 per cent, but not the tax-free limit. The extra 20 per cent is taxable as your child’s income in the year of withdrawal. For modest corpora under the basic exemption limit, this changes nothing. For larger ones, it bites.

The annuity rate. Insurers price life annuities higher for older buyers because they have fewer years left to pay. For an 18-year-old buying a lifetime annuity, the rate is closer to 4 to 5 per cent, well below the 6 to 6.5 per cent quoted for 60-year-olds. The 20 per cent of your NPS Vatsalya corpus that converts to an annuity at 18 produces a modest monthly pension, not meaningful retirement income.

The decision

State the goal first, in writing, before you open any account.

For a daughter saving for education or marriage: Sukanya Samriddhi as the core, plus an aggressive hybrid mutual fund for equity.

For a son saving for education or career launch: PPF as the core, plus equity in the same way.

For higher returns than PPF or SSY, with discipline built in: NPS Vatsalya is now genuinely competitive. The 80 per cent lump-sum rule means most of the corpus is your child’s at 18.

For the highest return and full flexibility, an aggressive hybrid mutual fund delivers more than any of the three above. But only if you genuinely will not touch it before the goal date.

Most families will mix two or three of these. That is fine. The mistake is not picking the wrong product. It is picking a product before you have named the goal or been honest with yourself about what you can leave alone.

Also watch: Best Investment for Your Child?

This article was originally published on May 13, 2026.

Ask Value Research ![]()