Aditya Roy/AI-Generated Image

Aditya Roy/AI-Generated Image

Summary: The Prime Minister, the Government and the largest AMC in the country reached the same conclusion about gold within 72 hours. That kind of convergence is rare. What happened in the 16 months before it explains why it matters now.

Three things happened in India this week that have not happened together before. On Sunday, the Prime Minister asked citizens not to buy gold for a year. On Tuesday, the Government imposed a 15 per cent customs duty on gold and silver. By evening, HDFC Mutual Fund withdrew its Gold and Silver NFO, scheduled to open this Friday.

The State, the Treasury, and the largest AMC in the country reached the same conclusion in 72 hours. The gold party is over.

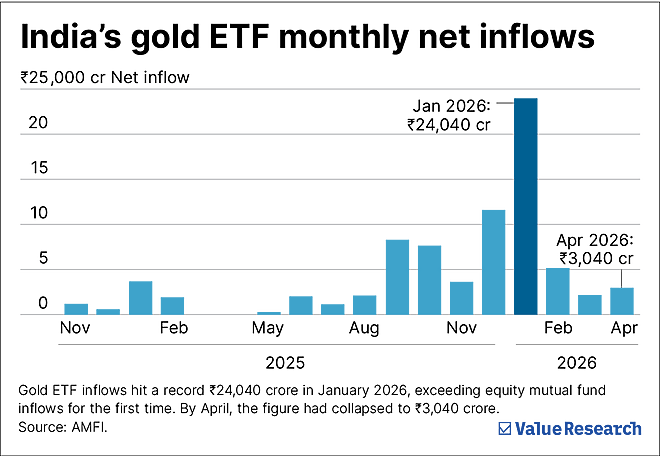

The number nobody is talking about

The AMFI flow data tells the cleaner story (see chart). Gold ETF inflows hit a record Rs 24,040 crore in January 2026. For the first time, they exceeded equity mutual fund inflows. By April, the figure had collapsed to Rs 3,040 crore. An 87 per cent fall in 90 days. Silver ETFs entered net outflows in February.

Around 75 per cent of all gold ETF inflows in the past three years came in just eight months, between September 2025 and April 2026. This was never a measured shift. It was a stampede.

Five years, and a cliff

Indian 24-karat gold was Rs 47,400 per 10 grams in 2021. Today it is Rs 1,62,000. A 243 per cent rise, most of it in the last 16 months. By late January, gold sat five standard deviations above its inflation-adjusted historical norm, as Ruchir Sharma noted in the Financial Times. The World Gold Council itself blamed 80 per cent of the rally on “risk and uncertainty,” meaning even the buyers did not know why they were buying.

On January 29, gold touched $5,595 an ounce. It crashed 21 per cent within 48 hours. The trigger was a US personnel announcement, not inflation data. By mid-March, gold had given back 27 per cent. The safe haven was not safe when everyone owned it.

The behaviour gap, in its purest form

Nobody bought gold ETFs when gold was Rs 30,000 per 10 grams. Modest interest at Rs 50,000. At Rs 1,30,000, it became the most popular product in the country. Price was the only signal.

At Value Research, we have documented this pattern for years. The behaviour gap is the difference between what a fund returns and what the average investor in that fund actually earns. Globally, it runs at 2.5 percentage points per year, because people buy after prices have risen and sell after they have fallen. In Indian gold over the last 18 months, that gap is almost certainly wider.

My position, updated

I was a gold sceptic for two decades. I changed my view in October 2024 because the central bank's buying after the Ukraine reserves freeze had altered the calculus. A 5-10 per cent gold allocation, held as insurance, is sensible.

But insurance is what you buy when it is cheap and boring, not when it is expensive and exciting. Gold at five standard deviations from norm, with the PM appealing against it, customs duty raised today, and HDFC pulling its NFO this evening, is neither.

The engine that drove this rally is already idling. Central bank gold purchases slowed to 5 tonnes in January 2026, from a 27-tonne monthly average in 2025. When the buyer stops buying, the price reflects it.

Three things to do this week

1. Count your jewellery. Most Indian households already have 20 to 30 per cent gold exposure, once jewellery is included. Adding gold ETFs on top is a form of concentration, not diversification.

2. If your financial portfolio has more than 10 per cent in gold, trim it. Use the rally to rebalance, not to add.

3. Do not start a new gold SIP this month. SIPs work for assets whose long-term direction is upward and whose short-term direction is uncertain. Gold at present levels fails both tests. Put that money into a flexi-cap fund instead.

When the Prime Minister, the Government, and the largest AMC signal the same thing in 72 hours, that is not noise. That is data. India’s mutual fund industry has rewarded performance-chasing for a generation. The behaviour gap is what investors pay for that habit.

Gold’s storybook has reached India. Your portfolio does not have to include a chapter..

Ask Value Research ![]()