AI-generated image

AI-generated image

It happens every so often that investors are swept off their feet in a love affair that is quick, gushing and eccentric. Case in point, Manorama Industries and its gobsmacking rally. The small-cap company's share price nearly doubled in less than two months! Its P/E ratio mounted a high of 102 times from 52 times between March 15 and April 26, 2024. This is despite its vapid ROCE of less than 15 per cent. So, why does it still have such a hold on investors? Find out in our analysis:

The business

If you ever ate a Ferrero Rocher chocolate or used Loreal's cosmetics, you likely consumed butter made by Manorama Industries. The company primarily produces cocoa butter equivalent (CBE), a synthetic substitute of cocoa butter, used in confectionery, chocolate items and cosmetic products. It procures exotic tree-borne seeds such as mango, kokum, and mowrah from India and shea from Africa to produce CBE and other specialty fats and butters. These seeds are extracted and processed at its Raipur plant. The company's client base includes renowned brands like Modelez, Ferrero Rocher, Loreal, Hershey's, etc. Exports make up a big chunk of the business, contributing around 43 per cent to its FY24 revenue.

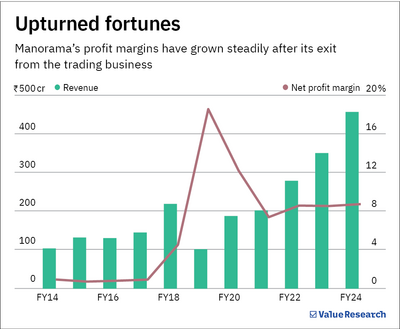

The growth meter

Manorama's days of glory followed a period of defeat. The company was originally a trader of agro-based commodities. Trading activities generated 72 per cent of its revenue in FY18. However, the business ended up being a dud with stagnant sales and low margins. Naturally, Manorama changed gears and exited the trading business in FY19 to transition into a fully integrated CBE player. Here's how this was done:

The procurement advantage. The company has in place a robust system of procuring seeds directly from the local tribal communities that grow them in India and West Africa. It did so by establishing strong relationships with these communities over the years. Since these communities do not easily place their trust in businesses, they are less likely to switch to new players.

Winning over customers. The company develops its products jointly with customers to address their specific requirements. The tailor-made solutions ensure that customers, too, do not switch to others. This stickiness has helped Manorama grow consistently with stable margins in the last four years.

Its revenue and profit after tax grew compounded 31 per cent and 39 per cent per annum, respectively, between FY21-24. The profit margins, too, witnessed robust growth.

What's behind the surge in the share price?

Industry tailwinds. Climate change-induced drought has ravaged cocoa crops in West Africa, which produces 80 per cent of the world's output. As a result, cocoa prices have been on a boil in the last few months, surging from $2,000-$3,000 per metric tonne (MT) to around $10,000 MT.

The chronic underinvestment in cocoa farms is another tailwind, which has led to very low replanting rates with cocoa trees quickly ageing. Against this backdrop, global chocolate and cosmetics companies are centering their focus more towards increasing the use of CBE, presenting a big potential for Manorama to scale up.

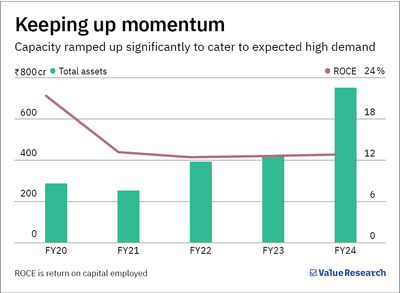

Capacity expansion. To meet the growing demand for CBE, the company recently commissioned a new fractionation capacity of 25,000 tonnes per annum (TPA), more than doubling its total capacity to 40,000 TPA. Further, it has strategically built large raw material inventories that have grown from Rs 158 crore in FY23 to Rs 389 crore in FY24 to ramp up CBE production in the coming quarters. This is expected to charge up sales and earnings ahead.

Valuation pitfall and more

The capacity expansion has cemented Manorama's growth prospects. But the frenzy in its valuation has been rapid, that too, due to a single development. It appears investors have already priced in most of the future growth, leaving no margin of safety. More importantly, other risk factors seem to have been ignored altogether. We suggest considering them before making an investment decision:

- Manorama's business is highly working capital intensive, requiring huge inventories due to the seasonality of raw materials. Its inventory days were 568 in FY24.

- The high working capital needs have resulted in poor cash flows forcing the company to significantly increase its short-term debt recently.

- The company's capacity expansion and inventory build-up has almost doubled its asset base, deteriorating its return ratios. However, it expects them to improve once capacity utilisation is optimum and inventories get liquidated.

- Its major customers are large chocolate companies. If they were to begin backward integration, Manorama would be in trouble.

- It is heavily reliant on Africa for sourcing shea seeds used for CBE production. Any geopolitical or climate-related issues there can disrupt its supply chain.

Note that this story should not be construed as a stock recommendation. Investors must do their due diligence before making an investment decision.

Also read: Varun Beverages: 7x rise in five years

Ask Value Research ![]()