We often exclude banks from many of our data-driven exercises highlighting market trends. The reason is rather simple: banks need to be treated differently.

Banks earn through lending. So, it might seem obvious that to grow and create wealth, they should lend more. However, loan book growth at the cost of asset quality leads to wealth destruction rather than creation.

Take, for example, the public sector undertaking (PSU) banks. Their performance over the last decade underscores the importance of asset quality.

The destruction era

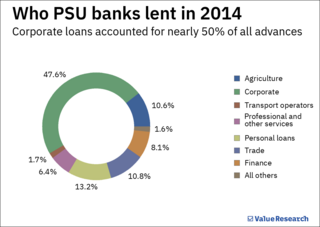

For the uninitiated, here's how the story unfolded. Public sector banks dished out enormous corporate loans in the first few years following the millennium. The strategy worked, too, as most industries were witnessing an upcycle thanks to India's economic boom. However, the recession of 2008 laid bare the cracks in the system that many already knew.

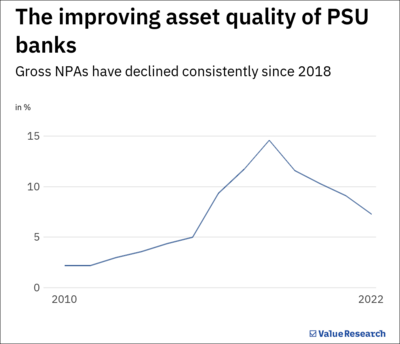

As the global economy stagnated, multiple industries witnessed a cash crunch. Unsurprisingly, the gross non-performing assets (GNPAs) of PSU banks skyrocketed to unprecedented levels, and profitability took a nosedive.

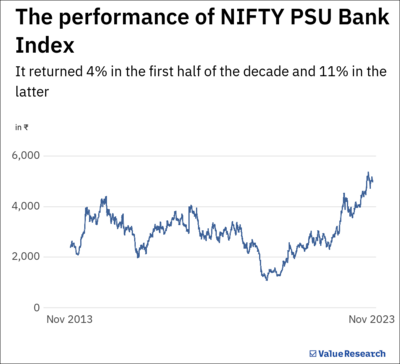

Their share prices ran parallel to their profitability, and investors suffered significant losses. Between FY14-19, the NIFTY PSU Banks index gave a measly four per cent annual return.

The redemption arc

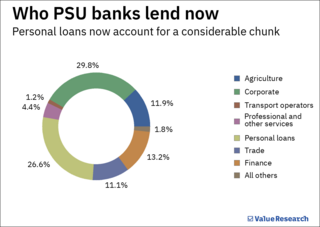

To recover, public sector banks had to take a page out of the playbook of their private sector counterparts. They started focusing on retail loans, which carry much lower risks given their smaller ticket size and larger spreads. In addition, retail loans provide diversification, safeguarding banks against industry-specific downturns.

The strategic shift acted like an elixir to the ailing loan books of public banks. Their share prices also followed suit. In fact, in the last two years, the NIFTY PSU Bank index has grown 34 per cent annually.

Investors' takeaway

The above example highlights the importance of asset quality for banking stocks. However, the underlying lesson to learn is one of sustainable growth.

Businesses must survive periodic downturns and capitalise on economic booms to create wealth for shareholders. Banks are no different in that regard. Their growth must also be based on sustainable models, capable of withstanding all moods of the economy.

In short, if you are looking into banking stock, scrutinise who it lends to and not just how much it lends.

Also read: Beyond the PSU stock hype

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()