Indian aluminum major Hindalco Industries, which is a part of the famous Aditya Birla Group has fallen more than 30 per cent during the last three months. From being close to a 52-week high, it has come close to its 52-week low.

While the general volatility in the market is also a reason, there are a couple of other reasons why the shares took a toll.

Disappointing results from Novelis

While Hindalco's overall EBITDA (earnings before interest tax depreciation and amortisation) increased, its subsidiary Novelis posted an adjusted EBITDA of $431 million (Rs 3,247 crore) in the Q4FY22 compared to $505 million (Rs 3,705 crore) in Q4FY21, a 15 per cent year-over-year decrease. Adjusted EBITDA per ton too decreased by 15 per cent year over year from $514 in Q4FY21 to $437 in Q4FY22. The net profit of Novelis increased by 21 per cent mainly due to a fall in interest expense. The market was also a bit concerned as Novelis has announced a $3.4 billion capex which will be commissioned from FY26, which will also have an impact on the company's free cash flows.

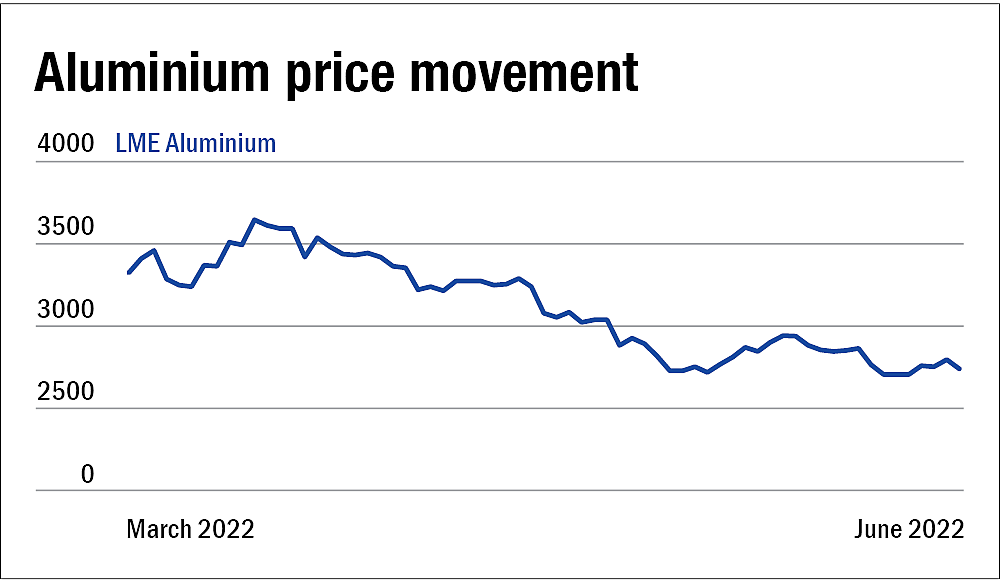

Falling aluminum prices

A major reason for Hindalco's consistent increase in revenue and profits during the year was rising aluminum prices which resulted in a higher realisation. But it seems like things are coming to an end in that angle as aluminum prices have been falling sharply in the last three months thereby returning to normalcy. The subsequent quarter or Q4FY23 quarter may face the pressure of a high base in Q4FY22. Falling aluminum prices may make it difficult for the company to sustain the same levels of revenue and profits.

Also read:

Good times in the stock market

ONGC trumps Tata Steel and TCS

Ask Value Research ![]()