Ujjal Das/AI-Generated Image

Ujjal Das/AI-Generated Image

Summary: Every year, you can book Rs 1.25 lakh of equity gains tax-free. The maximum you can save is Rs 15,625. And the larger your portfolio grows, the smaller that saving becomes as a share of what you actually owe. The benefit fades precisely when your tax bill starts to matter.

Every financial year, the tax code hands equity investors a small gift. Long-term capital gains, the profit on shares or equity funds held for more than a year, are taxed at 12.5 per cent, and the first Rs 1.25 lakh of those gains is tax-free.

Around this exemption has grown a March ritual: sell enough units to book Rs 1.25 lakh of gain, buy them back the next day, and you have raised your cost base without paying a rupee of tax. Three months into a new financial year, with no deadline pressing, is a good time to ask what the ritual earns.

Less than the effort suggests. The most it can save you in a single year is Rs 15,625; you can rarely get even that, and the benefit matters less as you grow wealthier, which is precisely when your tax bill starts to matter more.

The ceiling is Rs 15,625 a year

The cap takes no finding. The exemption is Rs 1.25 lakh, and the rate is 12.5 per cent, so the most you can avoid in a year is Rs 15,625, or Rs 16,250 after adding the cess. No amount of clever timing moves it further.

Over a 20-year holding period, you get 19 usable harvests, since your first year's units are not yet in the long term. Fill in the exemption for each of them, and you save about Rs 2.97 lakh, against a Rs 10 lakh investment that grows past a crore over the same period. Even this best-case scenario assumes Rs 1.25 lakh in fresh long-term gains to harvest every year without a miss, which most investors cannot manage.

A fixed ceiling on a growing tax bill

We modelled the strategy on the BSE Sensex Total Return Index, which includes dividends as well as price movements, across all rolling periods since 1996. A Rs 10 lakh lumpsum, held for 20 years and harvested annually, saved a median of Rs 2.77 lakh. That is about 1.9 per cent of the final corpus, or roughly 12 basis points per year added to your return, and the exemption could be filled in only about a third of the periods we tested.

The longer you compound, the harder the cap bites. Over 10 years, the savings amount to about 40 basis points per year. Over 20, it falls to 12 because the savings are capped while the corpus is not. The same squeeze appears when the sums grow.

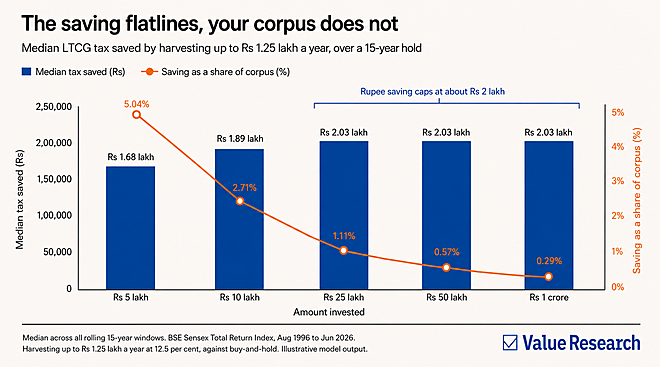

Once your corpus is large enough to generate Rs 1.25 lakh in annual gains, the rupee savings hit the cap and stay there. Over a 15-year holding period, an investor with Rs 25 lakh and one with Rs 1 crore both save about Rs 2 lakh in tax. As a share of the corpus, though, the saving falls from 1.1 per cent to 0.29 per cent.

This is the heart of the matter. The investor with the largest gains, and therefore the largest future tax bill, gets the least help from harvesting. The break is generous when your tax is trivial and fades towards irrelevance just as your tax bill turns serious.

The real objection is size, not cost

The natural reply is that the strategy is free, so why not take it? On cost, the reply is fair. Selling and buying back a day apart, the way a real fund redemption settles, trimmed the benefit by less than one per cent in our tests and never turned it negative. The securities transaction tax on a fund redemption of this size comes to about five rupees, though direct stocks pay 0.1 per cent on both legs and take a far bigger bite. For a fund investor with no exit load, cost is genuinely not the problem. Size is.

For most of our readers, the case is thinner still. In a SIP, every instalment starts its own one-year clock, so harvestable long-term gains build slowly. A Rs 10,000 monthly plan has close to nothing to harvest in the first year, about Rs 11,000 in the second and about Rs 50,000 in the third, against an exemption of Rs 1.25 lakh. In no period we tested could a monthly investor fill the exemption every year. There is a twist too: a SIP that puts in Rs 24 lakh over 20 years saves less tax than a one-time Rs 10 lakh investment, because what you can harvest depends on how long your money has been invested, and SIP money has been invested, on average, for less time.

One case deserves a warning. Harvest inside an exchange-traded fund, and the price you buy back at can sit above the fund's indicative net asset value. That premium is a real cost that a regular index fund does not impose, and it can swallow up much of the benefit this thin.

Worth doing only if it costs you nothing

If your platform harvests automatically and your fund carries no exit load, go ahead. It is a free, if small, gain. Just keep it in proportion: a few lakh of tax saved over two decades, against a corpus running into crores, is a rounding error. Take it when it is free. Leave it when it is not.

What you should never do is organise a real investing decision around it. No harvesting move will shift your wealth the way three larger choices will: how much you invest, how long you stay invested, and which funds you hold.

That last choice is the one worth your energy. If you are no longer sure your funds deserve their place, that is exactly what Value Research Fund Advisor is built to settle: a researched portfolio, monitored for you, and changed only when the evidence demands it. Get that right, and the exemption will look after itself.

This article was originally published on July 14, 2026.

Ask Value Research ![]()