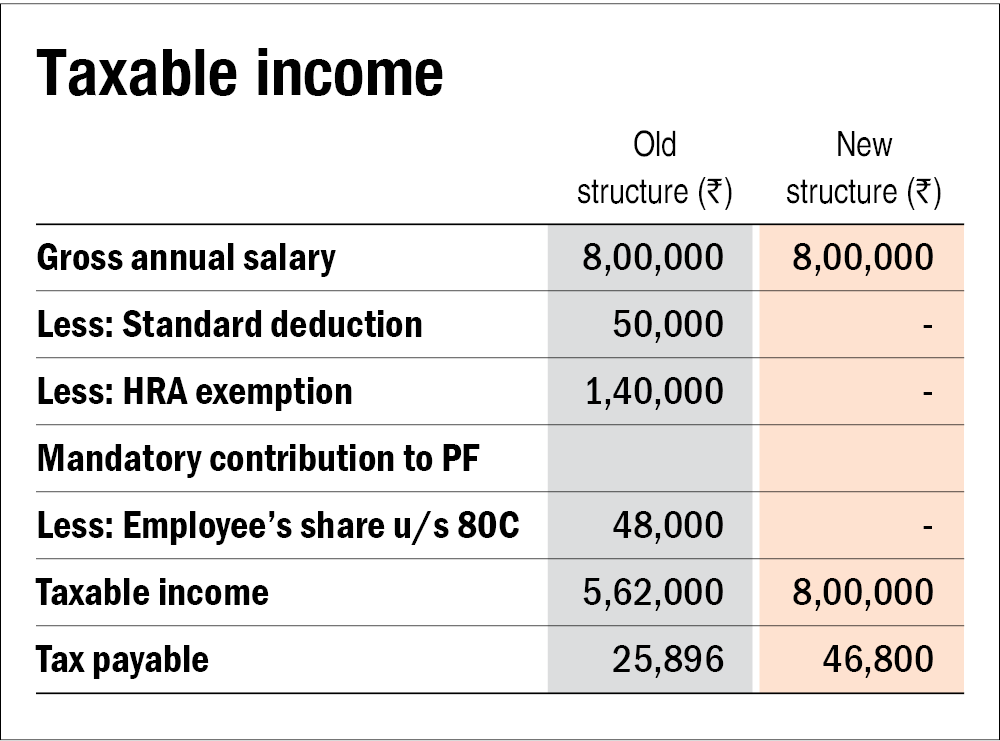

Manish is 33 years old. And works with an IT company. As part of the annual appraisal, his salary has been revised to Rs 8 lakh per annum. And is now wondering whether opting for the new tax slabs would be more beneficial to him or if he should continue with the existing taxation regime.

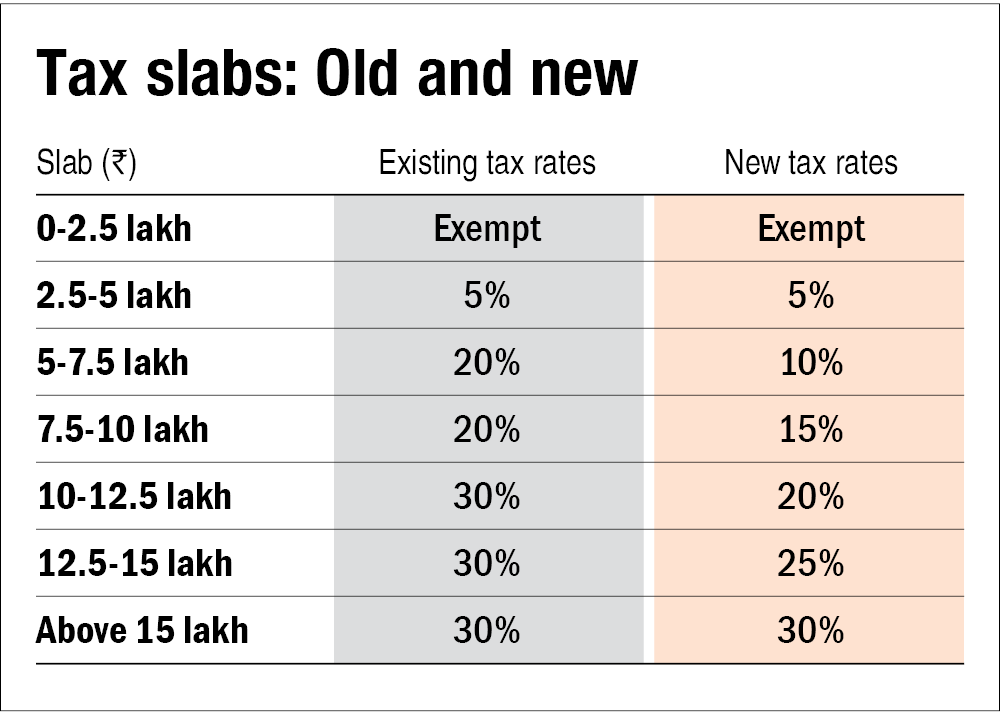

See the table 'Tax slabs: old and new'. The salaried can choose either of the two systems, and even switch between them from one financial year to the next. However, businesspersons can choose their tax slabs only once. After they have done so, they must continue with them.

In the existing (old) taxation system, one can claim a variety of deductions and exemptions. On the other hand, the new tax slabs are simplified. They have no deductions or exemptions, except for a few miscellaneous ones such as deduction for agricultural income and leave encashment on retirement. However, they also have lower tax rates.

Here is what Manish will have to pay in tax under the existing tax system and under the new one.

Existing tax slabs:

The existing taxation system allows many deductions and exemptions that can lower your taxable income. Manish has the following:

Standard deduction:

A deduction of flat Rs 50,000 is allowed for all the salaried and pensioners.

House rent allowance (HRA)

Manish lives in a rented accommodation for which he is paying Rs 15,000 every month. The basic pay and HRA components of Manish's annual salary are Rs 4 lakh and Rs 2 lakh, respectively. He can claim a tax exemption of Rs 1.4 lakh on HRA by producing the rent receipts, rent agreement and the PAN of his landlord.

How to calculate your HRA

Your HRA entitlement should be the least of the following:

- Actual HRA received

- Actual rent paid minus 10 per cent of basic salary and dearness allowance (DA), if any

- 50 per cent of basic salary and DA (if any) if you are living in a metro city, otherwise 40 per cent

Provident fund deduction

An amount of Rs 4,000 is deducted every month from Manish's salary. This goes towards his mandatory provident-fund contribution, which is eligible for tax deduction under Section 80C. If Manish continues in the old regime, an amount of Rs 48,000 (4,000 × 12) can be further reduced from his taxable income.

Tax liability

After considering the above deductions, Manish will have a taxable income of Rs 5,62,000. His tax would be Rs 25,896. However, he can reduce his tax liability to zero by investing Rs 62,000 more under Section 80C. Section 80C has many investment avenues, such as the Public Provident Fund, five-year FD, National Savings Certificate, etc. Of those, we recommend tax-saving mutual funds, also called equity-linked savings schemes (ELSS), as they are the best from a returns perspective. Manish can do an SIP of Rs 6,200 in a good tax-saving mutual fund throughout the financial year. This will reduce his taxable income to Rs 5 lakh, after which he can claim a rebate of Rs 12,500 under Section 87A. This will bring down his tax liability to zero.

New tax slabs

While the new tax slabs bring simplicity to taxation and have lower tax rates in the absence of any exemptions, one's tax may actually go up, as seen in the table below.

Even if Manish is not able to invest Rs 6,200 every month in tax-saving funds as advised above, he will still be at a loss under the new tax regime. He will have to pay an additional tax of Rs 20,900. So, Manish should continue in the old tax regime.

Don't limit your investment to just saving taxes

While Manish would be able to reduce his tax liability to zero by investing just Rs 6,200/month, he should not stop there. He should try to save more to meet his various goals. He should also have a contingency fund equivalent to at least six months of his expenses. It should be maintained in a combination of sweep-in fixed deposits and liquid funds. If he has financial dependents, he should buy a pure term plan. Its premium is also eligible for deduction under Section 80C. Finally, medical emergencies can be financially exhausting. So, an adequate health insurance cover is indispensable.

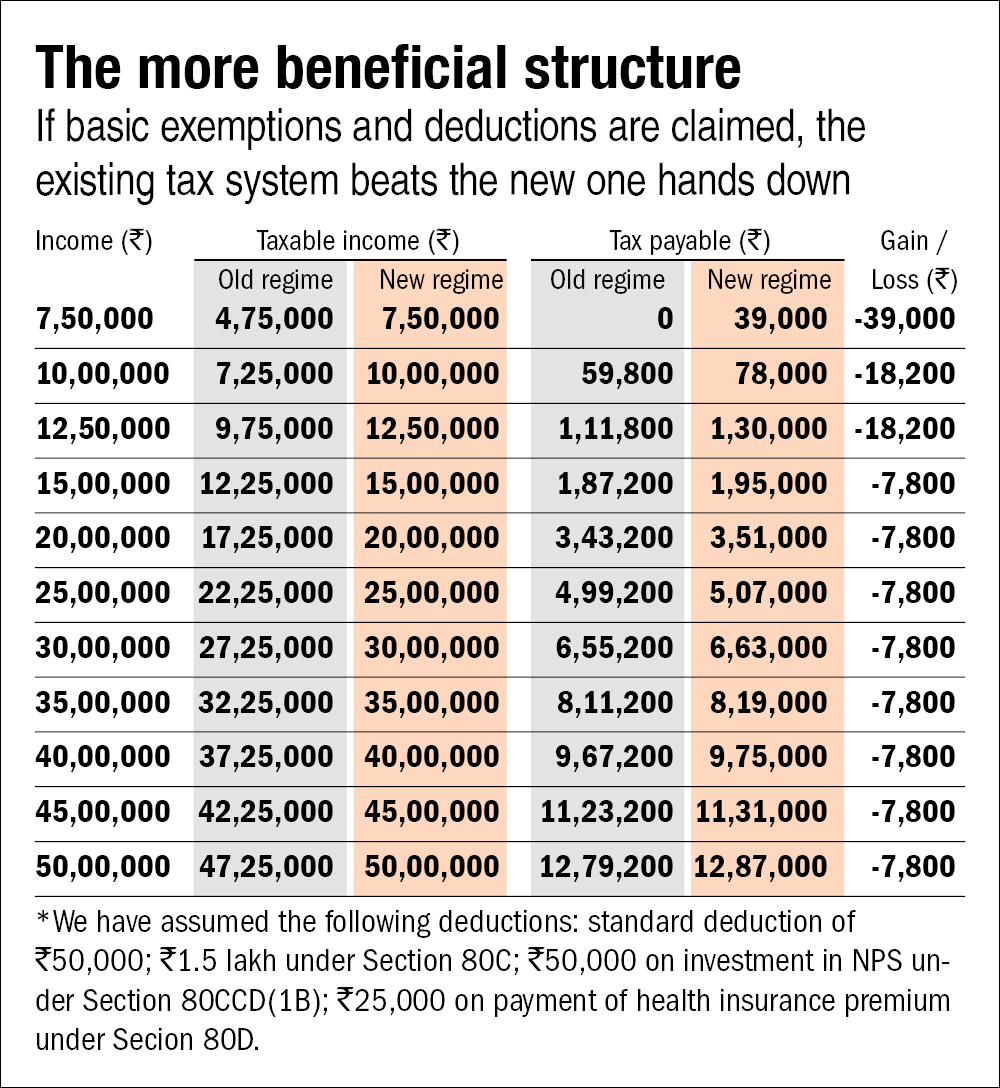

How to choose between the old and new tax structures

Look at the table 'The more beneficial structure'. It shows that if you go for deductions and exemptions for Rs 2,75,000 (including the standard deduction, Rs 1.5 lakh 80C limit, Rs 50,000 additional NPS contribution under Section 80CCD(1B) and medical insurance premium of Rs 25,000 under Section 80D), you can pay much less tax in the existing system if your income is up to Rs 15 lakh. Over that amount, the difference is nominal and one can opt for the convenience of the new tax slabs. Of course, if you are able to claim more exemptions and deductions, your tax liability can be lower. Use Value Research tax calculator to figure out which tax regime is beneficial for you.

This article was originally published on January 15, 2021.

Ask Value Research ![]()