Yogesh Sharma/AI-generated image

Yogesh Sharma/AI-generated image

Summary: A low price-to-book ratio can signal a bargain or a business the market has rightly abandoned. Momentum can reward a genuine winner or a speculative rally about to unravel. Factor investing has decades of evidence behind it and a structural flaw that the evidence alone won't fix.

Factors offer a structured, rule-based way to navigate markets. They rank companies by measurable traits with decades of evidence tied to long-term returns. Quality favours strong fundamentals for stable compounding. Value favours companies priced below their worth, rewarding the patient and contrarian investor. Momentum favours recent winners for those at ease with higher churn and high short-term volatility. Low volatility favours smaller price swings for investors who prize capital preservation. Multifactor blends all four for diversified, cycle-resilient exposure.

The theory is sound and the academic evidence deep. So why do raw factor portfolios still carry hidden risks in practice? The missing layer is not a better factor. It is better filtration.

The illusion of raw factors

A raw factor portfolio ranks every stock on one single-factor score and selects the top names. The flaw is structural. A score tells you where a stock ranks, not its quality, governance or risk.

A low price-to-book ratio can signal a bargain or a business the market has rightly abandoned. Reliance Communications looked cheap as debt rose and its business weakened. After failing to repay lenders, it entered bankruptcy in 2019, leaving shareholders with nothing.

Momentum has its own trap. Brightcom Group, an advertising-technology firm, surged on a speculative rally in 2021, then lost more than 70 per cent once the regulator probed its accounts. Satyam Computers fooled both a low-volatility and a quality screen.

A ranking tells you the position, not the quality of what occupies it.

What gets in without a filter

Not every stock that passes a factor screen belongs in a portfolio. Three red flags stand out consistently.

The first is low return on equity (ROE). Companies in the bottom decile (bottom 10 per cent) of ROE often earn less than the cost of capital and tend to destroy it over time. The second is high debt-to-equity ratio. High leverage amplifies losses in downturns and can turn ordinary falls into permanent capital losses. The third is heavy promoter pledge, a red flag specific to Indian markets, which can invite forced selling even when the stock still scores well on a screen.

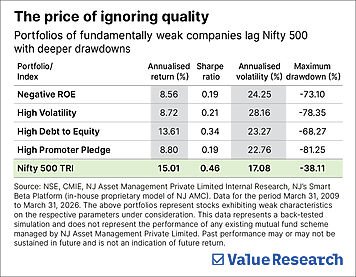

Beyond these, interest coverage ratio, earnings consistency and auditor’s independence also matter. The cost difference is measurable. Over the last 17 years, the Nifty 500 TRI returned about 15 per cent annually. Fundamentally weak companies’ portfolio managed roughly 8 to 14 per cent and fell far harder, dropping 68 to 81 per cent from peak against the index’s 38 per cent.

How filtration works

Filtration works in two stages. First, screen the universe for financial health, removing names that fail minimum standards on ROE, leverage and promoter pledge. Then rank the survivors on the target factor. What remains is factor-attractive and fundamentally sound.

The gains are consistent across styles. Value avoids value traps. Momentum sidesteps speculative rallies. Quality gets rid of highly-levered companies. Multifactor avoids the worst of each.

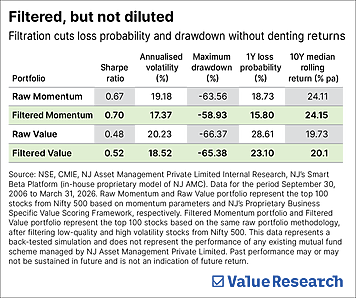

Filtered momentum, for instance, reduces the one-year loss probability from 18.7 per cent to 15.8 per cent and annual volatility from 19.2 per cent to 17.4 per cent, while the 10-year median rolling return stays almost unchanged at 24 per cent. Filtered value shows a similar pattern: lower drawdown, lower loss probability, comparable long-run return.

The hidden benefit

The gain from filtration is not only in returns. Filtered portfolios fall less and swing less because the wealth-destroying tail of weak companies is removed. The improvement is asymmetric: most of the upside is preserved while much of the downside is shed. With regular rebalancing, the portfolio cleans itself, dropping a name as fundamentals weaken.

A filter is not optional

A filter is not a mere tweak. It is what turns a factor model from a ranking exercise into an investable portfolio. That is the point of our investment approach and philosophy: each model starts with a factor score and a slew of financial-health and quality filters are applied so that weak companies do not enter the portfolio.

India has more than 5,000 listed companies, but that abundance doesn’t signal opportunity. In such a market, a robust factor framework must do more than just sort the attractive. It must first remove what should not be owned.

Also read: Process before performance

Ask Value Research ![]()