Adobe Stock

Adobe Stock

Summary: Even as broader markets struggled, PSU stocks stood out with strong gains. Their performance reflects a shift that investors took time to recognise, but the real test may still lie ahead.

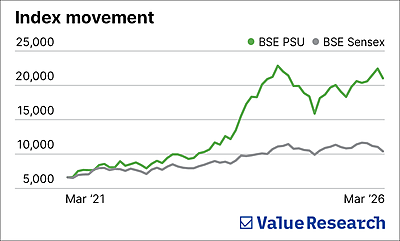

The Indian stock market has had a forgettable year. The Sensex is barely above where it was 12 months ago. Mid and small caps have corrected sharply. And yet, the BSE PSU index has delivered strong double-digit returns over the same period. For investors conditioned to think of public sector companies as slow, bureaucratic and perpetually disappointing, this needs explaining. The short answer is that a small number of PSU businesses had already fixed themselves. The market just took a long time to notice.

A banking system back from the dead

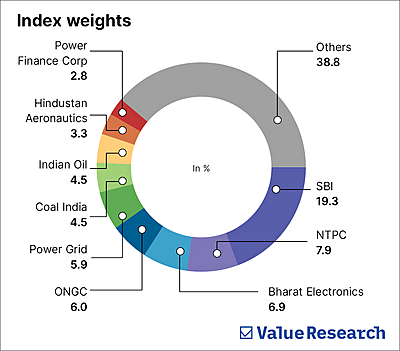

The dominant force behind the index’s performance is PSU banks, and the story here is not a small one. For the better part of a decade, India’s government-owned banks were in genuine crisis. They had lent recklessly to infrastructure projects in the 2000s, many of which collapsed. The bad loans piled up, were hidden, and then finally forced into the open. Banks stopped lending. Profits evaporated. The government spent hundreds of crores recapitalising institutions that seemed to have a limitless appetite for losses.

What followed was slow and unglamorous: loans were restructured or written off, managements were changed, the Insolvency and Bankruptcy Code gave banks real tools to recover money from defaulters, and one by one the balance sheets began to heal. For years, none of this showed up in stock prices because investors had been burned too many times. They waited for proof.

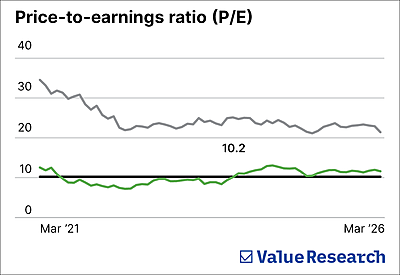

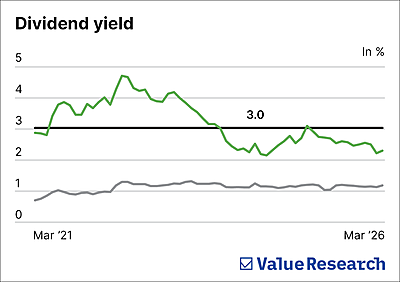

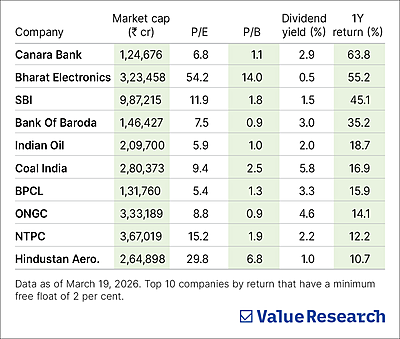

The proof came in the form of earnings and, most importantly, improved asset quality. PSU bank profits reached levels not seen in decades. The ratio of bad loans to total loans fell to its lowest in years. Return on equity, long an embarrassment compared to private banks, crossed into territory that demanded attention. And through all of this, valuations stayed low because the market had not yet decided to believe the recovery was real and lasting.

When the broader market started struggling, and investors began looking for something with actual earnings at a reasonable price, PSU banks were the most obvious answer in the room. The re-rating that followed was not driven by optimism. It was driven by a recognition that these banks had changed, and the price had not.

Defence: From supplier to compounder

The defence names in the index tell a different story. Bharat Electronics and Hindustan Aeronautics have been beneficiaries of India’s long-standing push to buy less from abroad and make more at home. This policy existed for years without much visible impact. What changed recently is that the order books at both companies became large enough and credible enough that investors could see earnings several years into the future. That kind of visibility is rare and valuable, particularly in an otherwise uncertain market. The re-rating here was less about recovery and more about the market finally taking the indigenisation story seriously.

The real reason PSUs outperformed

This is not the entire picture for sure, since there are several other entities and sectors that have contributed to this growth, but this gives us an idea. But we must remember one thing: Markets do not reward the past. They reward the gap between what a business is and what the market thinks it is. For most of the last decade, PSU companies were priced as though nothing about them would ever improve. Some of them did improve substantially, but the discount in their valuations persisted out of habit and memory.

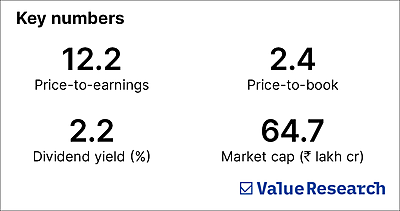

An important thing to remember here is that PSUs, especially banks, while having improved, still trail their private peers. These companies made a lot of sense at a heavily discounted valuation, but the same cannot be said after the surge over the past few years. Now starts the real test.

This article was originally published on April 01, 2026.

Ask Value Research ![]()