AI-generated image

AI-generated image

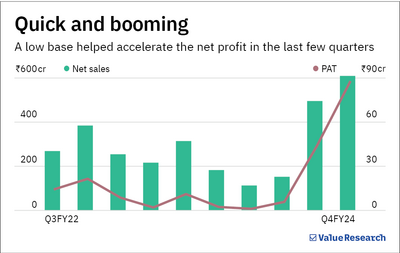

The modern tale of finding El Dorado, the fabled city of riches sought by explorers in 16th century South America, has played out in the Indian stock market. Shakti Pumps, a manufacturer of pumps and motors, found its own El Dorado a few years ago that has begun to generate handsome rewards recently. The treasure trove helped the company grow its net profit almost six times in FY24. But in the latest quarter, this figure grew even more astronomically. The company's profit after tax of Rs 2 crore in Q4 FY23 shot up to Rs 90 crore in Q4 FY24; a leap of 45 times in a year!

Landing a windfall

Shakti Pumps' El Dorado has been the government's 'PM-KUSUM' scheme, which has landed the company its recent windfall. The scheme aims to increase solar energy usage in agriculture by subsidising farmers to use solar pumps. After its launch in 2019, the company that had been eyeing this opportunity shifted gears and turned its focus sharply towards solar pumps through innovation and research. Its first-mover advantage has helped it clutch the highest market share under the scheme, which was 25 per cent as of Q4 FY24. In the same quarter, it delivered 15,000 solar pumps to farmers under the scheme, which grew its revenue by 41 per cent YoY and led to the explosive net profit growth. This was in part due to a lower base and raw material costs. The company has applied for 27 patents for its solar pumping solutions and has received 13 so far.

Will the banner year continue?

The company's total order book was worth Rs 2,500 crore at the end of FY24. This will be executed over the next 18 months, providing enough revenue visibility. Moreover, about 49 lakh pumps, across the components where the company is present, are required to be installed under the KUSUM scheme. Of this, only 282,708 have been executed as of Q3 FY24. Given the company's leading market share, it expects to grab orders with annual revenue potential of Rs 7,000 crore in the next two to five years (nearly 3 times its current order book of Rs 2,500 crore). To cater to the demand, the company recently raised Rs 200 crore via a QIP to double its revenue potential to Rs 5,000 crore. It has also acquired 46 acres of land in Madhya Pradesh for this expansion.

In addition, it has forayed into the electric vehicle (EV) space, manufacturing EV motors, charging stations, battery management systems, and more. The company will derive synergy from this venture since its current technology will be used to manufacture EV motors and pumps. It has invested Rs 30 crore in this business and has sold 10,000 two and three-wheeler motors since December 2021.

The caveats

The company hopes to maintain its operating profit margin of 15 per cent in coming years. Achieving a topline of Rs 7,000 crore per annum will, thus, generate Rs 1,000 crore in operating profit each year (it was Rs 225 crore in FY24). At the company's current market-cap of Rs 7,000 crore, it is valued at an attractive m-cap/EBITDA ratio of 7 times. But, every prize has its price.

- Threat from competitors: The market opportunity under the scheme is vast given only a tiny portion of the government's target has been met so far. Low entry barriers are further expected to drive competition. Additionally, the low payback period in this industry is enticing as well. For instance, Shakti Pumps will spend just Rs 200 crore to add an additional capacity with revenue potential of Rs 2,500 crore. Assuming that the company operates at full capacity and earns an annual operating profit margin of 15 per cent, it will generate Rs 350 crore of EBITDA from its capex of Rs 200 crore in less than a year. Such lucrative prospects are likely to attract many new players. This is already evident from its market share, which declined from 35 per cent in Q3 FY23 to now around 25 per cent as peers like Tata Power, Roto Pumps and Kirloskar Brothers increasingly vye for a pie.

- Revenue concentration: The company's revenue share from the government was 67 per cent as of FY24. This part of the business is highly lumpy as tenders are not floated at regular periods, which makes order flows inconsistent. Moreover, in FY23, the company experienced a drop in sales and margins as raw material costs shot up but the government held back on price revisions of contracts.

Shakti Pumps' growth acceleration has been top-notch but the company operates in a market, which by design, has many limitations. How long it can keep the ball rolling remains uncertain.

This story is not a stock recommendation. Please do your own research before making an investment decision.

Also read: What does the new SEBI order mean for holding company stocks?

Ask Value Research ![]()