John D Rockefeller once said, "Do you know the only thing that gives me pleasure? It's to see my dividends coming in."

Investors are united in their love for dividends, and many have a considerable part of their portfolio dedicated to companies that pay out high dividends consistently.

However, there's a widespread belief in the community that high dividend yield companies are usually mature companies with little legroom for growth. And companies that don't pay out dividends regularly are doing so because they see growth on the horizon.

While this belief is somewhat true, it downplays the fact that consistent dividend payments highlight something far more important: The financial health of the company.

You see, to pay out dividends consistently, the company must have cash on its books. In other words, it should be able to turn its earnings into cash. So if a company has been paying out high dividends regularly, investors can rest easy knowing that the company's profits are not notional.

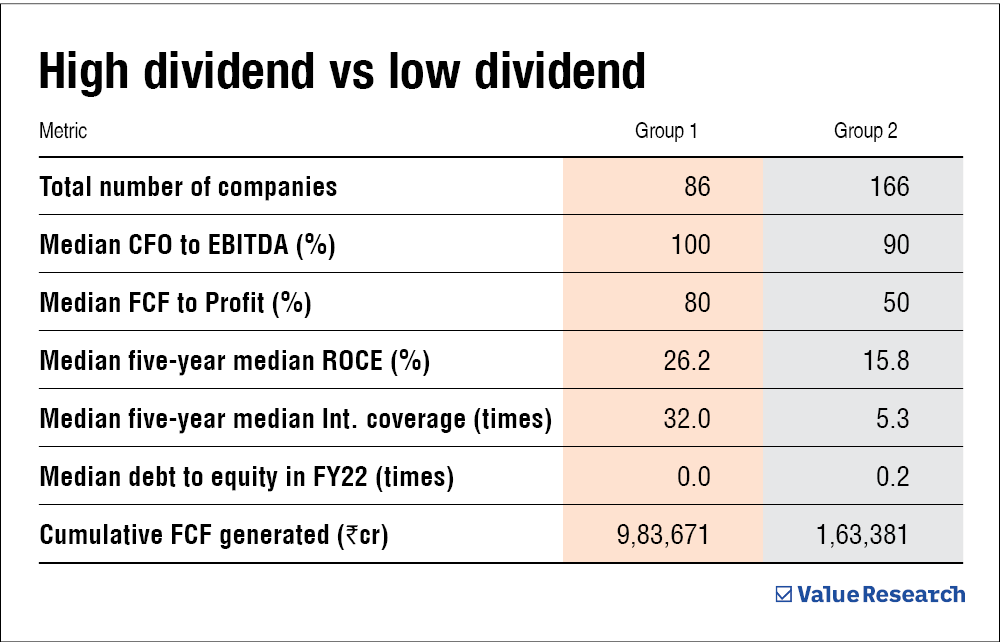

To prove our point, we conducted this simple exercise. We took the BSE 500 index and divided its constituents into two groups: Group 1 and Group 2.

Group 1 consists of companies with a dividend payout ratio of at least 25 per cent in each of the last five years. In other words, they paid out at least 25 per cent of their earnings to shareholders as dividends in each of the previous five years. Group 2 is the polar opposite. These companies did not have a dividend payout ratio of 25 per cent in any of the last five years.

Our aim was to compare the companies in these two groups in terms of their ability to convert their earnings into cash. Here's what we found.

In terms of converting accounting profits (EBITDA) into cash flow (CFO; cash flow from operations), Group 1 was awe-inspiring. Their five-year median cumulative CFO to EBITDA was 100 per cent! To put that into perspective, if all the companies in Group 1 were a single entity, the entity would likely be able to turn all of its accounting profits into cash.

And individually, they are not far off either. Ninety per cent of the companies have a five-year median CFO to EBITDA of more than 80 per cent. Now compare that with Group 2, where only 67 per cent of the companies have a median CFO to EBITDA of 80 per cent.

Clearly, there's a connection between high dividend payout and the ability to turn EBITDA into CFO.

But what about debt? EBITDA doesn't account for debt, and what if companies in Group 1 have large amounts of debt?

Even in terms of converting net profit into free cash flow (which is cash left after paying for operating expenses, capital expenditure, etc.), Group 1 maintains its lead.

Group 1's median cumulative FCF to net profit is 80 per cent. In contrast, Group 2's median cumulative FCF to net profit is a meagre 50 per cent.

So to summarise the results, companies with a history of consistent and high dividend payout (Group 1) are also significantly better at converting their earnings into cash compared to companies that don't pay out dividends regularly.

More than just cash

So our claim is indeed correct. High dividend-paying companies are better at converting their profits into cash.

However, that is not all.

In our exercise, we also found that the companies in Group 1 also have better median ROCE! In addition, all the companies in Group 1 have a median five-year interest coverage ratio (a metric for a company's ability to pay back its debt) of more than two times. In contrast, only 77 per cent of the companies in Group 2 could claim such numbers.

While a direct correlation might be stretching it, it is safe to say that high dividend payouts are a good omen for a company's capital efficiency and interest coverage.

Are low dividend paying companies bad investments?

No, of course not. As we have mentioned earlier, there's truth to the notion that companies often pay out low dividends to conserve cash for future growth.

Even in our exercise, Group 2 had many companies that have earned their right to be called wealth creators. Growth requires cash, and often, companies that are in their growth phase pay little to no dividends and have negative free cash flows in many years.

Our exercise aimed to show the link between high dividend payments and a company's financial health. In an age where companies are hiding their losses behind gimmicks like adjusted EBITDA, it is crucial to remind investors of the real signs of a financially healthy company. And dividends are indeed one of the signs.

Also read: Which is better: ROE or ROCE?

This article was originally published on March 03, 2023.

Ask Value Research ![]()