Adobe Stock

Adobe Stock

Summary: India’s power sector spent more than a decade trapped by financially broken utilities and stalled investment, despite rising electricity demand. Here is how reforms, surging power consumption and the renewable-energy buildout combined to finally revive the sector and reshape the fortunes of power and equipment companies alike.

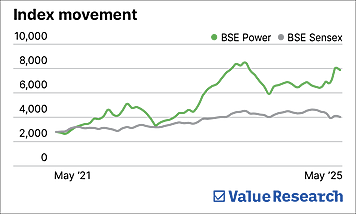

The BSE Power index peaked in January 2008, collapsed, and spent the next 14 years going nowhere.

The root cause was not a shortage of electricity demand; it was a broken customer. State electricity distribution companies (DISCOMs) were technically bankrupt, buying power at market rates and selling it below cost for political reasons. Aggregate technical and commercial losses ran at 23.7 per cent in FY2016. Power companies could not collect what they were owed, equipment manufacturers had no buyers, and the entire value chain froze.

Reform before revival

The revival began with governance, not demand. The Ujwal DISCOM Assurance Yojana (UDAY), launched in 2015, enabled states to absorb 75 per cent of DISCOM liabilities through low-interest bonds and pushed operational reform.

The Revamped Distribution Sector Scheme (RDSS), launched in 2021, tied central funds to performance improvements. Aggregate losses fell from 23.7 per cent in FY16 to 15.8 per cent by the early 2020s. The sector’s largest customers were becoming creditworthy again, unlocking a decade of stranded investment.

The demand shock nobody saw coming

Then came an unanticipated demand surge. India’s peak electricity demand rose 68 per cent between 2014 and 2024, from 148 GW to 250 GW, driven by post-Covid industrial capacity, rising air-conditioner penetration and surging economic activity.

The renewable multiplier

Renewable energy proved decisive, but its real impact lay in infrastructure demand. Unlike coal plants, solar farms in Rajasthan require hundreds of kilometres of transmission lines, substations, and switchgear.

India’s non-fossil capacity tripled from 81 GW to 250 GW between 2014 and September 2025, with Rs 9.15 lakh crore earmarked for transmission by 2032. This created a global equipment shortage: transformer lead times exceeded 24 months, that Indian manufacturers, having survived the lean decade, were perfectly positioned to capture.

Data centres add a new chapter

Data centre electricity consumption in India is set to grow at nearly 15 per cent per annum through 2030, over four times faster than all other sectors combined. Capacity is set to grow from 1.2 GW in 2024 to 4.5 GW by 2030.

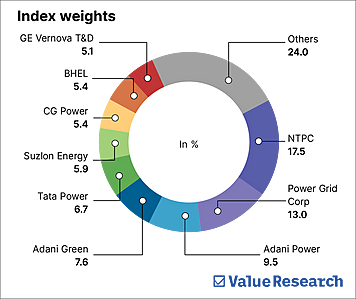

Two businesses, one index

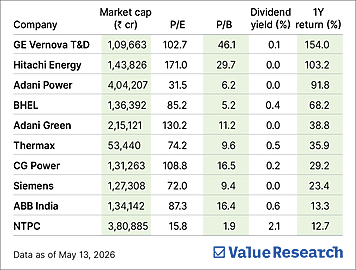

The index holds two distinct businesses. Traditional utilities, which include generators and transmission companies, benefitted first as DISCOM reform restored revenue collection, but improvement was gradual, constrained by regulated, capped returns.

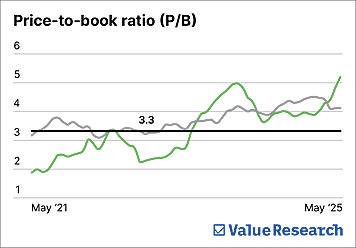

Capital goods companies such as transformer makers, switchgear manufacturers and engineering firms gained far more. A decade of suppressed demand released simultaneously into an underscaled supply chain meant revenue surged into a lean cost base, producing disproportionate profit growth. The market re-rated these companies sharply, from struggling industrials to long-term structural winners.

The 14-year gap between peaks was not incidental. Three things needed to converge: creditworthy customers, genuine demand growth and a sustained investment supercycle. When they did, the move was swift and significant.

This article was originally published on June 01, 2026.

Ask Value Research ![]()