Opening act

The year is 1978. Rajni Bector, a housewife, starts a home business and makes ice creams, puddings, and salads for weddings in and around Punjab and Haryana. And Mrs Bector's Food Specialities is birthed.

Fast forward to 2022. The same business now is the largest Indian supplier to quick-service giants, such as McDonald's, KFC and Burger King, and is a global brand supplying biscuits to over 63 countries. Not just that, its brands, English Oven, Cremica, and many others, are household names all across India.

A happy beginning indeed. But every movie needs a villain.

Enters Russia-Ukraine conflict.

Enters the villain

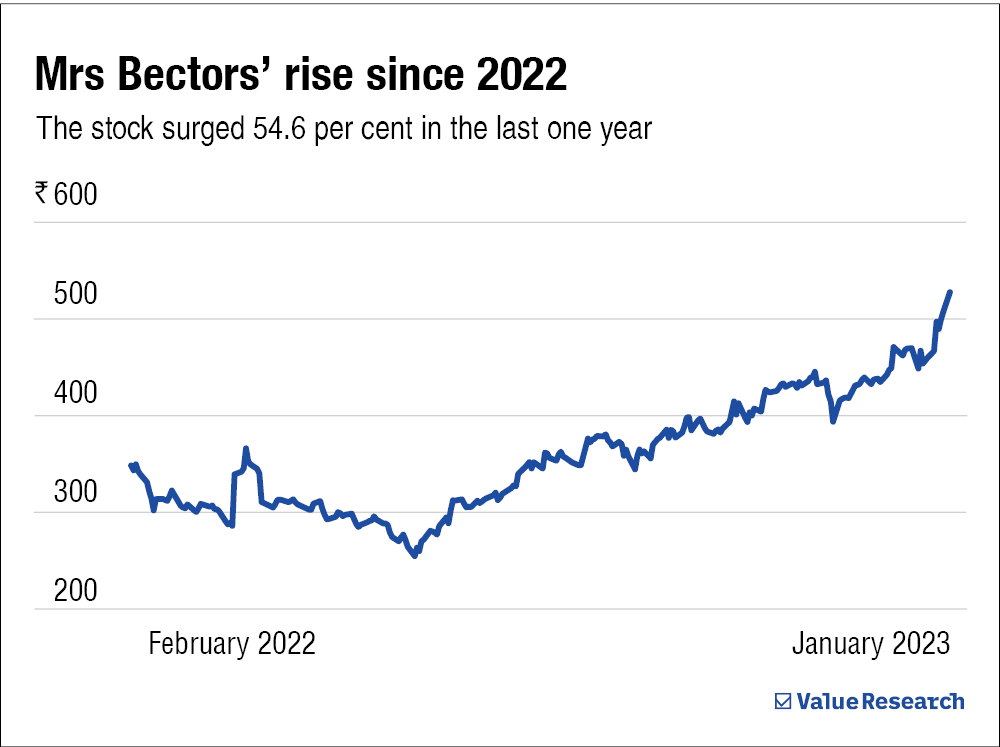

In 2022, the Russia-Ukraine conflict led to a rapid rise in raw material prices for food manufacturers like Mrs Bector. Its earnings took a hit, investors lost faith, and the stock went on a nosedive, hitting an all-time low in June 2022.

The comeback

So, is it time to roll the credits?

Never. What seemed like a sad drama might just turn out to be an inspiring comeback story.

As of February 13, 2023, the stock has more than doubled from its all-time low in June 2022.

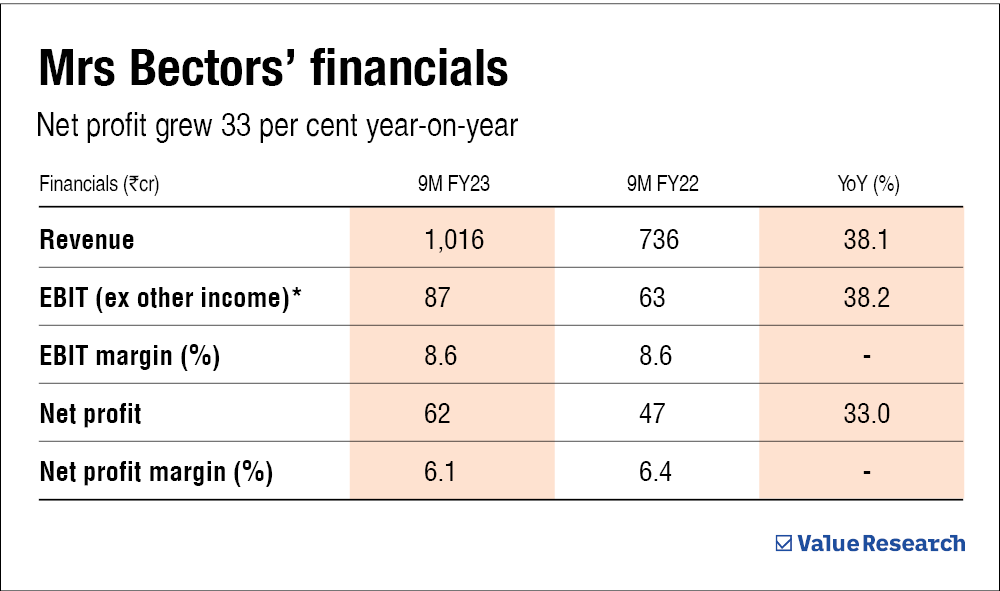

And it's not all just optics. The business's financials are stronger than ever. In the nine months of FY23, Mrs Bector's revenue from the biscuit and bakery segments jumped 34 and 47 per cent, respectively, compared to the same period previous fiscal. In fact, it reported its highest net profit margin in Q3 FY23.

There's more to the story

So far, so good. The worst is behind; the company has regained its momentum.

But the question remains. What lies ahead?

Here's why investors believe there might be a happy ending.

- Better distribution

The company is planning to foray into south and west India, where its presence is still relatively weak. Moreover, it is planning to double its direct outlet reach to 3,20,000 outlets by the end of FY24.

- New innovative products

Frozen buns, dessert jars and brownies - the company has a mouth-watering list of new products lined up. It has already captured the heart of many rusk lovers with its new product under the English Oven brand.

- Expansion plans

The company has approved a capex plan of Rs 22.5 crore for a bakery manufacturing facility in Alwar. A few more manufacturing facilities are being added in the Dhar region in MP and Maharashtra.

Our review

The story so far has been impressive, for sure. But only time will tell how the climax will be. If you are planning to invest, we advise you to do the due diligence on the company's fundamentals. And if you are not, stay tuned and keep the popcorn ready.

Suggested read: Is the worst over for Divi's?

Ask Value Research ![]()