Vinayak Pathak/AI-Generated Image

Vinayak Pathak/AI-Generated Image

Summary: Passive investing removes many decisions, but not all of them. This piece highlights how the choice of index influences both risk and return. It explores the trade-offs hidden behind seemingly simple investment strategies.

Spend enough time talking about investing and one particular view almost always comes up: someone will always announce they are switching to passive investing, no more stock-picking, no more fund manager dependency, just a simple index fund and a monthly SIP. The room nods approvingly. And that, almost always, is where the conversation ends. It rarely goes one step further to ask which index you should invest in.

For most Indian investors, the answer is the Nifty 50 almost by default. It is the oldest, the most recognised, the one whose number flashes on every news ticker. Choosing it feels like choosing the market itself. But the Nifty 50 is not the market. There are 50 companies. And how those 50 companies are arranged inside the index has consequences that most passive investors never pause to examine.

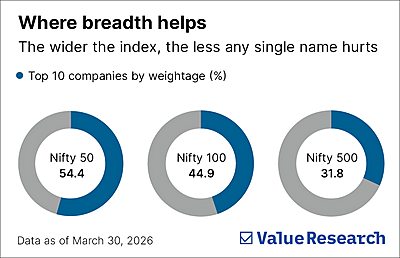

Half your money ends up in just 10 stocks

Here is a fact that tends to surprise people. The top 10 holdings of the Nifty 50 account for 54.4 per cent of the entire index. Every rupee you invest has more than 50 paise invested in just 10 businesses. If those companies go through a difficult few years, a regulatory change, a valuation reset after years of premium pricing, or simply a period of slower growth, your supposedly diversified portfolio will feel it acutely.

This is not a design flaw. It is simply how free-float market-capitalisation weighting works. Larger companies occupy more space and in a universe of just 50 stocks, the biggest names inevitably dominate.

Looking beyond the Nifty 50

The Nifty 100 and the Nifty 500, on the other hand, offer a somewhat different construction. The Nifty 100’s top 10 account for around 45 per cent of the index. The Nifty 500’s top 10 account for nearly 32 per cent.

To put that in perspective: in the Nifty 50, a single bad year for Reliance Industries or HDFC Bank moves the needle for your entire portfolio. In the Nifty 500, no single company, however large, carries that kind of weight. The portfolio’s fate is spread across 500 businesses, across sectors and market caps, across different stages of the economic cycle.

More importantly, the Nifty 500 is not simply a diluted version of the Nifty 50 with more names added. It gives you the stability of India’s largest, most established businesses, just like the Nifty 50, while also capturing the growth potential of mid- and small-cap companies. The established giants keep the portfolio grounded. The emerging ones give it room to compound faster.

Nifty 50 vs Nifty 100 vs Nifty 500

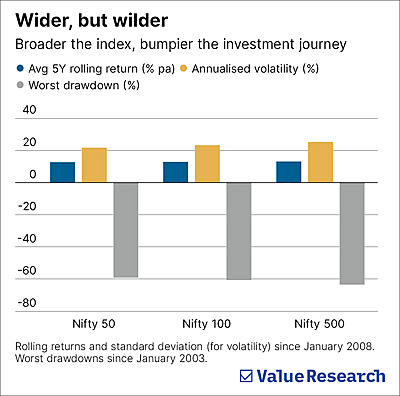

The Nifty 500 has delivered an average five-year daily rolling return of 13.2 per cent annually since January 2008. The Nifty 50 has delivered 12.7 per cent. That is a gap of 0.5 percentage points every year, in favour of the broader index. The Nifty 100 sits at 13 per cent.

That extra return, however, comes with a cost. The broader indices are more volatile. The annual volatility (measured by standard deviation) of the Nifty 500 and Nifty 100 based on one-year daily rolling return since January 2008 is 25.5 and 23.4 per cent, respectively, both higher than the Nifty 50’s 21.9 per cent.

The difference is simply that as broader indices expand to include more mid- and small-cap companies, daily price swings grow larger. This is not incidental. Mid- and small-cap businesses are inherently more sensitive to economic cycles, liquidity conditions and investor sentiment than their large-cap counterparts. Their earnings can swing more sharply. Their stocks can fall harder and faster when the mood turns. The volatility in the broader indices reflects this underlying reality.

The real test comes in downturns. The worst drawdown figures reveal what broader exposure means when markets turn ugly. Since January 2003, the Nifty 50 has fallen as much as 59.9 per cent from its peak at its worst point. The Nifty 100 fell 61.5 per cent at its worst. The Nifty 500 fell 64.3 per cent. Simply put, more mid- and small-cap exposure and less concentration in large caps have historically meant a deeper fall during severe market stress. Smaller companies with thinner balance sheets and less pricing power are hit the hardest when financial stress peaks and the broader indices absorb that fully.

There is no default answer

Passive investing removes many costly decisions. It spares you the guesswork of when to buy, when to sell, which fund manager to trust and which sector to chase. But one decision still remains: Which index should you own? And too often, that choice is made on autopilot, with investors defaulting to the Nifty 50 simply because it is familiar.

That is not always wrong. However, it has its own trade-offs. The Nifty 50 offers lower volatility and shallower drawdowns, but it is more concentrated. The Nifty 500 has delivered better returns but with sharper swings and deeper falls. The Nifty 100 sits somewhere in between. So, the takeaway is that passive investing may be effortless, but choosing the index should not be. Each one asks you to accept a different trade-off and a different reward.

This article was originally published on May 01, 2026.

Ask Value Research ![]()