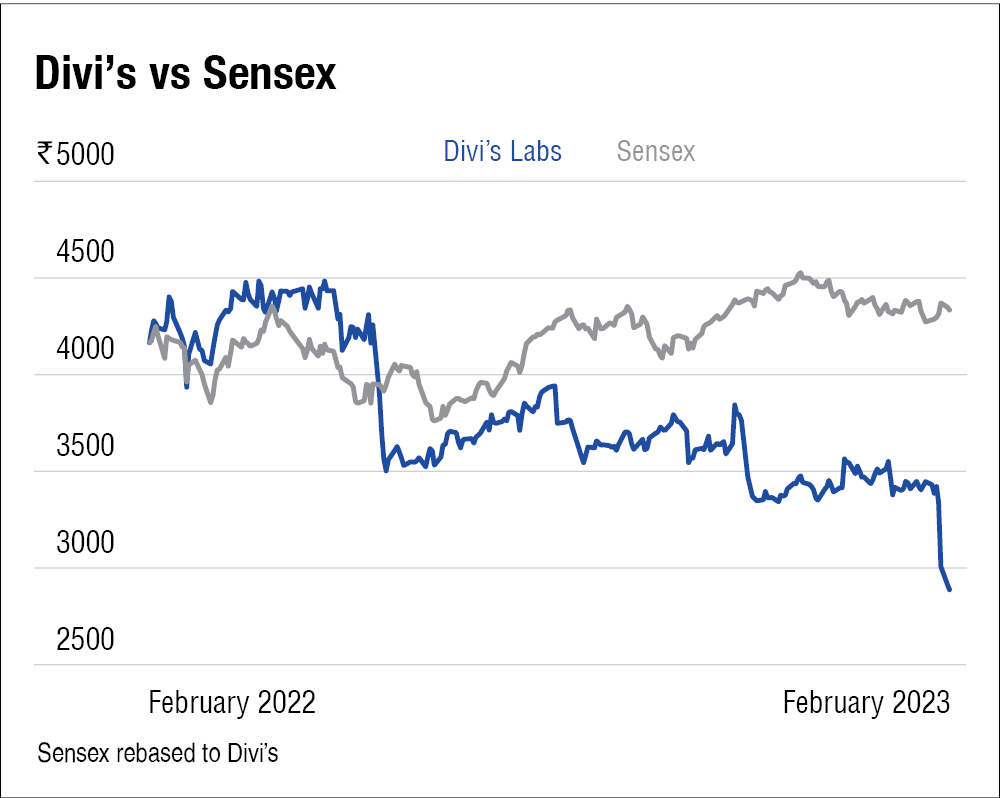

It's been on and off between the market and Divi's Laboratories. The stock has been one of the rising stars of the Indian Pharma space, posting negative returns in only two of the last 11 calendar years. Not just that, it has consistently maintained an operating margin higher than the industry median for the previous 10 years.

However, the market's love for Divi's has soured recently. After posting a fairly weak set of results in Q3, the market sent the stock tumbling, and it fell nearly 10 per cent on the result day, further wounding the already limping stock.

Here are the key factors that have left the Divi's bleeding.

The aftermath of COVID

Back in May 2021, when the pandemic was at its peak, US-based Merck selected Divi's laboratories to become the authorised manufacturer of API (active pharmaceutical ingredient) for the COVID drug 'Molnupiravir'.

And it soon became evident why Divi's was picked ahead of the bunch. Thanks to the company's scale, it could supply the API in large quantities, which shot up its revenue for the next few quarters.

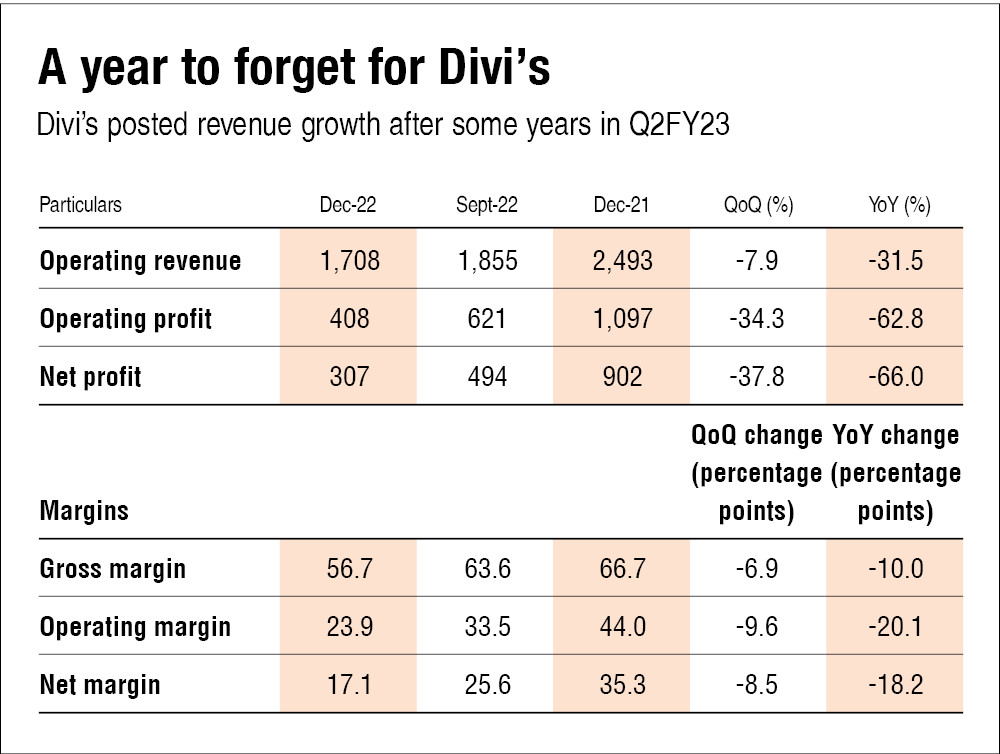

Everyone expected that once COVID subsided, there would be a dip in revenue (revenue fell seven per cent in Q2 and 31.5 per cent in Q3). Even Merck reported a 13 per cent decline in the sale of Molnupiravir.

However, what people did not expect was the drastic fall in gross margins.

When high cost meets pricing pressure

Before the company could recover its topline, it was struck with another blow to its bottomline. Prices of key raw materials, such as lithium, iodine and toluene, shot up, and to add to the injury, there was also a spike in energy costs.

Usually, during cost pressures, companies hike their prices, cushioning the impact on their margins. Unfortunately, on top of cost pressures, Divi's and many other pharmaceutical companies also had to deal with pricing pressure in generics. Combined, this led to a drastic fall in Divi's margins.

What the future might hold

The weak results last quarter did not do the stock any favours, and the market was at its ruthless best. However, it seems like the new year might mark a new beginning for Divi's.

The management has stated that the pricing pressure has eased in generics, and margins should improve in the quarters ahead. Volumes have also returned to double-digits. At the same time, raw material prices have returned to favourable levels.

Apart from the above, there are several growth opportunities on the horizon for Divi's.

Patent expiry opportunities: The management has stated that there's a $20 billion-plus opportunity from patent expiries. It has filed some applications for launches and will continue to file more.

Progress in iodine contrast media: Commercial production has started for two products, and considering its strong relationship with big pharma, it will start reaping the benefits from Q1FY24 onwards.

Custom synthesis: There are multiple opportunities in multiple therapies which don't have the pricing pressures of generics. Two fast-tracked custom synthesis projects are ramping up and will see revenue starting Q4 before full impact in Q1FY24.

Kakinada: Divi's has set a capex of Rs. 1,000 crore to invest in Kakinada. This facility could start production in stages before being fully completed over the next two to three years.

To sum up

This is not Divi's first downturn. After its fall in 2016 due to the USFDA notice, the company bounced back and gave 43 per cent returns pa in the next five years.

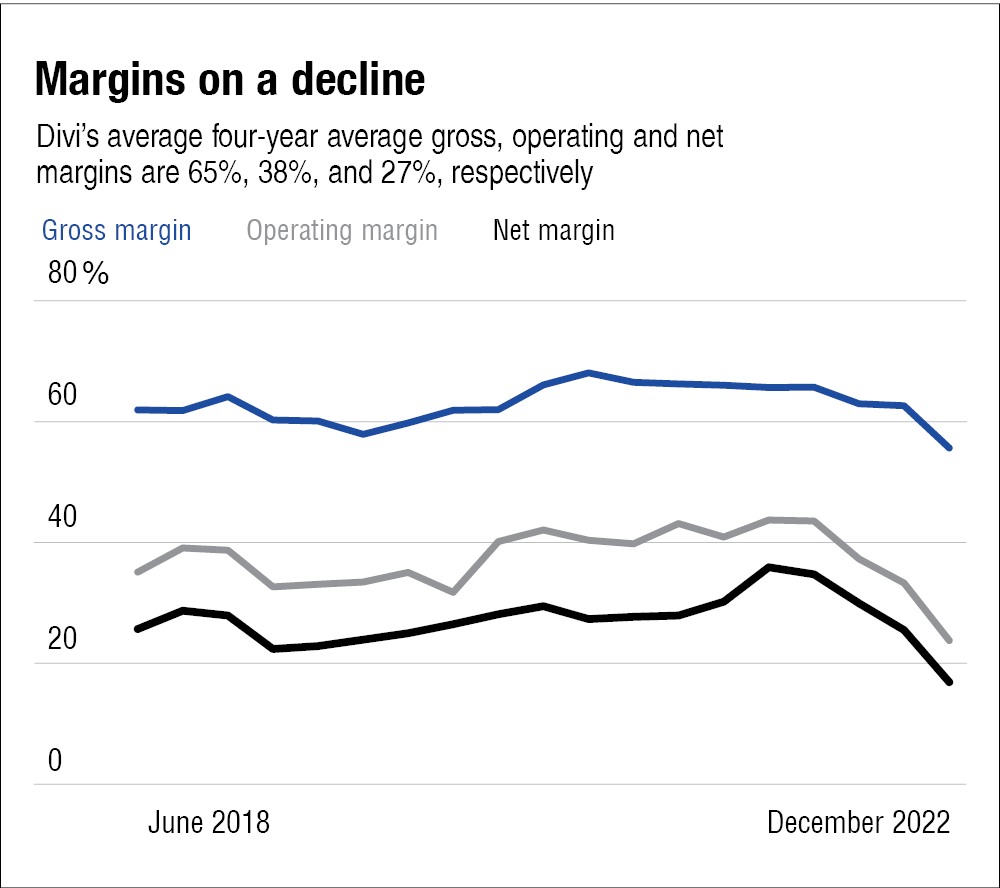

Having said that, there's no denying that the drop in gross margins would have deterred even the most ardent of believers. But those who found the strength to stick around do have enough to hope for a comeback, and the quarters ahead have some exciting opportunities.

But readers should note that this is not a stock recommendation. We request you do the due diligence before you decide to invest in any company. Always remember opportunities are the fuel. But without strong fundamentals, there is no growth engine.

Suggested read:

It's a no-go for Yes Bank

Investing lessons from the fall of Videocon

Ask Value Research ![]()