Efficiency, better returns, tax savings, smoother management - there are many pros to owning subsidiaries. However, they are no magic pills for better numbers.

While some entities look more attractive when viewed as a whole with their subsidiaries, some seem like they would be better off alone.

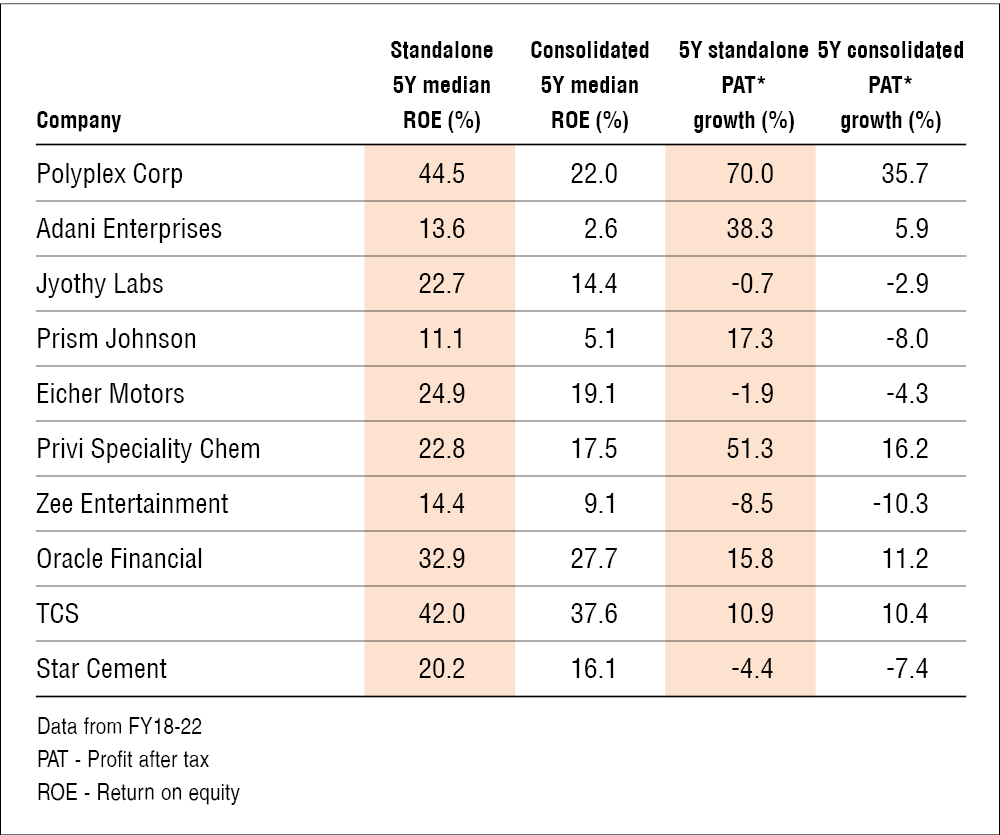

Take the example of the BSE 500 companies listed below. These companies are far more efficient (standalone 5Y median ROE > consolidated 5Y median ROE) and profitable (standalone 5Y PAT CAGR > consolidated 5Y PAT CAGR) than their subsidiaries. As a result, their individual performance looks far superior, and the subsidiaries are a drag on their consolidated numbers.

Similarly, these BSE companies seem far better when viewed from a consolidated perspective.

But this begs the question, what causes this disparity between the performance of the parent companies and their subsidiaries?

While it is true that the usual suspects, bad management and inefficient capital allocation, can ruin the party, the answer is often not as simple as "the subsidiaries are mismanaged."

Here are some factors that can lead to subsidiaries bruising the consolidated performance.

Different products need different levels of capital allocation: A parent and its subsidiaries might operate in the same industry, such as FMCG, but have a diverse range of products. For example, Dabur India deals in skincare, haircare, oral care products and more. However, each product requires different capital allocation and decision-making levels, which inadvertently leads to significant variations in the performance of subsidiaries.

Geographical variations: Even if the subsidiaries deal broadly in the same products, if they operate from different geographies, the economics of operating the same business in different geographies may vary.

Conglomerates: At times, the parent and its subsidiaries operate in completely different segments, and this is especially true for conglomerates like Adani Enterprises. Unsurprisingly, the subsidiaries operating in capital-intensive segments end up impacting the consolidated performance of the parent.

To sum up, subsidiaries can indeed be a double-edged sword. While some might add value to the conglomerates, some might be baggage. New acquisitions and new subsidiaries are often a positive move. However, investors should still be vigilant and assess if they would actually benefit the parent company in the long run.

There's a reason why the markets favour organic growth rather than inorganic growth fueled by random acquisitions.

Suggested read: Why financial leverage is a double-edged sword

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()