It is important for us to ensure the smooth transfer of all our assets and investments to our loved ones in our absence. Although financial and legal experts suggest having an estate plan in place, we hardly pay attention to it. But life is full of uncertainties. The recent devastating second wave of COVID has proved the fact again.

Obviously, we don't want our loved ones to face any hardship while getting ownership of the investments and assets that we have built over the years. The least we can do is to devise a plan and ensure the smooth transition of our investments and assets in our absence. Here is a step-by-step guide to help you.

1. List all your visible assets

Start with making a simple list of what all you would like to be transferred to your loved ones in your absence. To keep things simple, start with all your tangible assets, like your investments in real estate - a house, a piece of land or probably any commercial establishment that you have purchased.

Don't forget to add all the valuables that you have, such as jewellery, an expensive car or bike or any of your belongings that you want to be transferred after your death.

2. Add your financial assets to the list

The list does not end with physical assets. Irrespective of purposes, we all save and invest. Even if one doesn't have any investments in mutual funds, shares or fixed deposits, everyone has a bank account. Any such money can be of great use to your loved ones in your absence, especially if they are financially dependent on you.

List down all your bank accounts and financial investments, no matter how small the amount is.

3. Outstanding loans

The hard reality is that the money that we owe needs to be repaid even if something happens to us. Just take the example of an outstanding home loan. If something happens to the breadwinner, the bank usually sells the house to recover the outstanding loan amount. Precisely this is where insurance comes in handy. We will discuss it in the next step but for now, just list down all your outstanding loans and open credit cards.

4. Life-insurance policies

Continue the list with all the life insurance policies that you have purchased. At the same time, make sure that you have adequate cover to meet all the outstanding loans and take care of the essential financial goals of your loved ones who are dependent on you. Quite often, a separate insurance policy is sold by the bank when you take a big-ticket loan like a home loan to cover it. Do mention such policies in the list with a clear indication that it has been linked with the said loan.

5. Write down all essential details

By now, you are mostly done with listing down all the important things that would be transferred to your loved ones in your absence. However, just mentioning the names may not be of great help.

Draw a few columns in the same list and provide all the necessary details that they may require. The account numbers, the folio numbers, the address of the real-estate investments, contact details of the organisation with which you have invested your money or have taken a life insurance policy. Likewise, collect the essential documents - the policy bond in the case of life insurance; ownership papers of the physical assets and so on.

You should also mention the details of your financial advisor (if any) and the insurance agent (if any) who can help your family members in your absence.

6. Review and update the nominee

A nominee refers to the person whom you would want to receive the asset or money in your absence. For example, if something happens to the account holder or a person who has invested in mutual funds, the amount/ investment will be transferred to the nominee. Registering a nominee makes it much easier for loved ones to claim the money in your absence. In that case, they just need to give proof of their identity, the death certificate of the investor and submit a simple request form and that's all. So, just think about a beneficiary for each of your assets and get it updated in the records of the organisation wherein you hold the investment or the bank account. You can also mention this in the list prepared by you in a separate column.

What happens if a nominee is not registered?

Claiming the money or investment after the death of the investor could be a herculean task if the nominee is not registered.

According to the website of the Association of Mutual Funds of India (AMFI), if a nominee is not registered, the claimant has to provide an individual affidavit from each of the legal heirs, mentioning that they do not need the stated investment and can be given to the claimant. Besides, the claimant is required to submit either a notarised copy of a will certified by the court, succession certificate or the court order if the investor dies without any will. The condition of a will or a court order may be relaxed if the investment value does not exceed Rs 2 lakh. However, each legal heir may be required to sign an indemnity bond, stating that if there is any dispute in future, the stated legal heirs will take the responsibility and the fund house will not be liable for the same. Also, the claimant needs to prove his/her relation with the investor through any document.

All these requirements are in addition to the usual procedure that generally demands a transmission request in a particular format (issued by the AMC), the death certificate of the investor and the KYC of the claimant.

Likewise, the website of State Bank of India mentions a somewhat similar set of documents - a copy of the certified will/court order, etc. If the investor dies without any will, the bank will require a letter, along with an affidavit, from each legal heir.

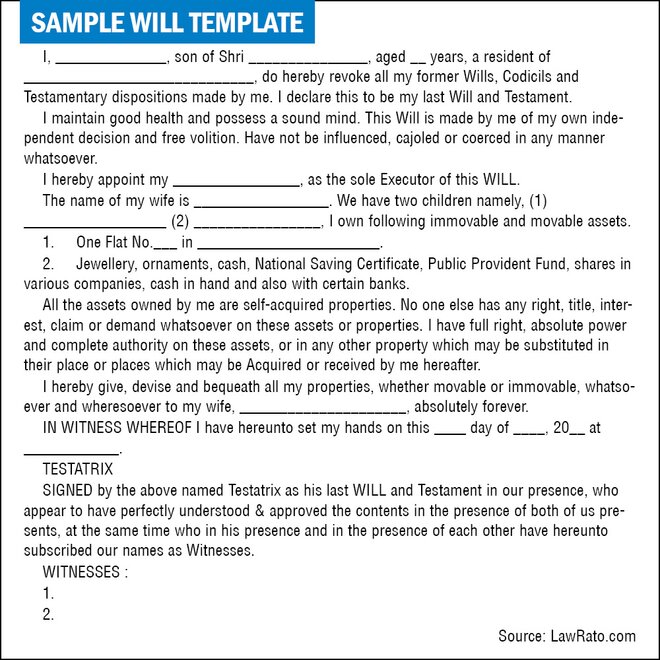

7. Make a will

The nature of human psychology is such that subconsciously, we connect the word 'will' with the deathbed. However, that should not be the case. It is an important document that we all must prepare. One can register the nominee for a financial asset as we discussed. When it comes to tangible assets like an expensive car, jewellery, house or a piece of land that you own, there is no provision for a nominee. In such cases, you can transfer all these assets by creating a 'will'. Moreover, by law, a 'will' supersedes the nomination.

How to make a will

While one always has the option to hire a lawyer to create a will, it is no rocket science. It can be as simple as writing on a plain piece of paper at home - which asset you want to be succeeded by whom. It doesn't even have to be necessarily on a stamp paper. While writing a will, one should broadly follow the following format to avoid any ambiguity.

Self-declaration: The will should ideally start with your personal details, including name, age, address and father's name followed by a declaration that it is being made in full senses and without any kind of pressure. Further, it should mention that this is the latest will and the previous ones do not hold any relevance. One may also include one's Aadhar number or any such identity issued by the government to make it more supportable.

Choose an executor: Think of a trustworthy person who will execute your wish in your absence and provide his/her details. The executor can be a beneficiary or a third person. The purpose here is to inform a trustworthy person about the will and where you have kept all the important documents. It will ultimately help him/her execute your wish and get the assets transferred to the loved ones in your absence.

Details of your assets and investments: Here one should mention the details of all the assets and investments that were listed in the initial steps and that you would like to be succeeded by your loved ones.

Mention who would own what: Now, clearly mention which asset or investment you would like to be succeeded by whom and in what proportion. Here you may also mention the way you would like it to be utilised by the successor. For example, if you want the successor to utilise a sum of money for any particular purpose, say for a charity or something of that sort, mention it here. All the outstanding liabilities can also be included here with the plan that you have for them.

Sign in the presence of two witnesses: The last step should be to sign on each and every page of the will along with the date and place. Do remember that this signature should be done in the presence of two witnesses to make the will legally valid. These witnesses should not be a direct beneficiary and can be anyone, your friends or neighbour. Basically, they are required to certify that the will was made in their presence by you without any external pressure.

Alternatively, one may also use the internet to create a 'will'. These days, many websites are helping people create their will. One doesn't have to worry about the format here as these websites are designed in a way that they ask simple questions from the users like - what assets do you own, to whom you would like to get them transferred and so on. And then, these websites create a will in an acceptable format.

Is it mandatory to register a will with the court?

One doesn't have to register a will with the court. However, doing so is recommended if one feels that there may be a dispute within the beneficiaries or someone who is not a beneficiary may claim a stake. However, one must remember that even a registered will can be challenged in a court of law. If one decides to register a will, a copy should be kept safely with the registrar.

The final step

Keep all the documents and a copy of the will in a safe deposit locker and make sure that the executor knows about the place. Also, it is important to review and update the list and the will periodically, say every year or whenever there is a significant change in your assets and investments. For example, if you purchase a new house, it is time to update your will, as the older one created by you may not have included this house.

This article was originally published on December 02, 2021.

Ask Value Research ![]()