Devyani International is the largest franchisee of Yum Brands in India and is among the largest operators of quick-service restaurants (QSR) in India. The company primarily operates three international brands:

KFC: A global chicken restaurant brand with over 25,000 outlets in over 140 countries. The company operated 284 KFC stores as of June 30, 2021.

Pizza Hut: One of the largest pizza chains in the world with over 17,000 restaurants. Devyani International operates 317 Pizza Hut stores in India.

Costa Coffee: A global coffee chain under which the company operated 44 stores in India as of June 30, 2021.

The company also operates KFC and Pizza Hut stores in Nepal and Nigeria. It refers to these brands (KFC, Pizza Hut, and Costa) as its 'core brands,' which contributed to more than 94 per cent of its revenues in FY21. Apart from these, the company also owns and operates brands such as 'Vaango' and 'Food Street.' All combined, the company operates 696 stores across 166 cities in India as of June 30, 2021.

Strengths

- The company collaborates with its international franchisor Yum! Brands for product innovation and development, brand strategy, and technology initiatives.

- The company operates in an industry that has witnessed growth and is expected to grow in the future as well. As per the GlobalData report, the QSR segment will continue to lead the foodservice sector, and the sales value of the QSR channel is expected to grow at a CAGR of 12.4 per cent from 2020 to 2025.

- The company follows a cluster-based approach and has a strong presence in key metro regions of Delhi-NCR, Bengaluru, Kolkata, Mumbai, and Hyderabad, with close to 50 per cent of its stores in these five regions.

- The company operates stores in strategic locations such as airports, high street locations, malls, food courts, business hubs, and transit areas. It also looks to open new stores for KFC and Pizza Hut in close proximity, allowing it to reduce capital costs related to store construction and logistics costs towards the supply of raw materials to both stores.

Risks

- Many of the company's core brand outlets have a dine-in model, which has taken a hit due to Covid-19. Dining-in revenues declined from Rs 542 crore in FY20 to Rs 284 crore in FY21.

- Majority of the stores are operated on leased properties and are exposed to market conditions of the rental market.

- The company's auditors had raised material uncertainty related to going-concern on audited financial statements for FY19.

- The company has a very high level of attrition which stood at 40.1 per cent at the corporate office and 73.6 per cent in stores as of FY21.

IPO questions

The company/business

1. Are the company's earnings before tax more than Rs 50 cr in the last twelve months?

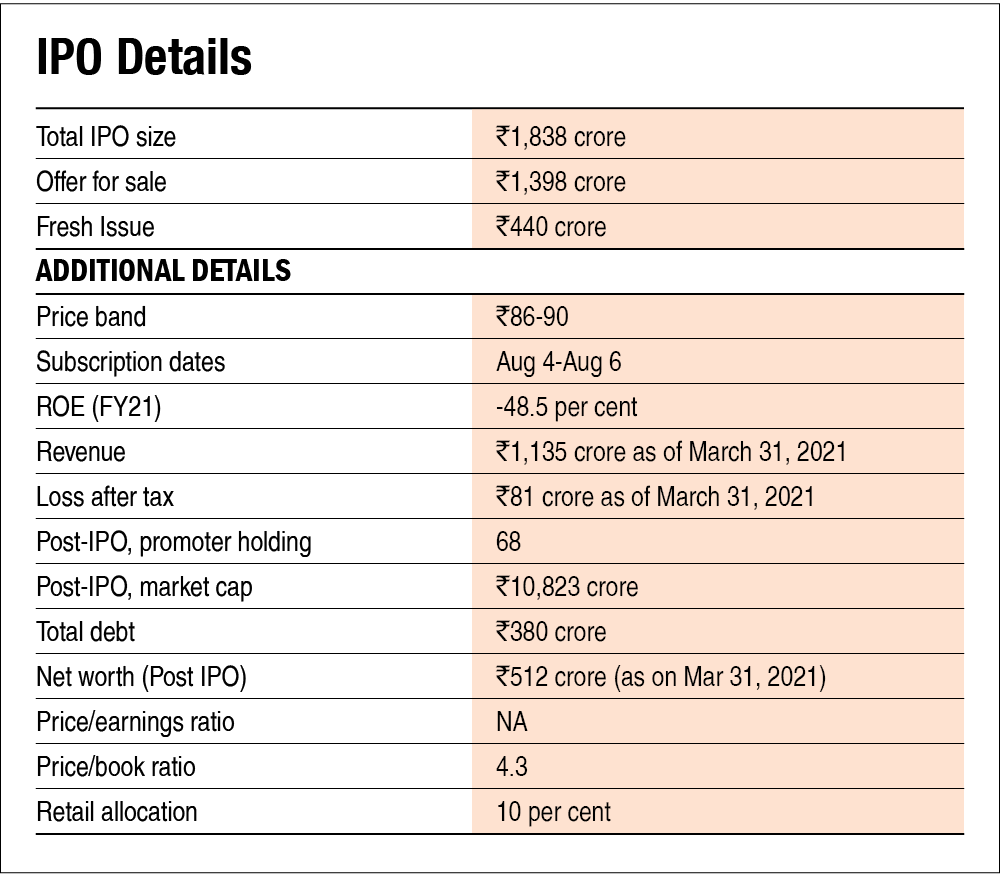

No, the company has reported a loss of Rs 82 crore in FY21.

2. Will the company be able to scale up its business?

Yes, the company has been expanding its core brand stores at a CAGR of 13.6 per cent from 469 stores in FY19 to 605 stores in FY21 and plans to increase its store network following its cluster approach and penetration strategy.

3. Does the company have recognisable brand/s, truly valued by its customers?

Yes, the company operates a franchisee chain of globally renowned brands such as KFC, Pizza Hut, and Costa Coffee.

4. Does the company have high repeat customer usage?

No. Though FY20 and FY21 have been exceptional years due to the pandemic, the company's stores have historically witnessed very low same-store sales growth compared to its other peers.

5. Does the company have a credible moat?

Yes, the company is the largest franchisee of the Yum! Brands (KFC and Pizza Hut) in India, Nepal, and Nigeria.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

No, the company is subject to a broad range of food and safety regulations.

7. Is the business of the company immune from easy replication by new players?

Yes, the company has a large chain of quick-service restaurants in India which might not be easy to replicate by new players.

8. Is the company's product able to withstand being easily substituted or outdated?

No, the company operates in the Food and Beverage industry, which is highly competitive, and products can be easily substituted.

9. Are the customers of the company devoid of significant bargaining power?

No, as stated above, the company operates in a highly competitive industry, and customers of the company have many options to choose from.

10. Are the suppliers of the company devoid of significant bargaining power?

Yes, the company sources its raw materials from vendors that are pre-approved by the franchisor and meet international safety and quality standards.

11. Is the level of competition the company faces relatively low?

No, the company operates in a highly competitive foodservice industry with a lot of players.

Management

12. Do any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than 25 per cent stake in the company?

Yes, the company's promoter will continue to hold 68 per cent stake in the company post-IPO.

13. Do the top three managers have more than 15 years of combined leadership at the company?

Yes, Rajat Luthra, CEO of KFC, and Amitabh Negi, CEO of Pizza Hut business, have a total combined experience of 15 years with the company.

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with Sebi guidelines?

Yes, we have no reasons to believe otherwise.

15. Is the company free of litigation in court or with the regulator that casts doubts on the intention of the management?

No, there have been litigations against the promoters of the company Ravi Kant Jaipuria and Varun Jaipuria in their capacities as directors on the board of Varun Beverages.

16. Is the company's accounting policy stable?

Yes, we have no reasons to believe otherwise.

17. Is the company free of promoter pledging of its shares?

Yes, the promoter's shares are free of any pledging.

Financials

18. Did the company generate the current and three-year average return on equity of more than 15 per cent and return on capital of more than 18 per cent?

No, the company has been reporting losses in the last three years and had negative equity in FY19 and FY20. However, the current and three-year average return on capital stood at 3 per cent and 16.4 per cent, respectively.

19. Was the company's operating cash flow positive during the previous three years?

Yes, the company reported positive cash flow from operations in the last three years.

20. Did the company increase its revenue by 10 per cent CAGR in the last three years?

No, the company's revenue fell from Rs 1,310 crore in FY19 to Rs 1,135 crore in FY21.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest-coverage ratio more than 2?

No, the company's interest coverage ratio stood at 0.08 in FY21.

22. Is the company free from reliance on huge working capital for day-to-day affairs?

Yes, the company has a negative working capital cycle of 28 days, wherein it receives payment well before it has to pay to its suppliers.

23. Can the company run its business without relying on external funding in the next three years?

No, the company has been reporting losses and plans to use the fresh issue from the IPO to repay debt. Thus, the company might have to rely on external funding in the future to open new stores.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

Yes, the company's short-term borrowings have decreased from Rs 68 crore in FY19 to Rs 21 crore in FY21.

25. Is the company free from meaningful contingent liabilities?

No, the company's contingent liabilities are more than its equity and stand at Rs 76 crore as of FY21.

The stock/valuations

26. Does the stock offer an operating-earnings yield of more than 8 per cent on its enterprise value?

No, the stock will offer a yield of 1.2 per cent post IPO based on March 2021 numbers.

27. Is the stock's price-to-earnings less than its peers' median level?

NA. Since the company is loss-making, P/E ratio is not applicable.

28. Is the stock's price-to-book value less than its peers' median level?

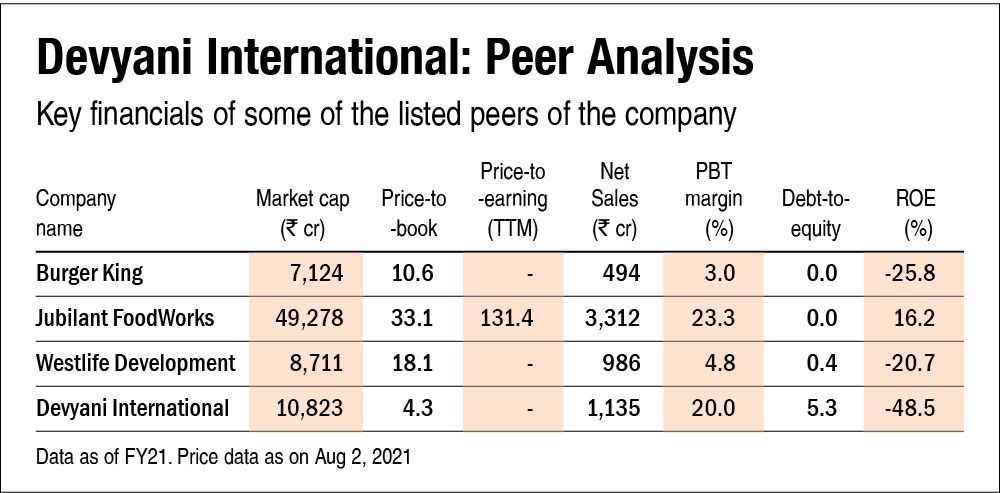

Yes, the stock's P/B ratio stood at 4.3, which is less than its peers' median level of 18.1.

Disclaimer: The authors may be an applicant in this Initial Public Offering.

Ask Value Research ![]()