Ujjal Das/AI-Generated Image

Ujjal Das/AI-Generated Image

Summary: The market fell 1,092 points in the last thirty minutes of Friday. Within minutes, a viral explanation named the culprit. It was wrong. And if you sold because of it, you sold for the worst reason there is.

On Friday, 29 May, the market did almost nothing for six hours, then fell hard in the last thirty minutes. The Sensex dropped 1,092 points to close at 74,775, down 1.44 per cent. About Rs 6 lakh crore of market value disappeared, most of it in that final half hour.

Within minutes, an explanation went viral: MSCI had cut India's weight, foreign funds were fleeing, the world had lost faith in India. It was a frightening story, and it was wrong. If you sold because of it, you sold for the worst reason there is — a panic built on a misreading. Here is what actually happened, and why it should not change a thing you do with your money.

First, what an MSCI rebalance is

MSCI revises those lists, and on the day a change takes effect, every fund tracking the index must buy the new entrants and sell the leavers. The trading is automatic. It says nothing about whether a company is good or bad, or whether India is trusted.

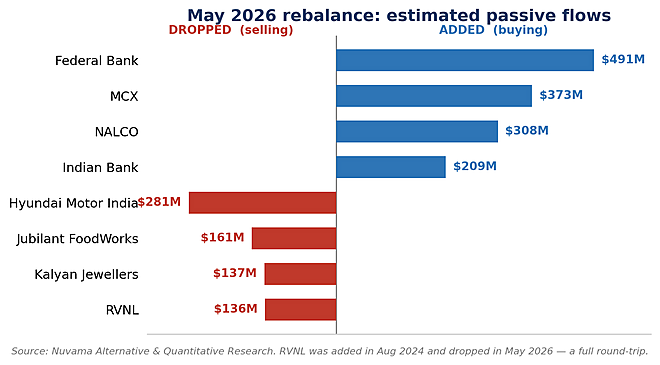

This May, MSCI added four Indian shares and removed four. India's overall weight hardly moved, from 12.4 to 12.3 per cent, and the number of Indian shares stayed at 165. The claim that MSCI had slashed India's weight was simply untrue. The list was published on 12 May and took effect at the close on 29 May, 17 days' warning, no surprise in it.

On one day, funds bought four shares and sold four others. That is the whole event.

Why was the forced selling small

Start with what the rebalance can and cannot move. When MSCI drops a share, the only investors forced to sell are the index funds that must mirror the list. Active foreign funds may sell or may not; everyone else simply watches. So the forced selling is never the company's whole foreign holding. It is a slice of a slice — the part held through funds that track the index.

Look at the four shares MSCI dropped, with the foreign holding each carried into the event:

| Dropped share | Foreign holding | Forced exit selling |

|---|---|---|

| RVNL | ~5% | a fraction of it |

| Hyundai Motor India | ~5% | a fraction of it |

| Kalyan Jewellers | ~15% | a fraction of it |

| Jubilant FoodWorks | ~18% | a fraction of it |

| Foreign (FPI) holding from the companies' latest disclosed shareholding patterns, NSE/BSE. Only the index-tracking portion of that holding trades on an MSCI exit. | ||

Foreign (FPI) holding from the companies' latest disclosed shareholding patterns, NSE/BSE. Only the index-tracking portion of that holding trades on an MSCI exit.

Foreigners owned about 5 per cent of RVNL and about 18 per cent of Jubilant FoodWorks. But only the index-tracking part of those stakes was forced to move on 29 May — and nobody, not even the index trackers themselves, publishes that exact figure. Brokerages estimate the total forced outflow across all four exits at roughly $800 million to $1 billion, about Rs 8,000 crore. Set that against the Rs 6 lakh crore the whole market lost that day, and the MSCI piece is a rounding error. That we cannot pin the number more precisely is the point: it is too small and too buried to matter to a long-term investor.

So what drove the fall? Several things at once. Crude oil rose above $104 a barrel, and India buys about 85 per cent of its oil abroad. Goldman Sachs cut its 2026 growth forecast for India to 5.9 per cent. The weather office warned of a below-normal monsoon. A fragile US–Iran situation kept traders nervous, and many cut risk before the weekend. Foreign investors did sell heavily that day — far more than the rebalance alone explains, and for these macro reasons, not the index reshuffle. The rebalance simply landed on top of it all, at the one moment when index funds are forced to trade. That is why a dull session ended in a sharp half hour.

Indian institutions, for their part, did not run. Provisional exchange data showed domestic funds were heavy net buyers that day, absorbing most of the foreign selling. Forced selling met willing buying — not a country being abandoned.

The part the panic got half-right

The frightened posts were pointing at something real. India's weight in the MSCI Emerging Markets index has fallen sharply, from a peak near 20 per cent in September 2024, when India briefly overtook China, to under 12 per cent now — a six-year low. Some blamed taxes, the weak rupee and a drift toward subsidies over investment. Those are fair worries about India's long-run appeal. But they did not pull this number down.

India's slide is mostly a story about other markets rising, not India falling apart.

The real cause is the global rush into artificial intelligence and the chips that power it. Money has poured into Taiwan and South Korea, home to the world's big chipmakers. Taiwan now accounts for about a quarter of the index, and one company, the chipmaker TSMC, carries more weight than all of India's shares put together. India's market is built on banks, consumer goods, and software services, with little chip manufacturing to offer. So as the AI shares soared, India's slice shrank by comparison. Indian companies did not get worse; the index simply tilted toward the excitement.

That tilt carries a warning of its own, though not the one the panic had in mind. An index now packed with a few AI names — its top ten companies make up more than a third of it, is narrower and more fragile than it looks. The real risk sits in the markets that rose, not the ones that fell.

We have watched this film before, running backwards

Eighteen months ago, the same machine ran the other way. Through 2024, each MSCI review lifted India's weight to a fresh record and brought billions of dollars of index buying, and the headlines spoke of a structural rerating of Indian shares. Yet despite all that buying, MSCI India still fell about 16 per cent in dollar terms over the following months. The flows followed the price; they did not set it.

One share tells the whole story. RVNL was added to the index in August 2024 to applause and a wave of index buying. This May, it was dropped. The same share, the same index, a full round trip in twenty-one months. An investor who bought it because MSCI added it, then sold it because MSCI dropped it, traded on noise both times and paid for the privilege twice.

What you should do

Nothing on this news. An index reshuffle is not a signal to buy or to sell; a share is not better because MSCI added it, nor worse because MSCI removed it. Think of an index weight as a thermometer: it reads the market's temperature, it does not cause the fever. If you hold a sound equity fund through a monthly SIP, the right answer to a closing-bell drop driven by index plumbing is to carry on. On Friday, the headline was loud, and the event was small. Knowing the difference is what keeps your money working while others sell in the dark.

Ask Value Research ![]()