Vinayak Pathak/AI-Generated Image

Vinayak Pathak/AI-Generated Image

Summary: The funds that sat on high cash piles in the previous bull run are no longer sitting idle. As valuations cool, many of them have started buying again. We reveal which funds are deploying cash, why this shift matters, and how investors should read this signal.

Indian equities were on a dream run until late September 2024. Broad markets had delivered stellar returns with the Nifty 500 TRI clocking around 22 per cent per annum in the previous five years.

But soaring markets often come with a side effect: expensive valuations. By then, the Nifty 500 was trading above its three-year and five-year average P/E ratios. For many fund managers, that meant fewer bargains to chase and more temptation to hold cash while waiting for better opportunities.

But the mood has changed. As markets have cooled off and volatility has returned, the majority of equity funds that had the highest cash allocations before the correction are now deploying their idle money again.

Tracking the cash hoarders

Of the top 10 equity funds that had the highest average cash holdings in the six months before the correction, most have decisively reduced their cash pile in the six months ending March 2026. See the table below.

Note that for this exercise, sectoral and thematic funds, and those less than a year old, were excluded.

Most cash-heavy funds are now light

Six of 10 funds with the highest pre-correction cash buffers now sit on a slimmer pile

| Fund | Apr'24 to Sep'24 (%) | Oct'24 to Mar'25 (%) | Apr'25 to Sep'25 (%) | Oct'25 to Mar'26 (%) | April'26 (%) |

|---|---|---|---|---|---|

| Parag Parikh ELSS Tax Saver | 16.9 | 18.6 | 15.9 | 11.7 | 4.4 |

| Parag Parikh Flexi Cap | 16.7 | 21.9 | 23.6 | 21.6 | 15 |

| Quantum ELSS Tax Saver | 14.3 | 15.1 | 12 | 7.3 | 5.6 |

| Quantum Value | 13.5 | 14.1 | 12.1 | 6.9 | 6.5 |

| ICICI Prudential Value | 12.2 | 9.4 | 8.3 | 5.9 | 6.2 |

| Motilal Oswal Midcap | 12.1 | 16.1 | 18.3 | 8.6 | 4 |

| LIC MF Children's | 12 | 12.6 | 13.2 | 15.5 | 17.8 |

| ICICI Prudential Smallcap | 11.2 | 14.3 | 12.9 | 4.7 | 4.5 |

| HDFC Focused | 10.1 | 13.2 | 12.7 | 10.5 | 7.5 |

| Motilal Oswal Flexi Cap | 10.1 | 14.2 | 12.7 | 13.3 | 1.7 |

| Top 10 funds by average cash allocation between April and September 2024. Analysis includes active funds across all equity categories as classified by Value Research, excluding sectoral/thematic funds. Funds with less than one year of history as of September 30, 2024 were excluded. Cash positions were tracked from October 2024 to April 2026, broken into six-month windows. The last window only has April 2026 as of now, as it will be completed in September 2026. | |||||

From the table, one can see that the most evident reduction in cash holdings has only occurred in recent months, especially between October 2025 and March this year, when equity markets suffered sharp declines, paving the way for better valuations.

How valuations influenced these moves

To examine this, we widened the analysis beyond just the top 10 funds. This time, we looked at funds that had an average cash holding of over 7.5 per cent in the six months prior to the fall, i.e., between April and September 2024.

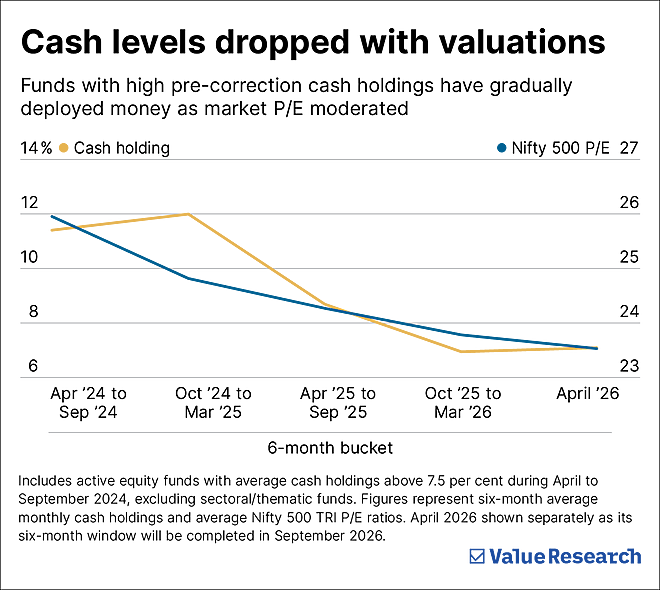

As the graph below shows, these funds have seen their average cash holdings fall in line with the market’s declining P/E ratio.

As markets got cheaper, cash levels declined

Funds with high pre-correction cash holdings have gradually deployed money as the market P/E moderated

Includes active equity funds with average cash holdings above 7.5 per cent during April to September 2024, excluding sectoral/thematic funds. Figures represent six-month average monthly cash holdings and average Nifty 500 TRI P/E ratios. April 2026 will be shown separately as its six-month window will be completed in September 2026.

The Nifty 500’s average P/E, above 28 times at its September 2024 peak, was down to 23.8 times in the October 2025 to March 2026 window. Over the same period, the average cash holding of these funds slid to its lowest level in the entire 18-month stretch.

Of course, this does not automatically mean that fund managers were only reacting to lower valuations. Cash calls can be influenced by several factors, including market outlook, stock-specific opportunities, or risk management preferences. But the broad direction does suggest that many managers became more willing to deploy money as markets cooled.

This is the time to put money to work

Fund managers appear to be doing what every sensible investor should do. They held back when valuations were stretched and are now deploying money when prices have cooled.

That is the real lesson. Corrections are not just periods of pain. They are also periods of opportunity. If your goals have a long horizon, this is not the time to freeze or pause. It is time to invest without compromising on quality.

That is where Value Research Fund Advisor can help you. Our analysts study fund portfolios, track long-term records, risks, costs and consistency to recommend funds that are truly worth holding for your goals.

So make use of the current downturn and start investing now.

Ask Value Research ![]()