Summary: Silver ETFs have gone from quiet to frenzied in a year. Volumes have exploded. Prices have surged. But here’s the catch: when demand runs ahead of value, investors can overpay without realising it. This piece explains what to check before you click ‘buy’.

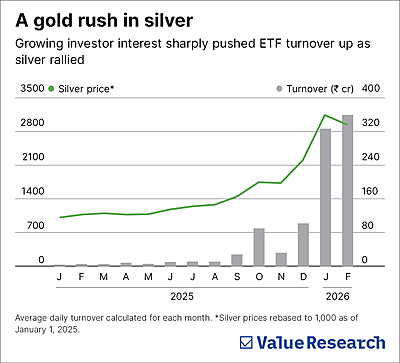

A good way to gauge how ‘hot’ an asset is at any moment is to consider its trading activity. As volumes jump, what once may have been a quiet corner of the market instead becomes a noisy, one-way trade. That is exactly what has happened with silver or more precisely silver ETFs.

Over the past year, turnover in silver ETFs (total value bought and sold daily) has exploded. In January 2025, average daily turnover sat at Rs 4 crore and a year later, it is Rs 327 crore. One obvious reason was the metal’s rally. And another was the convenience of ETFs (that can be bought from an exchange just like any share), which made them an investor favourite.

High activity however, becomes a problem even in simple instruments like ETFs when excess demand pushes prices away from the actual value of the underlying metal.

Price is not always value

An ETF has a net asset value or NAV. That is the per-unit value of the assets the fund holds. Then there is the trading or market price on the exchange at which the ETF is bought or sold.

In an ideal world, the market price should sit very close to the NAV. Yet in periods of frenzy, a divergence appears. When demand spikes suddenly, buyers often accept higher prices just to get in quickly. That pushes the ETF above its NAV and results in a premium.

When sellers dominate, prices slip below NAV and result in a discount. In simple terms, you end up paying more than the silver held by the ETF is worth. Or selling it for less. Both are distortions but they do not hurt investors equally.

How buying at premiums wrecks your returns

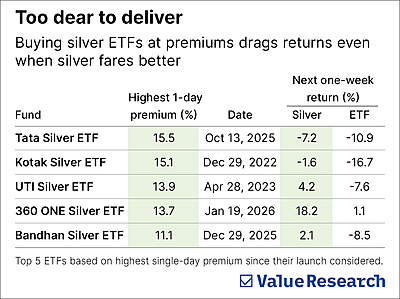

Premiums are the bigger danger because they are self-inflicted. You choose to overpay.

Here’s how they hurt: We examined the five silver ETFs with the highest-ever one-day premiums and compared their one-week returns from those dates with silver’s performance over the same period.

The results in the table ‘Too dear to deliver’ show how buying at a steep premium wipes returns even when silver itself performs well. The 360 ONE Silver ETF, for instance, traded at around a 14 per cent premium. Over the next week, silver rose 18 per cent. But the investor who’d have bought the ETF at that inflated price earned only about 1 per cent. The missing return did not vanish into thin air. It was simply the premium collapsing back towards NAV.

That is the key point. When excitement cools, the gap between fair and market value tends to close. The investor who paid too much watches part of silver’s gain get used up in repairing the entry mistake.

This is why silver ETFs can disappoint even in a rising silver market. If you pay above the NAV, that excess becomes a permanent drag on returns.

Discounts sting, but temporarily

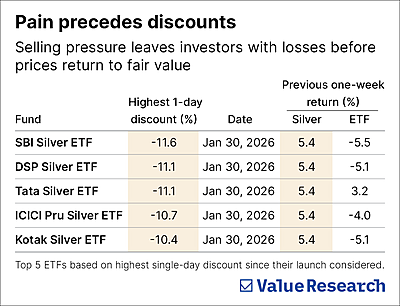

Discounts tell a different story. They often appear after selling pressure, which means investors who entered earlier can be left nursing losses even if silver has not actually fallen.

See table ‘Pain precedes discounts’. The top five silver ETFs by the highest one-day discounts, all simultaneously hit on January 30, 2026, fell up to 11.6 per cent below their NAV this day. At first glance, a bargain. But look at the week prior: investors who bought just before this decline were sitting on losses of up to 5.5 per cent even as silver itself gained 5.4 per cent.

Still, discounts are less dangerous than premiums. If you bought when price and NAV aligned, a subsequent discount is merely driven by temporary market dynamics. Over time, prices converge. The mistake is panicking and selling into the discount, crystallising a temporary dip into permanent loss. Premiums, however, are unforgiving. You pay extra upfront and that excess never comes back.

A reality check

Silver’s long-term numbers look impressive at 12 per cent per annum from January 2006 to January 2026. But strip out the last year and that 19-year return shrinks to 7 per cent. One blockbuster year did the heavy lifting.

That’s how market excitement works. When an asset is flying, it feels eternal. But silver has had quiet phases too. After peaking in April 2011, it plunged 61 per cent over the next four-and-a-half years.

This isn’t a warning to avoid silver but a reality check. Some exposure to precious metals can balance a portfolio. But only in small doses. So treat silver exposure as a portfolio ingredient, not a portfolio plan.

What to remember

ETFs are one of the easiest ways to invest in silver but remember to glance at the price tag before buying. When premiums are steep, wait. When discounts appear, don’t panic and sell. In markets swept by excitement, the best returns often go not to those who rush in first but to those who enter wisely.

This article was originally published on February 20, 2026.

Ask Value Research ![]()