Summary: Silver has broken out of gold’s shadow, driven by supply shortages and accelerating demand from solar, EVs and electronics. With industrial usage rising and volatility offering diversification benefits, silver is emerging as a meaningful satellite allocation for long-term portfolios.

Until recently, silver was seen as a supporting character in the world of precious metals. Investors admired gold for its stability and central-bank backing, while silver was a more volatile cousin best suited for jewellery and small savings. However, 2024 and 2025 have reshaped this perception dramatically. Silver prices have crossed Rs 2 lakh per kilo, rising nearly 2.6 times in the last two years, a surge that coincided with one of the strongest demand-supply imbalances in years.

The dramatic rally has compelled investors to revisit a simple question: Is silver finally stepping out of gold’s shadow and developing an independent long-term story of its own? The answer lies in understanding what has changed beneath the surface.

The supply squeeze

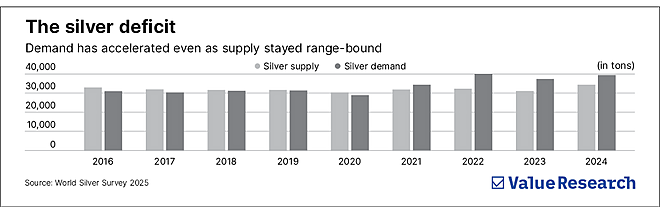

Global silver demand in 2024 stood at 1.16 billion ounces, compared with a supply of barely 1.02 billion ounces. The 149 million ounce deficit marked the fourth straight year of shortfall, pushing the combined deficit across 2021–2024 to over 600 million ounces.

Heavy dependence on by-product mining: Around 58 per cent of the world’s silver production comes unintentionally, extracted while mining other metals such as zinc, copper and gold. If those industries slow, silver supply contracts regardless of price. Silver, therefore, does not enjoy the production responsiveness that metals like copper or iron ore do.

Limited primary silver mines: Only 22 per cent of the global supply comes from dedicated silver mines. Many of these mines are ageing. A notable example is India’s Sindesar Khurd, one of the world’s largest, which contributes roughly 25-30 per cent of domestic output but is expected to wind down by 2029.

Recycling cannot bridge the gap: Recycling contributed around 19 per cent of silver supply in 2024, up from 12 per cent in 2016. But recycled silver often lacks the purity needed for industrial applications.

Mine development is slow: A new silver mine, from discovery to production, typically takes 8-10 years. With demand rising far faster, supply cannot catch up quickly, even if prices remain elevated.

Why silver’s strength may continue

If the supply story explains the recent rally, the demand story explains why the trend may persist.

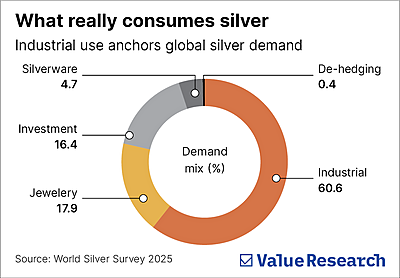

Solar power’s rising hunger for silver: Silver is used inside solar panels because it conducts electricity extremely well. Every solar panel needs a small amount of silver to carry the current generated from sunlight. In 2016, solar panels used only around 4 per cent of the world’s total silver demand. By 2024, this had grown to about 17 per cent, using nearly 5,500 tonnes of silver worldwide. Though manufacturers are trying to reduce the amount of silver used per panel (to save costs), the number of solar panels being installed globally is rising fast.

Electric vehicles and mobility electrification: Each EV uses 25-50 grams of silver, multiple times more than a conventional car. As countries scale EV mandates, silver demand from the transport sector is set to rise steadily.

Electronics, semiconductors and data infrastructure: Silver is key to circuitry, switching components and thermal systems. The growth of consumer electronics, AI computation and cloud data centres adds a durable floor for industrial demand. With global data-centre capacity projected to rise from 60 GW today to 180 GW by 2030, the supporting hardware ecosystem pulls silver along.

How it behaves across market cycles

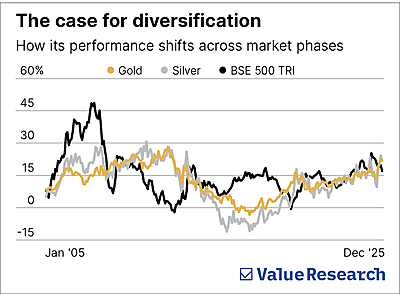

The five-year monthly rolling returns from January 2005 to December 2025 show a clear behavioural pattern. Silver and gold generally move in the same direction. However, silver tends to move more sharply, both on the upside and downside. In contrast, silver and the BSE 500 often move in opposite directions, especially during periods of equity stress. This inverse behaviour is visible across multiple market cycles and indicates that silver can offer meaningful diversification benefits.

The next question is whether an investor should prefer gold or silver. When we compare volatility across the period, gold shows a standard deviation of 7.3 per cent, making it the more stable option. Silver, at 10.6 per cent, is more volatile and closer to equities, which show a standard deviation of 10.2 per cent.

Given silver’s expanding usefulness, spanning solar, electronics, EVs and data infrastructure, its higher volatility is supported by evolving real-world applications. This makes it a viable complement to gold for investors seeking diversification grounded in structural demand.

Should you add silver to your portfolio?

Given its evolving role, silver can serve as a small but meaningful satellite allocation. A 5 per cent exposure works well for most long-term investors. It is large enough to influence returns during up-cycles but small enough to prevent volatility from dominating the portfolio. While silver ETFs are the simplest way to gain exposure, investors must be aware of pricing behaviour. During periods of heightened demand, many silver ETFs in India have traded at significant premiums to their underlying NAV. This happens when investor flows surge faster than new ETF units can be created or physical silver procurement lags demand.

The bottom line

Silver’s recent surge is not an anomaly; it reflects a market recalibrating after years of supply tightness and accelerating demand. With technology adoption rising and correlations offering diversification, silver deserves a fresh look from investors. A measured allocation through silver ETFs, combined with an awareness of premium risks, allows investors to participate in this evolving opportunity without compromising portfolio balance.

This article was originally published on January 01, 2026.

Ask Value Research ![]()