Vinayak Pathak/AI-Generated Image

Vinayak Pathak/AI-Generated Image

Summary: Lower volatility than the Nifty 100. Better returns than the Nifty 100. And 30 per cent sitting in government bonds. India's first hybrid index fund does something that shouldn't work on paper. And 15 years of data says it does.

Hybrid funds have long been active managers’ turf. That is now changing. India’s first hybrid index fund was launched recently and more can follow soon. This first offering tracks the Nifty LargeMidcap250 plus 8-13 year G-Sec 70:30 index, which combines equity with long-term government bonds. Let us start with understanding how it is built and then examine its past performance.

- 70 per cent of the index sits in equity through the Nifty LargeMidcap 250, split equally between the Nifty 100 and the Nifty Midcap 150.

- 30 per cent sits in long-term government bonds via the Nifty 8-13 year G-Sec index that tracks the three most liquid sovereign bonds with maturity of eight to 13 years.

As a hybrid offering, the index pitches a simple promise: offer equity’s growth with debt’s stability. The recipe sounds sensible. But the proof is found in the pudding. So we put it to the test.

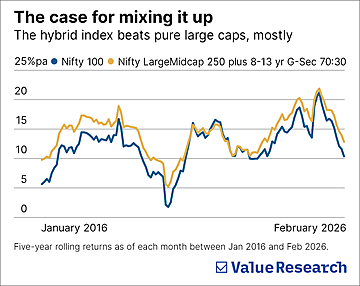

Performance that beats even pure equity

We put a simple question to 15 years of data: if you had invested in the hybrid index, or in the plain-equity Nifty 100, in any month since 2011 and held for five years, which would have given you better returns? In other words, we looked at every possible five-year holding period to test return consistency.

The hybrid index outperformed the Nifty 100 in over 90 per cent of all five-year windows, delivering an average annual return of 14.3 per cent versus 12.2 per cent for the large-cap benchmark. A hybrid index carrying sizable debt, beating a pure-equity index, can feel surprising at first, but the edge comes from the mid-cap exposure.

The hybrid index has a 35 per cent mid-cap allocation via the Nifty LargeMidcap 250, which has delivered average five-year rolling returns of 17.5 per cent over the last decade. Naturally, this pulls the overall return meaningfully higher.

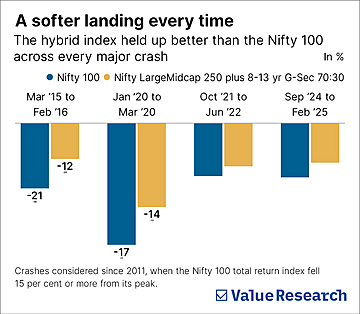

Defying volatility and downturns

The volatility that comes as a result of mixing mid caps is blunted by the debt portion. The mid-cap index’s average standard deviation (a measure of volatility) is a sharp 6.6 per cent against 3.9 per cent for the Nifty 100 over the tested five-year rolling periods. But it is only 1.1 per cent for the long-duration G-Sec index. Its dampening effect, therefore, kept the hybrid index’s overall volatility at 3.3 per cent, lower than the Nifty 100 but with better returns. The hybrid index has also fared better than the Nifty 100 during sharp market corrections, measured across episodes since 2011 when the large-cap index fell more than 15 per cent from its peak. The hybrid index cushioned the fall better in all four market corrections.

In effect, the index has managed to exceed the Nifty 100 over the long term while softening the blows better during market falls.

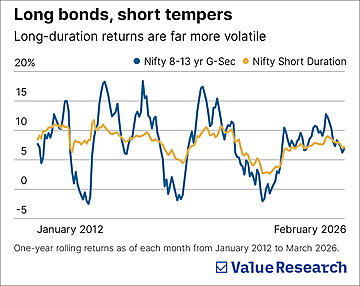

The short-term caveat of the debt slice

Over long periods, the debt allocation has helped steady the index. But over shorter stretches, long-term bonds that make up the debt portion can themselves turn volatile. This is because longer-duration bonds are more sensitive to interest rate changes. When rates rise, long-term bond prices experience steeper declines while short-term bonds remain relatively insulated.

The graph ‘Long bonds, short tempers’ captures this well. It shows how the 8-13 year G-sec index’s journey has been much bumpier over the past 15 years. The Nifty Short Duration index, which tracks shorter maturity bonds of one to three years, was smoother in comparison. The volatility is starkly different, even when both have averaged nearly 8 per cent annual returns over this stretch.

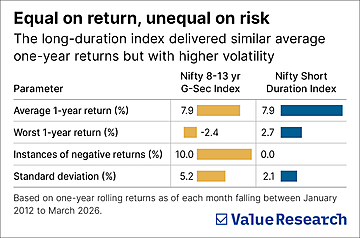

The chances of losses are also comparatively high over short periods. The long-term index gave negative one-year returns nearly 10 per cent of the time, while the shorter counterpart never did. The worst return it gave over a single year was a negative 2 per cent, while the short-duration peer’s worst was still a positive 2.7 per cent. See table ‘Equal on return, unequal on risk’. What this tells you is that in a rising interest rate environment, the debt component may not protect the hybrid index as effectively as it does over a longer period.

Poor returns from the debt portion are possible over a year. At such times, the index’s resilience can be tested, especially if the equity component is lagging too. But this should largely wrinkle out over a horizon of five years or more.

As the 15-year data earlier showed, the index in the long run still sees lower volatility thanks to the debt slice and higher returns due to the mid-cap exposure.

So, who is this index for?

Hybrid investing is for those who like balance. And this index delivers it. The mid-cap exposure lifts returns above what large caps alone would deliver and the government bond allocation blunts the volatility that mid caps introduce. The passive structure keeps costs low and removes the manager’s risk of active hybrid funds. What has to be borne in mind is that over short horizons, long-duration bonds can add to volatility rather than contain it. Therefore, the index will suit those investors better who can stay the course for five years or more.

This article was originally published on April 20, 2026.

Ask Value Research ![]()