Summary: Index investing is no longer just about large caps. With index options across market sizes, geographies and commodities, you can build a fully passive equity portfolio. The right mix depends on how much volatility you can live with while staying invested long term.

Most investors begin their passive investing journey with a simple large-cap index fund. It is familiar, broad and dependable. Yet the index universe has expanded far beyond that.

Today, you can build an entire equity portfolio using index funds alone because there are now options across large caps, mid caps, small caps, global equities and commodities.

With this wide array of options comes a practical question. How can a long-term investor build a fully passive portfolio to match their temperament and their goals? Let’s find out how, depending on your risk profile.

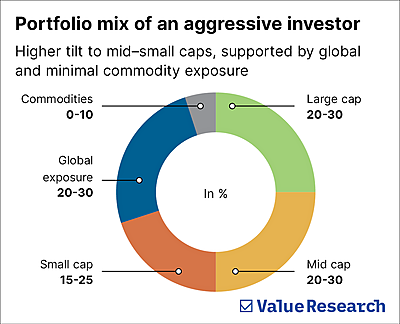

The aggressive investor

If you are someone who can stay calm through sharp market swings and you have time on your side, your portfolio can look like this:

- A large-cap allocation of 20 to 30 per cent, so that the overall structure does not feel unstable.

- The real power can come from mid and small caps. Together, they may form 40 to 50 per cent of your allocation. These segments often move dramatically in both directions, and they can go through deep corrections. However, over long periods, they have historically rewarded patient investors with stronger compounding. That said, because these indices are harder to replicate, comparing the tracking error across funds becomes important.

- Global equities can take up 20 to 30 per cent of your allocation. This introduces you to companies and sectors that the Indian market may not represent fully. It also brings a very important currency advantage. When the rupee loses value over time, your global investments often gain from this shift. When selecting a global scheme, it helps to understand how the fund actually invests. If it directly buys an overseas ETF, you should check whether the ETF trades at a premium or discount to the value of its holdings. If the scheme uses a fund-of-funds structure, be mindful of the double expense ratio. One expense ratio comes from the Indian fund house managing the fund. The other comes from the overseas fund that your money is actually invested in. These combined costs can add up over the years, so checking both is important before you decide.

- You may also keep up to 10 per cent in commodities, such as gold or silver. These assets do not create long-term wealth on their own, but they help protect your portfolio during sudden periods of stress in the equity market.

When all of this comes together, your portfolio uses your long horizon and higher risk appetite to your advantage. You allow the more powerful growth components to compound, you let global exposure and currency movements work for you, and you stay invested even when markets feel uncomfortable. Over time, this approach can turn temporary volatility into long-term opportunity.

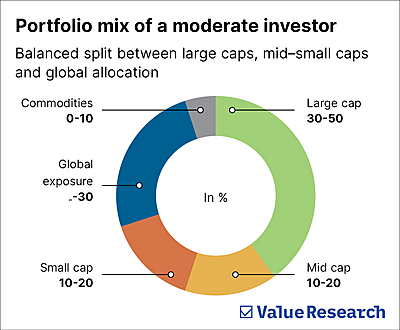

The moderate investor

- Here, a 30 to 50 per cent large-cap allocation becomes the backbone of your portfolio. These companies offer stability and predictable earnings, which help smooth your experience during uncertain periods.

- Mid and small caps can together form 20 to 40 per cent of your allocation.

- Global equities add another 20 to 30 per cent.

- A small commodity allocation of up to 10 per cent remains optional.

The allocation to commodities will not significantly change long-term performance, but it does provide some comfort during stressful market phases. This overall mix lets you participate meaningfully in equity markets while keeping your journey calm, consistent and disciplined.

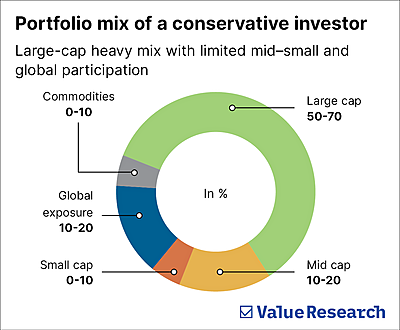

The conservative investor

If your goal is to stay invested in equities but with minimal discomfort from volatility, your portfolio will naturally tilt toward stability.

- A large-cap allocation of 50 to 70 per cent creates a strong, reliable base. This ensures that your portfolio behaves predictably even when markets turn turbulent.

- Mid and small caps can stay between 10 and 30 per cent.

- Global equities can form 10 to 20 per cent of your allocation.

- If you wish, you can include commodities up to 10 per cent, mainly to provide a defensive buffer during market shocks.

This structure keeps your portfolio steady and aligned with your comfort level. You participate in equity markets, but without the intensity that typically comes with more aggressive allocations.

How to choose the right mix?

The decision between these three allocations depends on your obligations and your time horizon. If your goals cannot be compromised, the conservative mix offers the safety and consistency required. If you want long-term growth but prefer a smoother experience, the moderate allocation provides a balanced approach. If you have time, flexibility and no short-term commitments, the aggressive allocation uses your investing horizon to turn volatility into long-term compounding.

Your age can guide this choice even further. Younger investors have more years to recover from temporary declines and therefore benefit from leaning toward the aggressive allocation. As investors approach important milestones, gradually shifting toward moderate or conservative portfolios helps protect accumulated wealth. Once this alignment is achieved, index funds allow your investments to grow with clarity and consistency.

This article was originally published on January 01, 2026.

Ask Value Research ![]()