Devyani International Limited (DIL) and Sapphire Foods India Limited (SFL) are two major players in the Indian QSR (quick service restaurant) market. Both operate Pizza Hut and KFC stores across the country.

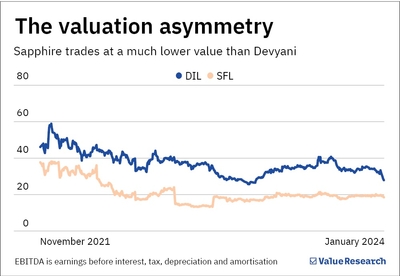

Yet, both companies trade at contrasting valuations, with Devyani being ahead of Sapphire. Let's explore why.

A tale of varying valuations

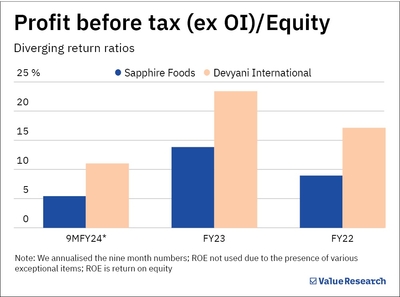

The first thing we checked was how much profit each company generates on its equity. On that front, Devyani International leads Sapphire Foods by quite a significant margin.

Upon taking a closer look at their returns, we observe little difference between Devyani and Sapphire's performance till the EBITDA (earnings before interest, tax, depreciation and amortisation) level.

However, the deviation started after that. Compared to Devyani, Sapphire boasts a larger equity base, the excess of which primarily lies in cash and fixed assets (particularly plant and machinery and leasehold improvements).

Further, while Sapphire has a lower store count than Devyani's, the former's quantum of store-related assets is similar to the latter's. As a result, Sapphire's high fixed assets have led to increased depreciation costs, affecting its return ratios.

A comparison of Devyani and Sapphire's financials (9M FY24)

Sapphire's legacy problems are hurting its profitability

| Metric | SFL | DIL |

|---|---|---|

| Total store count | 850 | 1452 |

| Revenue (Rs cr) | 1963 | 2509 |

| EBITDA margin (%) | 18.3 | 18.9 |

| Depreciation (Rs cr) | 237 | 259 |

| Interest cost (Rs cr) | 73 | 130 |

| Profit before tax (Rs cr) (1) | 54 | 85 |

| Shareholders' equity (Rs cr) (2) | 1313 | 1023 |

| (1) / (2) (%) | 5.4 | 11.1 |

| Cash and cash equivalents (Rs cr) | 216 | 30 |

| Property, plant and equipment (Rs cr) | 871 | 1028 |

| Note: P&L data as of December 2023; Balance sheet data as of September 2023 | ||

Why does the anomaly exist?

To understand why Sapphire's fixed assets are comparable to that of Devyani despite having fewer stores, we need to go back in time.

Before Sapphire Foods came into existence, Yum! Brands (the owner of Pizza Hut and KFC) operated its stores by franchising to various small operators and one relatively large operator (Devyani International). However, the small operators were not as efficient and became unviable. Hence, Yum! Brands clubbed all the small operators and got in touch with a consortium of private equity players who then set up Sapphire Foods in 2015.

That is the first important bit for understanding the anomaly. Here is the second one.

At the start of FY24, Sapphire's management commented that most of the extra capex was due to refurbishments of its legacy stores (those run by small operators earlier). The management expects the capex thrust to peak out in one or two years.

So, we decided to adjust Sapphire's equity and depreciation based on Devyani's numbers to find whether that was the case and what the former's return ratio would look like.

Adjusted numbers

The picture looks very different now

| Metric (in Rs cr) | Sapphire | Devyani |

|---|---|---|

| EBITDA | 358 | 474 |

| Adj. depreciation | 152 | 259 |

| Interest cost | 73 | 130 |

| Adj. profit before tax (1) | 133 | 85 |

| Adj. property, plant and equipment | 616 | 1028 |

| Adj. shareholders' equity (2) | 872 | 1023 |

| (1) / (2) (%) | 20.4 | 11.1 |

| Note: Shareholders' equity was adjusted for extra cash and fixed assets | ||

Remember that the above numbers are merely hypothetical calculations, as other factors must be considered. For instance, Devyani is more aggressive in its store expansion and diversification of its brand portfolio (Costa Coffee, Vango, and The Food Street). All these are in their initial stages and will take time to scale up.

But one thing is clear: once Sapphire's capex starts to peak out, its profitability may rise, and thus, there is a likelihood for its valuation gap to narrow down.

Our take

While the current valuation asymmetry can be attributed to Sapphire's low profitability ratios, there's a chance of this coming into symmetry in the future.

Does this imply that investing in Sapphire would be a good idea? Well, no one knows how much the valuation gap may narrow. Devyani may likely experience a contraction in its value with no improvement in Sapphire's financials.

Moreover, Indian QSR companies have been facing headwinds lately (high inflation and stiff competition from local players). Yet, they continue to trade at excessive valuations.

Hence, waiting and seeing how Sapphire's performance pans out in the coming years might be prudent before pressing the buy button.

Also read: Takeaway from this burger joint's comeback story

Ask Value Research ![]()