While most of us know that purchasing motor insurance is mandatory by law; many of us do not know a lot of other relevant information. So, before we dive into one of these key terms - IDV, let's set some context for you.

When buying a motor insurance, we can buy either a third party insurance or comprehensive insurance. The key difference between the two is that while third-party insurance covers only the damage caused to the other party; the comprehensive motor-insurance also covers your losses.

In effect, every policy varies in its structure and compensation. However, this does not mean that your car insurance may necessarily pay out the total value of your car in case of loss or theft of your vehicle. Do you know why?

Well, that's what IDV or 'Insured Declared Value' is about!

What is IDV?

IDV refers to the maximum amount an insurance company agrees to pay out in case of theft or total loss of the insured vehicle. They calculate it when you buy the insurance.

It is similar to what you call 'sum insured' in the case of health insurance.

Why is it important for me to know about IDV?

The higher the IDV, the higher the premium, and vice versa.

Since different insurers assess it differently, you can choose the one that works the best for you. Ethical insurers always evaluate your car so that its IDV is closest to its actual value.

Does this mean that my claim might be rejected on the basis of IDV, specially when I buy a used vehicle?

No. Ideally, the insurance company had already agreed to pay you money equivalent to your IDV when you purchased the insurance. Also, when the insurance company calculates the IDV, it factors in the condition of the insured vehicle.

There's a catch here. Sometimes, the highest IDV may not be justified because it may be more than the actual value of your car. So you should always choose an insurance company that offers you an IDV close to your vehicle's actual value.

How is IDV calculated?

It is calculated on the basis of the manufacturer's listed selling price of the vehicle. It is then adjusted based on the depreciation of the vehicle's age, wear and tear and market conditions.

For instance, if you buy a car for Rs 10 lakh, depending on the insurer, your sum insured or IDV could be Rs 9 lakh in case of an incident that occurs in 6-12 months.

Does the IDV of my car remain constant, or does it change?

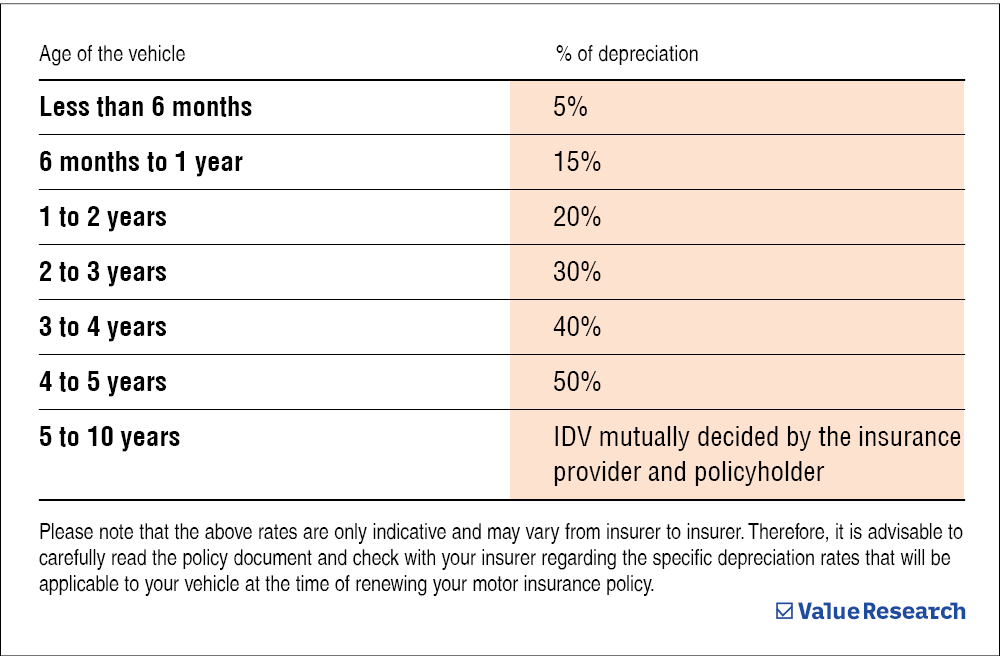

Your vehicle's value starts depreciating right when it leaves the showroom, as shown in the table here.

Since the market conditions keep changing, the IDV also keeps reducing every year.

For instance, each year, a car's value depreciates by a certain percentage, and the depreciation can go up to 40 per cent for a car aged five years. The IDV will be revised annually based on the vehicle's age, condition, and other relevant factors.

Key points for you:

- Speak to more than one insurer. Compare the IDV.

- Opt for a higher IDV. It will give you more cover, but it also comes at a higher premium.

- Choose the IDV that's closer to the actual value of your car.

This article was originally published on April 18, 2023.

Ask Value Research ![]()