FD interest rates have been increasing consistently and you can't easily ignore the luring rates being offered by the small banks.

But the confusion still remains - in which instrument should you park the debt portion of the portfolio?

What's the scenario?

The FD returns have picked up pace, yet they are not completely indicative of the revision and there is still room for northward movement in FD interest rates.

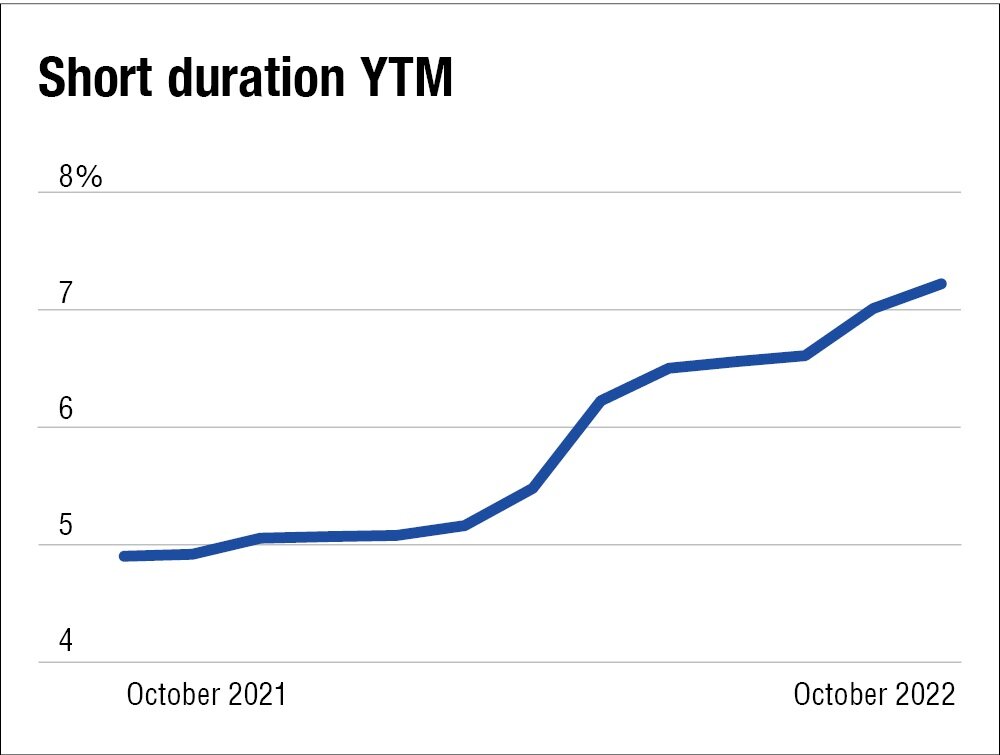

Debt funds' YTMs (yield to maturity) have also started moving upward and are higher compared to last year's YTM. YTM is the amount expected to be generated if you hold the instrument till maturity date.

Hence, we recommend not to park your funds for very long in FDs. If required, keep it under one year and redeploy those funds based on the market condition.

An advantage of debt funds over fixed deposits is simply the tax efficiency that they provide. Debt funds investments beyond three years give you indexation benefits and (long-term capital gains) are taxed at 20 per cent. Fixed deposits don't have that feature.

Do not forget

Define the objective for which you need the specific funds. You need to park your money in a different instrument if you want to build an emergency corpus versus if you want protection against market volatility. So, tie the benefits of the instrument with your objective and then allocate your funds.

In conclusion

- For emergency corpus, you may choose to resort to liquid funds.

- For debt allocation, you can consider short duration funds.

- If your horizon is wide and you want to take tax benefits, leverage products such as Public Provident Fund (PPF) and National Savings Certificate (NSC).

This article was originally published on December 02, 2022.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()