What is Public Provident Fund?

The Public Provident Fund (PPF) is a long-term savings instrument established by the central government. It offers tax benefits on contributions as well as withdrawals after the lock-in period. This scheme came into force on July 1, 1968, and is backed by the government with the objective to provide old- age income security to the self-employed and those working in the unorganised sector. Though the scheme is voluntary, assured returns and income-tax benefits have fuelled its popularity.

Features of PPF

- Eligibility: You need to be a resident Indian.

- Entry age: No age is specified for account opening.

- Investments: Minimum: Rs 500 per annum. Maximum: Rs 1.5 lakh per annum. Investment can be made in lump sum or instalments in multiple of Rs 50. No limit on the number of instalments in a financial year (earlier it used to be 12).

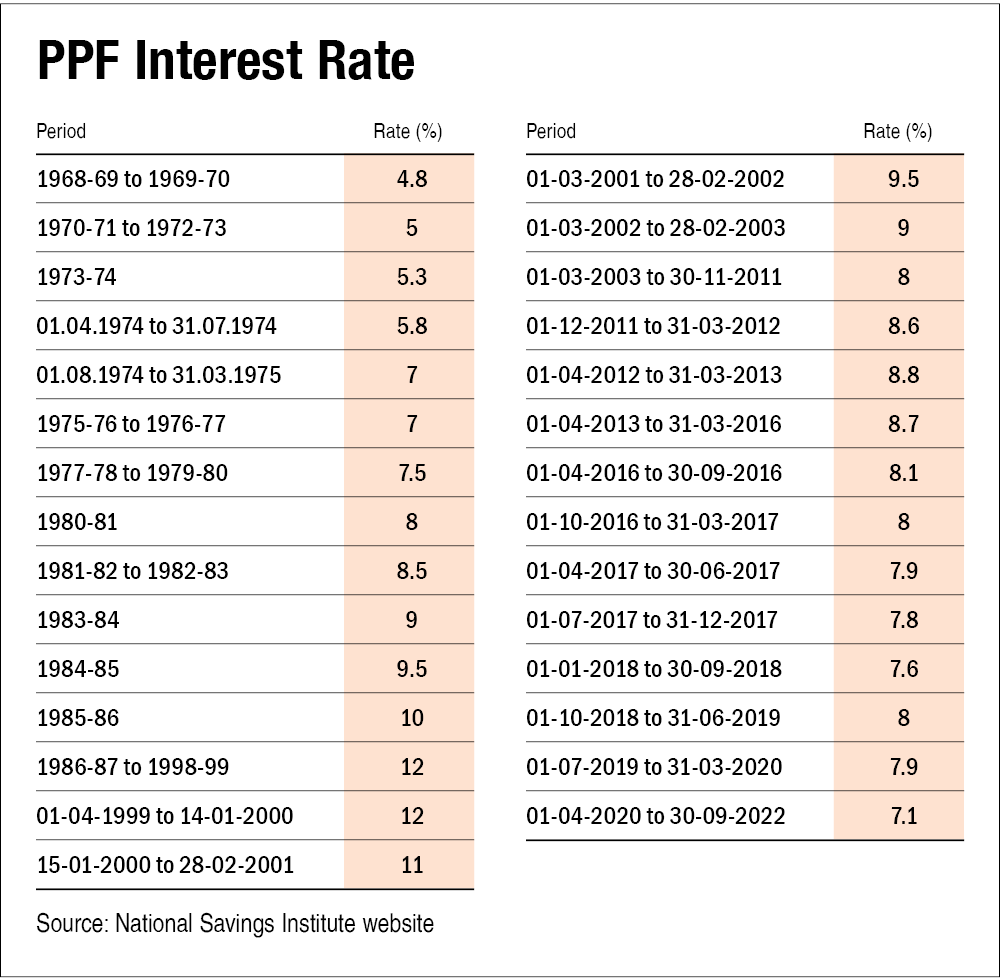

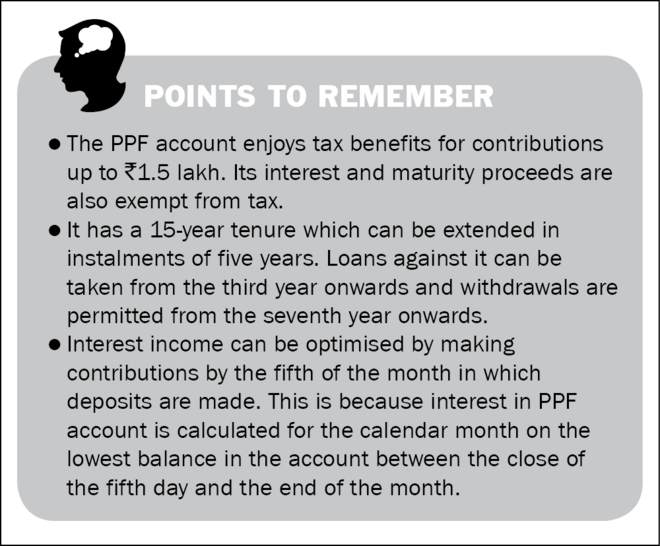

- Interest: 7.10 per cent compounded annually. The interest shall be calculated for the calendar month on the lowest balance in the account between the close of the fifth day and the end of the month.

- Tenure: 15 years. On completion of 15 years, the account can be extended with or without deposit in a block of five years at a time. There is no limit on the number of extensions. However, once the PPF account is continued without deposits for more than a year post maturity, then the account holder cannot make deposits in the subsequent years. The PPF account matures after 15 years but the contribution has to be made for 16 years in all. This is because the 15-year period is calculated from the end of the financial year in which the account is opened. Effectively, the PPF account matures on the first day of the 17th year. However, it can be extended indefinitely for five years at a time.

- Account-holding categories: Individual and minor (through the guardian).

- Nomination: Facility is available.

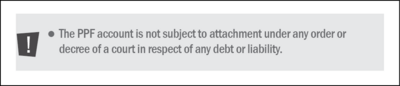

- Exit option: Premature closure of a PPF account is not permissible except in the case of the death of the account holder or after completion of five years from the end of the financial year in which the account is opened if the money is required for the treatment of a critical illness or to fund higher education.

Investment objective and risks

The primary objective of saving in the PPF account is to avail tax deductions on deposits, guaranteed returns on investment and tax-free withdrawal on the maturity. Savings in this product are completely risk-free because of the government backing.

Suitability and alternatives

- Suitable for risk-averse investors seeking assured returns by investing regularly for long-term goals, which are 15 or more years away.

- Not suitable for investors who can assume some risk by investing in equity-linked investments, which can generate much higher returns in a 15 year period.

- Alternatives can be NPS (for retirement savings) and Tax saver equity mutual funds (ELSS)/ Direct stock investing (for those who can assume risk).

Capital protection and inflation protection

The capital in a PPF account is completely protected, as the scheme is backed by the Government of India, making it fully risk-free with guaranteed returns. The PPF account is not inflation protected, which means whenever inflation is above the latest guaranteed interest rate, the deposit earns no real returns. However, when the inflation rate is below the guaranteed rate, it does manage a positive real rate of return.

Guarantees

Interest rates are aligned with G-sec rates of the similar maturity, with a spread of 0.25 per cent. The government has decided to review the PPF rates quarterly. For the fourth quarter of FY21-22, the rate has been set as 7.10 per cent compounded annually.

Liquidity

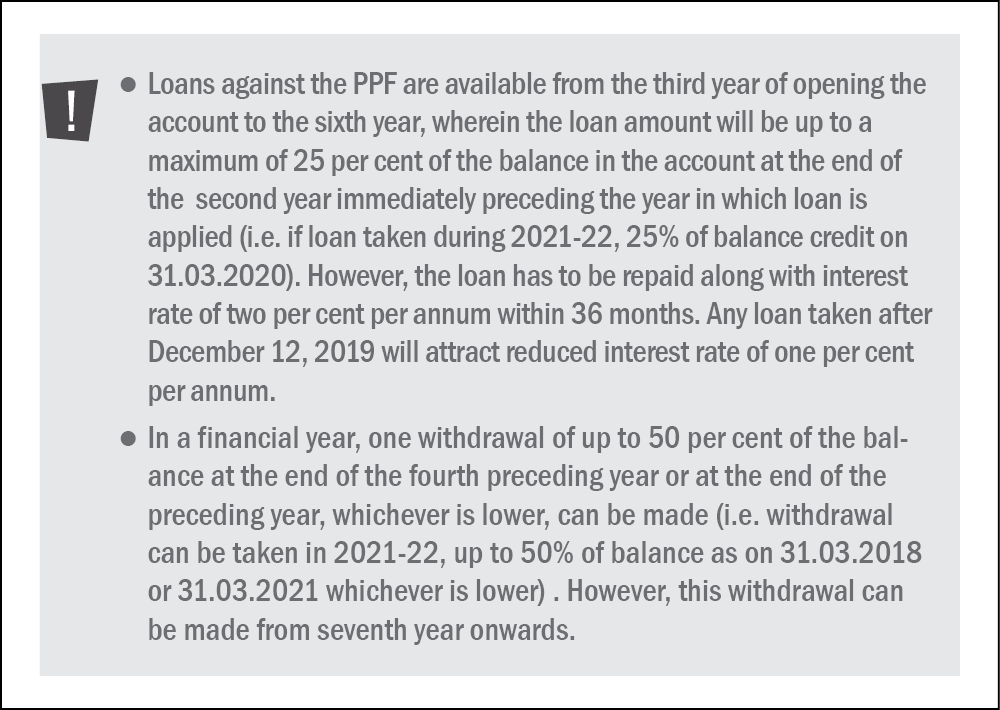

The PPF is liquid, despite the 15-year lock-in stipulated with this account. Liquidity is offered in the form of loans against the PPF from the third year and withdrawals are subject to conditions from the seventh year.

Also, it is now possible to close your PPF account pre-maturely at a penalty of 1 per cent on the interest. However, it can be done only after five years from the end of the financial year in which the account is opened, provided the money is required for the treatment of serious ailments of the account holder, spouse or dependent children, for the higher education of the account holder or dependent children or change in residency status to NRI.

Tax implications

The scheme has the exempt-exempt-exempt (EEE) status, where the deposits, the interest earned as well as the maturity amount are tax-free.

The sum invested in the PPF account is eligible for tax deduction under Section 80C, subject to a maximum of Rs 1.5 lakh in a financial year. On maturity, the entire amount, including the interest, is tax-free.

Where to open an account

You can open the account at various places such as:

- Any head post office or general post office.

- Branches of nationalised banks: State Bank of India, Bank of Maharashtra, etc.

- Private-sector banks: ICICI Bank, Axis Bank, etc.

How to open Public Provident Fund

Once you have selected the location to open an account, you will need the following documents:

- An account-opening form.

- Two passport size photographs.

- Aadhaar card. In the absence of the same, you need to provide a copy of the acknowledgement of your Aadhaar application.

- Address and identity proof, such as the Aadhaar card, passport, PAN (permanent account number) card or declaration in Form 60 or 61 as per the Income-Tax Act, 1961, driving licence, voter's identity card or ration card.

- Carry the original identity proof for verification at the time of account opening.

- Choose a nominee.

How to operate a PPF deposit

- You need a pay-in slip with the initial account-opening sum to be credited to your account.

- You get a PPF passbook with your photo affixed, stating the nominee's name.

- You can also manage your PPF account online via net banking.

To view the current rates on the schemes, go to vro.in/s34211

This article was originally published on December 24, 2021, and last updated on July 07, 2022.

Ask Value Research ![]()