It's raining additional tier-1 (AT1) bonds. But the mutual fund industry, still stinging from the Yes Bank fiasco and regulatory restrictions, has taken a raincheck.

Some of the banking heavyweights - including HDFC Bank, State Bank of India, Bank of Baroda, Union Bank, among others - have serially rolled out AT1 bonds at 7.75 to 8.85 per cent to raise around Rs 18,300 crore in recent weeks.

While the rate of returns is on the higher side as compared to other such products, mutual funds remain coy after what happened with Yes Bank.

Yes Bank 'ghosting' haunts mutual funds

In March 2020, when the then fifth-largest lender was effectively taken over by the state due to its ballooning loan book (of almost Rs 3 lakh crore) and growing bad loans, investors across 30 mutual fund schemes lost to the tune of Rs 2,800 crore.

The mutual fund industry is yet to erase that painful memory. "After the Yes Bank fiasco, we don't want to take unnecessary risks to earn extra returns," said a fixed-income head of a mid-sized fund on anonymity.

Why mutual fund industry lost Yes Bank money

Before that, let us explain how AT1 bonds work. Banks issue these bonds to raise money and ensure they have adequate capital, as stipulated by Basel III norms.

AT1 bonds have no maturity date and offer higher returns as compared to other issues.

However, they are often deemed riskier than other bonds because banks can skip paying interest if they are running on losses at that moment or fail to maintain a certain equity tier ratio - something that happened when Yes Bank went near-bust.

SEBI restrictions

Given the risk associated, market regulator Securities and Exchange Board of India (SEBI) imposed curbs on investments made by mutual funds in AT1 bonds in March 2021.

According to the guidelines, no scheme can invest more than 10 per cent in such bonds and not more than 5 per cent in the bonds of a single issuer.

Further, no AMC, under all its schemes, can invest more than 10 per cent in such bonds issued by a single issuer.

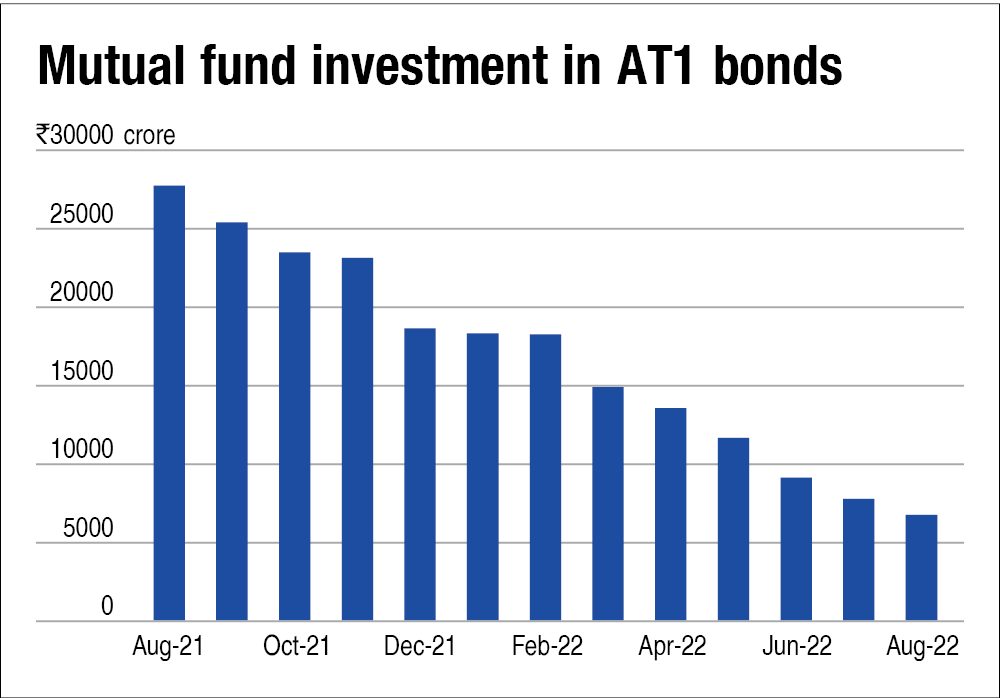

As a result, mutual fund holdings in AT1 bonds have reduced significantly in the last 12 months. As of August 2022, total investments made by mutual funds schemes in AT1 bonds stood at Rs 6,718.31 crore - down from Rs 27,788.73 crore a year earlier.

Insurance companies show interest

AT1 bonds aren't exactly lovelorn.

While mutual funds are swiping left, insurance companies, along with high net-worth individuals, have started making a beeline for these products as they offer better yields.

Ajay Manglunia, Managing Director & Head of Institutional Fixed Income at JM Financial, said, "In recent issues of AT1 bonds, we have seen they are giving better yields compared to other debt papers like corporate bonds. Prior to 2020, banks with poor balance sheets used to come out with the AT1 bonds, but now we are witnessing a trend wherein strong banks with solid balance sheets are tapping the markets through perpetual bonds. One of the major reasons why banks are coming out with AT1 bonds is because there has been a pick-up in credit demand."

What is in it for you?

Prior to March 2020, many retail investors (read: fixed deposit investors) were advised to invest in AT1 bonds of Yes Bank, which proved disastrous.

SEBI also imposed a penalty of Rs 2 crore on Rana Kapoor, former Chief Executive Officer (CEO) of Yes Bank, for mis-selling AT1 bonds to retail investors.

Therefore, you are advised to exercise caution.

Ask Value Research ![]()