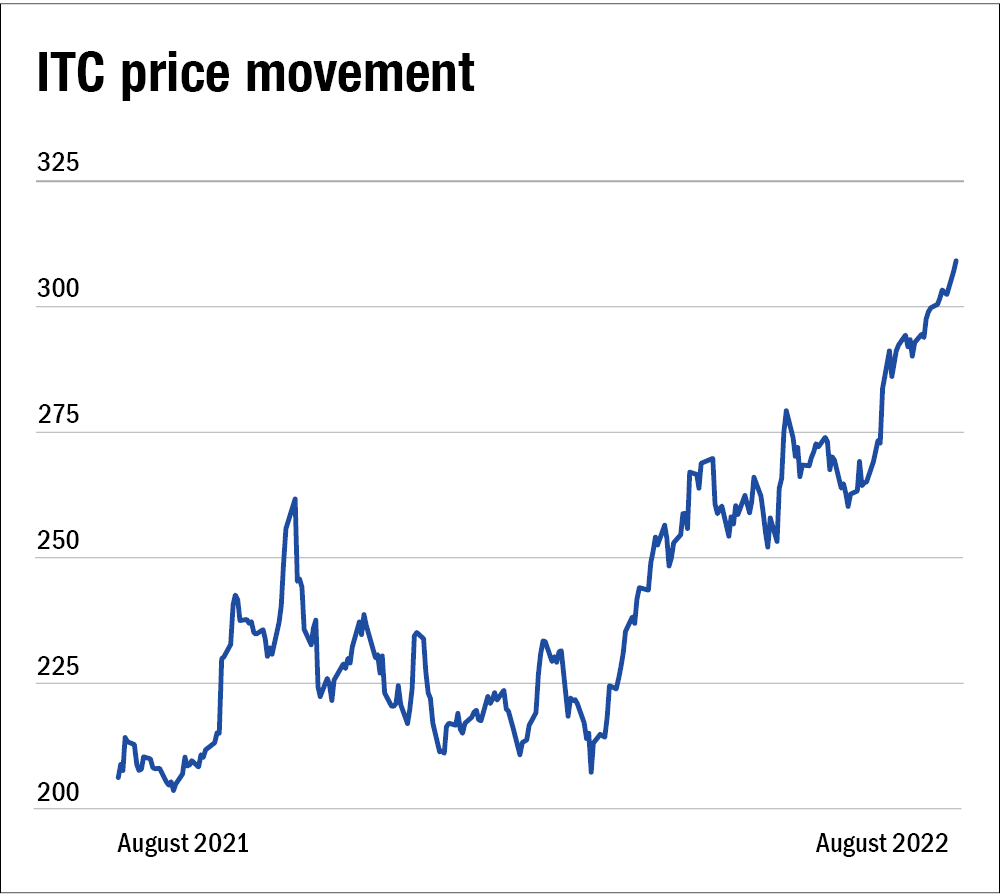

If you had told someone a year ago that ITC will go up 49 per cent in the next 12 months and increase its revenue and profits by more than 15 per cent in FY22, they would have laughed at you. And now, when the market is falling, ITC investors are a happy lot.

What resulted in such a performance? Strong growth in all of its business segments

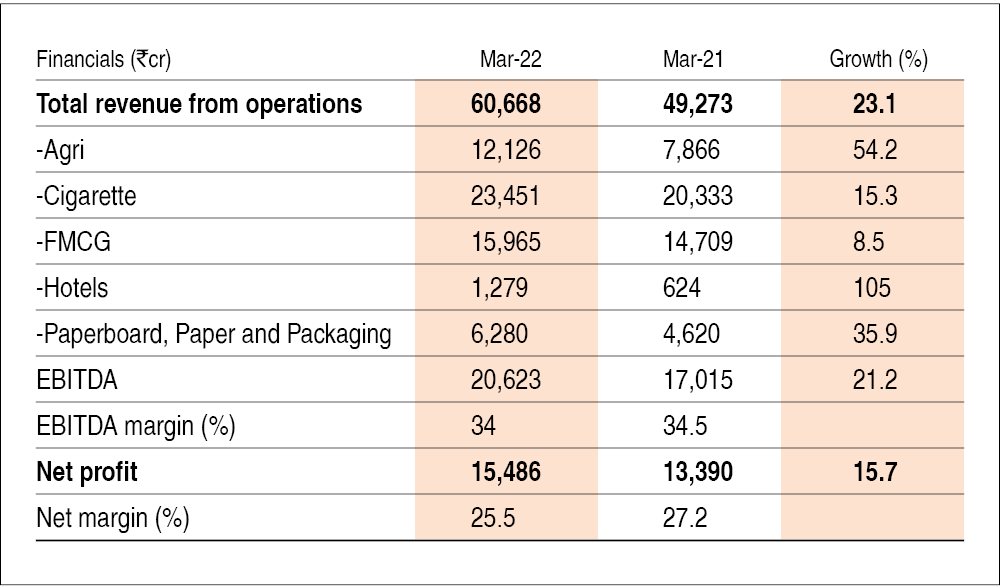

ITC witnessed strong growth in its cigarettes segment after facing a hiccup in FY21 and has posted a minimum of 10 per cent YoY (year-over-year) growth in the last five quarters. ITC also posted its best ever yearly revenue from this segment at Rs 23,451 crore (on a standalone basis) since FY17 when it posted a revenue of Rs 34,002 crore. This combined with the tobacco tax being untouched in this year's budget was a major boost.

Its hotel business, which saw a massive 66 per cent fall in revenue due to COVID in FY21 recovered well. In its recent quarterly results, ITC had stated that occupancy levels and average room rates have also reached pre-pandemic levels. This resulted in a segment EBIT (earnings before interest and taxes) of Rs 112 crore, a strong recovery from a loss of Rs 151 crore in the previous year.

Its paper boards, paper, and packaging segment not only posted the highest ever revenue but also highest ever yearly growth in FY22 at 36 per cent! The government's ban on single-use plastic is also expected to augur well for the company as it has already been developing alternatives for single-use plastics in its specialty papers division. ITC has also planned to spend around Rs 2,500 to 3,000 crore for Capex in this segment.

The same is the case for its agri segment too. It posted the highest ever revenue at Rs 12,126 crore and highest ever growth at 54 per cent! Around Rs 3,000 to 4,000 crore is expected to be spent on this segment to push digital growth.

Its FMCG business, where it has various flagship brands, flourished in the last couple of years posting the highest ever segment revenue and profit in FY22. While many companies were struggling to grow their topline, ITC almost doubled its profits in this segment in FY21 due to a surge in demand for convenience food and multi-channel distribution system, especially modern trade channels.

All these factors, coupled with a strong dividend payout, have made ITC once again attractive to investors. Even at a price of Rs 310, it has an attractive dividend yield of 3.7 per cent. Year to date the stock has given 42 per cent returns, its best performance in several years and a huge recovery from its mere 2 per cent returns in 2021. With strong momentum in almost all of its segments, the strong growth is expected to continue going forward too.

Also read:

Five pointers to find a moat

A simple measure to judge capital allocation

Ask Value Research ![]()