In our previous article, we looked at the management tenets that Buffett follows. Let us continue with the third and most important part of Buffett's beliefs - the financial tenets. These are critical measures that Buffett expects all the companies to maintain to be considered investment worthy. Here, we would like to point out that Warren Buffett doesn't look at the results of a company on a quarterly basis or even on a yearly basis. He looks at revenue and profit growth in five-year periods as it displays a better picture. We once again would like to remind you that these tenets are from the book 'The Warren Buffett Way' by Robert G Hagstrom, and if you would like to know in-depth, you can read the book (which is just awesome). Now let's not delay any further and look at the tenets.

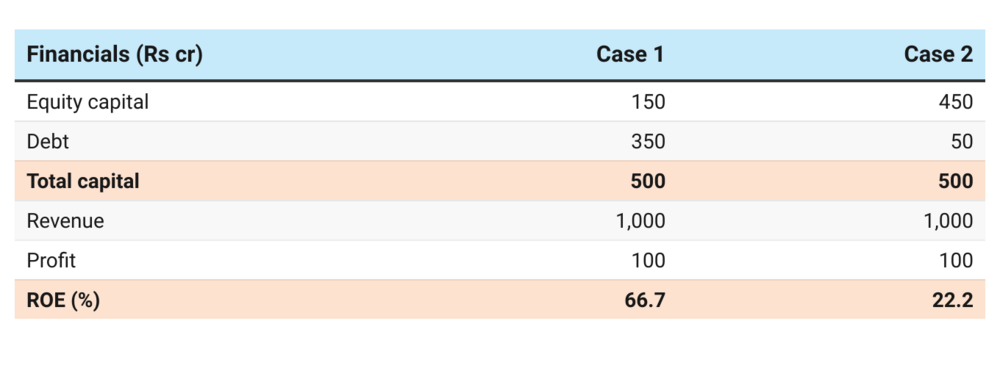

- Focus on return on equity (ROE), not EPS. The profits that are earned every year are retained by the company, at least a part of it after paying dividends. These retained earnings are then added back to the total equity which will then be reinvested in the company. So, it is obvious that the EPS will increase. But what matters is whether the company is able to give above-average returns on the equity invested. Buffett also emphasises that this high ROE must be attained without the help of high debt since it can inflate the ROE. You can see in the table below how high debt can affect ROE.

- Owners' earnings reflect true value. Buffett is not a big fan of accounting profits or even cash flows since cash flows don't account for capital expenditures. Instead, he uses owners' earnings which are calculated as 'Net income + (depreciation, depletion, amortisation) - capex - any additional working capital expenditures needed.' Now you may wonder, "Isn't this just free cash flow?". Yes, it is free cash flow. We must remember that Warren Buffett came up with this concept almost 37 years ago when cash flow statements weren't mandatory. You can also calculate it as cash flow from operations - capex incurred. You can find capex in cash flow from investing activities section - purchase of property, plant, and equipment. Owners' earnings exclude non-cash expenditures incurred (depreciation) and include total capex incurred which would only be depreciated over the years.

- Profit margins. This one is pretty simple. Great businesses are bad investments if they don't convert revenues into earnings. What is the use of such high revenue when only a small portion of it is converted to earnings? Warren Buffett believes that cost controlling should be a daily ongoing process where the managers should consistently look for any inefficiencies. Now, this doesn't mean you should reject companies just because they have low margins. Why? Avenue Supermarts (DMart) is an example. It has grown its profits at 28 per cent per annum in the last five years with a median net margin of just 4.7 per cent. How so? Instead of relying on margins, they rely on volumes (similar to Walmart). The company has a median asset turnover of 2.9 times!

- One dollar premise. Retained earnings are the money reinvested in the company out of previous years' profits after paying dividends. Warren Buffett says that if a company employs that retained earnings poorly over the years, the market price will reflect that and vice versa. So he states, that an increase in the market value of a company should match at least the amount of retained earnings. But since yearly data is fluctuating, Buffett takes it for a decade to arrive at a conclusion. The formula is 'Change in market cap divided by retained earnings for the period.' For example, Asian Paints has generated a total retained earnings of Rs 11, 473 crore from FY12 to FY22. The company's market cap has increased by Rs 4,68,447 crore during the same period. That means Asian Paints has increased its market value by Rs 41 for every single rupee reinvested. For details, read Buffett's $1 test.

In this series:

Also read:

How many stocks should you own?

Five pointers to find a moat

Excerpts from Howard Marks' recent memo

This article was originally published on August 02, 2022.

Ask Value Research ![]()