Dhruv, a 32-year-old legal professional, takes home about Rs 80,000 a month. For saving taxes, he plans to utilise the maximum permissible deduction of Rs 1.5 lakh under Section 80C of the Income Tax Act. Dhruv wants to earmark this investment for his retirement. However, he is confused between tax-saving mutual funds, also called equity-linked savings schemes or ELSS, and the National Pension System (NPS) Tier I. He seeks our advice on the appropriate investment option for him.

What is the NPS Tier-I?

- The NPS is a government-backed defined contribution pension scheme, started almost two decades ago. The minimum annual contribution is Rs 1,000 and anyone can invest in it. The money gets invested in a mix of equity and fixed income through a pension fund manager of your choice.

- On attaining the age of 60, you can withdraw 60 per cent of the accumulated corpus as a tax-free lump sum. It is mandatory for every investor to buy an annuity plan with the remaining 40 per cent if the total corpus exceeds Rs 5 lakh.

- Partial withdrawals (25 per cent of your contribution) are allowed only in certain specified situations, including for the higher education or wedding of children, house purchase, a business venture, the treatment of a critical illness and a few others. However, it can be done only after three years of opening the account.

- Pre-mature closure of the NPS account is allowed only after 10 years. In such a scenario, it is mandatory to buy an annuity plan with at least 80 per cent of the corpus if the total value of the corpus exceeds Rs 5 lakh.

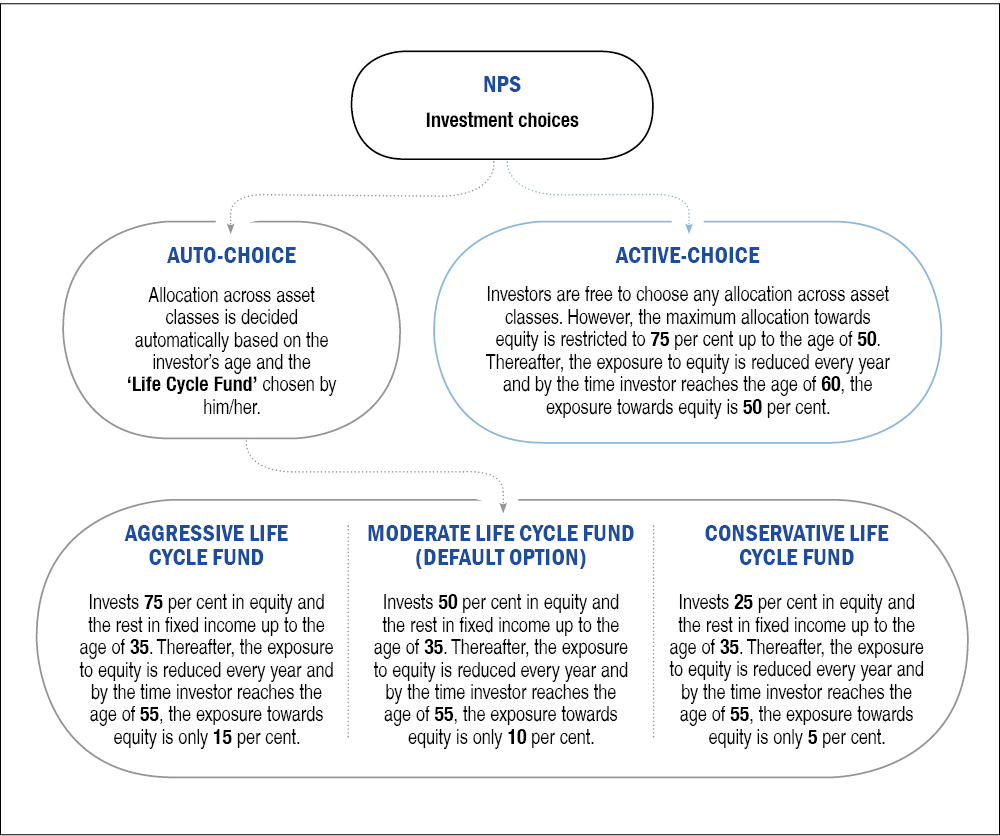

Where does the NPS invest your money?

- The NPS invests your money in a mixture of equities, government bonds, corporate bonds and alternative investments. The proportion can be decided by the investor.

- At present, two investment choices are available: Auto and Active. 'Auto' further has three variants: Conservative, Moderate and Aggressive.

- See the flowchart to understand the various options available in the NPS.

Tax benefits

- Section 80C of the Income Tax Act allows investments up to Rs 1.5 lakh in a financial year, in several products to lower the tax outgo, with investment in the NPS Tier I being one of them.

- One can claim an additional deduction of up to Rs 50,000 for investments made specifically in the NPS Tier I under Section 80CCD (1B).

- Contribution made by your employer to your NPS account are also exempt up to 10 per cent of your basic pay and dearness allowance. If you are a government employee, it is exempt up to 14 per cent.

How is the NPS different from ELSS?

- Liquidity: Unlike the NPS, tax-saving mutual funds or ELSS have a lock-in period of just three years. Investors are free to redeem their money after that without any restriction. However, it is advisable to link your ELSS investments to a long-term goal and continue with them accordingly.

- Maximum allocation to equity: Tax-saving mutual funds are pure equity funds and invest fully in equity. On the other hand, in the NPS, your allocation to equity cannot be more than 75 per cent. It further tapers down after the age of 50.

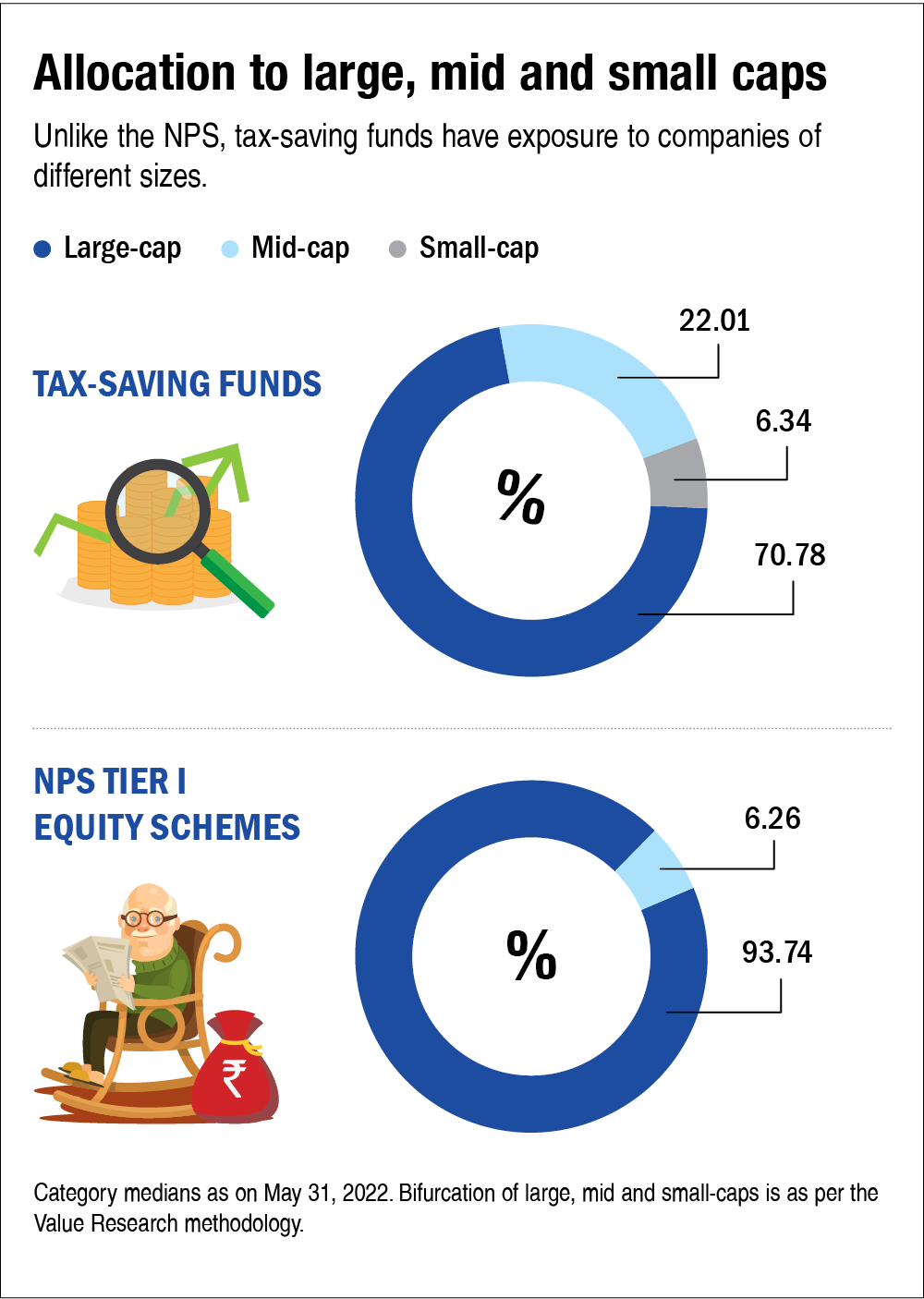

- Portfolio structure: Tax-saving mutual funds are quite similar to flexi-cap funds in terms of their exposure across companies of different sizes. Although the fund manager is free to allocate between large, mid and small caps in any proportion, tax-saving funds generally maintain about 70 per cent in large caps and the rest in mid and small caps to boost your returns over a long period of time. This can be beneficial if you have a long horizon, as in the case of Dhruv. On the other hand, equity plans of the NPS are predominantly invested in large caps (see chart 'Allocation to large, mid and small caps').

Performance comparison

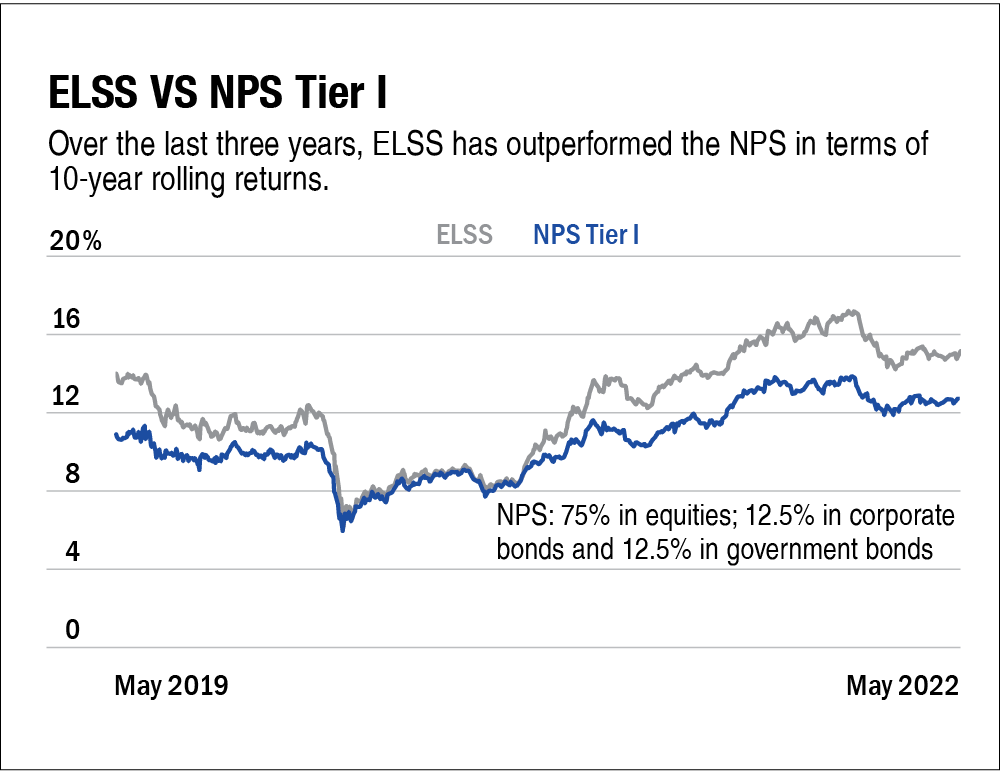

- Given that tax-saving funds have higher exposure to equities, they are likely to return more over a long period of time as compared to the NPS. The same is visible in the graph titled 'ELSS vs NPS Tier I', where we have compared 10-year rolling returns of ELSS with those of the NPS Tier I had someone invested 75 per cent in equities and 12.5 per cent in each government and corporate bonds.

- Over the last three years, the average 10-year return generated by ELSS has been 12.15 per cent as against 10.42 per cent by the NPS. That's about 14 per cent less as compared to ELSS.

Which one should you choose?

- In the case of Dhruv, the choice between the NPS and ELSS depends on how disciplined he is with his investments. The NPS virtually locks your money till the age of 60 and restricts the investment in equity to a maximum of 75 per cent. Further, it follows a conservative approach and doesn't allocate much to mid and small caps. Given these aspects, tax-saving mutual funds are a better proposition for Dhruv. Since he has a long investment horizon, higher exposure to equity with some allocation to mid and small caps will be beneficial. It will help him accumulate a higher corpus.

- However, if Dhruv lacks investment discipline and tends to use his retirement savings intermittently for other purposes (as and when some need arises), he should invest in the NPS. Since the investment in the NPS gets virtually locked till the age of 60, it works as an advantage for someone who lacks discipline as it keeps the retirement money safe.

- While investing in the NPS, Dhruv should choose the 'Active' choice and allocate the maximum possible to equity.

- He should also consider investing in the NPS for claiming the additional tax benefit of up to Rs 50,000 under Section 80CCD (1B) after exhausting the Rs 1.5 lakh limit of Section 80C. Money saved is money earned.

Don't ignore these

- Maintain a contingency fund which is readily available during the emergency. This should be equivalent to at least six months of your expenses.

- Buy a pure term plan with adequate life cover if you have financial dependents.

- Health insurance is a must for all family members.

This article was originally published on July 20, 2022.

Ask Value Research ![]()