At a time when debt funds are struggling to generate any real (inflation-adjusted) returns for investors, how about a debt fund that gives 150 per cent returns a year? If you think we're kidding, we aren't. Click here to see it for yourself.

Given such outsized returns, BOI AXA Credit Risk Fund shines at the top across the entire debt-fund spectrum. However, there's a catch here. These returns are based on writebacks and sales of Amanta Healthcare and Sintex bonds, respectively, which were earlier marked down.

Putting things in perspective...

From 2018 to 2020, this fund has witnessed significant downgrades in its bond holdings of issuers like Kwality, IL&FS, DHFL, Sintex, Avantha Holdings, Café Coffee Day, Accelarating Education and Development Pvt. Ltd, RKV Enterprise Pvt Ltd, Amanta Healthcare, and Dinram Holdings.

In the interim, the fund's AUM nosedived as disappointed investors exited the fund after significant write-offs. Thus, these current recoveries on a small asset size have made this fund look like the best performing one in the last one-year period.

So, while a wider set of investors bore the losses on account of downgrades, the spoils of the recoveries have gone to the handful who've continued to stay with the fund.

This is precisely the anomaly that SEBI's segregation (or side-pocketing) rules aim to plug to make mutual funds a fairer investment vehicle for all investors.

Had these bonds been segregated, even the investors who had exited would have got their fair share.

While SEBI had already introduced side-pocketing norms at the time of write-offs, the fund inserted them in its Scheme Information Document (SID) only in May 2020.

So what you ended up with is a windfall in the hands of a select few instead of being distributed more equitably among its rightful claimants.

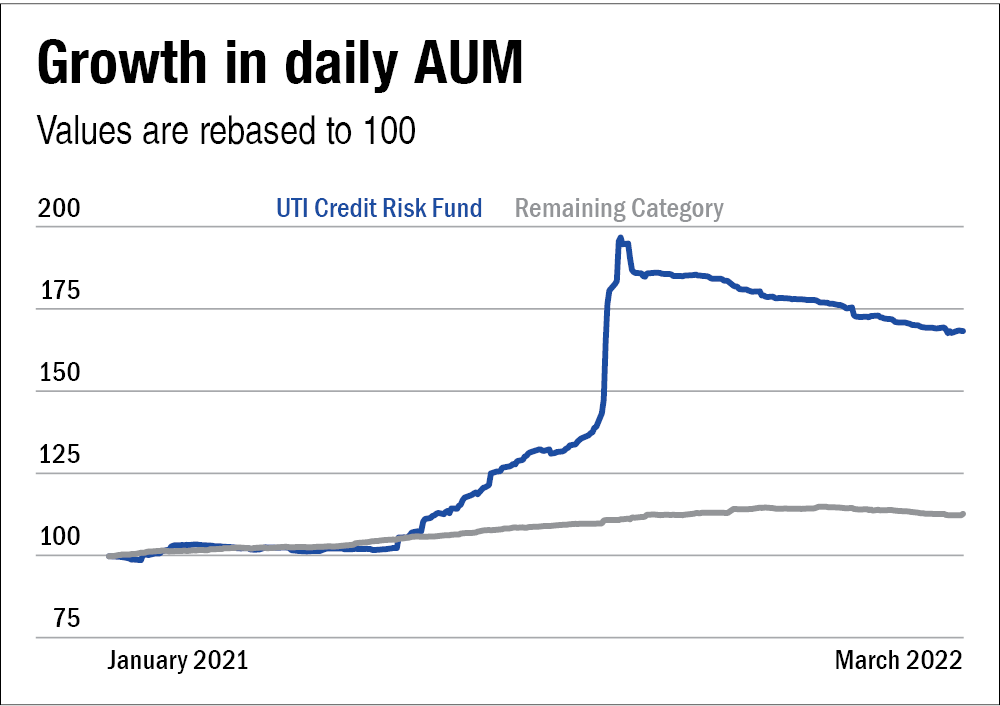

Now, this is not a unique case. UTI Credit Risk Fund, which had taken massive write-offs of DHFL bonds in mid-2019, was supposed to receive a partial recovery from these bonds in late-2021 as part of DHFL's resolution plan. And this information was in the public domain in advance. Subsequently, we noticed a substantial rise in the fund's AUM vis-à-vis the rest of the category ahead of the recovery, suggesting opportunistic investors may have entered to make short-term gains. Notably, the steady fall in AUM post the recovery is suggestive of a few investors exiting post participating in the gains.

But hopefully, such situations can be averted going forward since most fund companies have now enabled side-pocketing provisions in their fixed income funds. Therefore, if a bond in their portfolio goes bad, it can be segregated from the main portfolio. If there is any recovery, that amount will be paid to those who were investors at the time of segregation.

Takeaway for investors

From investors' standpoint, the key takeaway is to avoid investing blindly in the fund which shows the best returns. Given this sharp up movement in NAV, it is likely that BOI AXA Credit Risk Fund will remain the top performer in its category for a long time from here on. But investors need to scratch the surface and understand the underlying reasons driving those returns. In this case, looking at the rolling returns is sufficient to provide an insight into what may have transpired.

Ask Value Research ![]()