In our story, Tarsons Products IPO: Information analysis, we read about the key details of the IPO along with important information about the company. Here we will answer some questions about Tarsons Products and evaluate it on parameters like management, financials, valuations etc.

IPO questions

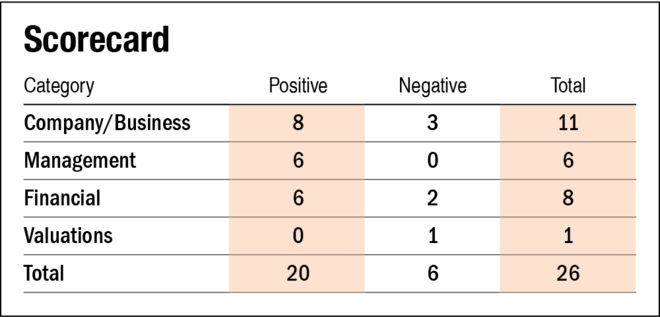

The company/business

1) Are the company's earnings before tax more than Rs 50 crore in the last 12 months?

Yes. In the last 12 months ending June 2021, the company's earnings before tax stood at Rs 116.4 crore.

2) Will the company be able to scale up its business?

Yes. The capacity of the company's injection moulding machines depends on the SKU manufactured, mould, raw material, number of cavities and other details. With 1,700 SKUs across 300 product categories and 63 machines and 645 moulds (as of June 30, 2021), the permutations and combinations are humongous. Moreover, it intends to increase its manufacturing capabilities by developing a new facility using the proceeds of the IPO. Through this new facility, it aims to enhance its production capacity in existing products and launch new products as well.

3) Does the company have recognisable brands truly valued by its customers?

Yes. In an industry historically dominated by global MNCs, Tarsons Products has won the trust of the scientists' community in India by offering differentiated, user-friendly, consistent quality, and cost-effective products, thereby providing an alternative for high-cost imports. In fact, some of its key products are identified by their brand names.

4) Does the company have high repeat customer usage?

Yes. The company uses a distribution-led model to sell its products. It has maintained long-term relationships with its top 10 distributors in, both, domestic and overseas markets.

5) Does the company have a credible moat?

Yes. The company's three-year (FY19-21) average gross and EBITDA margins were 73 per cent and 43.1 per cent, respectively. Tarsons Products' broad range of products and its ability to customize products allow its end customers to source most of their product categories from a single brand and enables it to expand its business from existing customers, as well as address a larger base of potential customers. Also, in an industry dominated by MNCs, the company has made its way to being among the top three labware manufacturing companies in India.

6) Is the company sufficiently robust to major regulatory or geopolitical risks?

Yes. The company is sufficiently robust to major regulatory or geopolitical risk.

7) Is the business of the company immune from easy replication by new players?

Yes. The labware industry presents significant entry barriers, including customer validation and approvals, expectations from customers for process innovation and requirement of adherence to high-quality standards and stringent specifications. In particular, end customers typically spend significant resources to engage with vendors who comply with quality standards.

8) Is the company's product able to withstand being easily substituted or outdated?

Yes. Currently, plastic labware is replacing many of the segments of glass labware. However, if in the future, environmental concerns regarding the use of plastic increase, then the company's products might be substituted.

9) Are the customers of the company devoid of significant bargaining power?

No. Though Tarsons Products often includes pricing and volume incentives in its contracts, its end customers are generally not obligated to purchase any fixed quantities of products, and they may stop placing orders with its distributors at any time. In addition, it may not be able to repeat its supply arrangements with its end customers on favourable pricing terms if its competitors reduce their prices in order to procure business, or if a customer is insistent that it lower the price charged for a product in order to procure repeat purchase by the end customer.

10) Are the suppliers of the company devoid of significant bargaining power?

No. The key raw materials include polypropylene, polystyrene, high-density polyethylene, low-density polyethylene and other materials. The company imports more than 75 per cent of its raw materials and purchases specialized medical grades of these plastic resins. Even though the prices of these high-grade resins (despite being a crude derivate) are not as volatile as the crude price and are generally passed on down the value chain, the company is a price taker.

11) Is the level of competition the company faces relatively low?

No. The Indian demand is predominantly catered to by a mix of domestic and MNC suppliers. Customisation of products to suit individual customer requirements, timely deliveries and strong relationships with channel partners form the core competencies of the companies to increase their market share.

Management

12) Do any of the company's founders still hold at least a 5 per cent stake in the company? Or do promoters hold more than a 25 per cent stake in the company?

Yes. Post-IPO, the promoter and promoter group will hold about a 47.3 per cent stake in the company. Moreover, another group company (Clear Vision Investment Holdings) will hold about 23.4 per cent stake in the company.

13) Do the top three managers have more than 15 years of combined leadership at the company?

Yes. Chairman and MD Sanjive Sehgal (also the promoter) has been associated with the company since its incorporation in 1983.

14) Is the management trustworthy? Is it transparent in its disclosures, which are consistent with SEBI guidelines?

Yes, we have no reason to believe otherwise.

15) Is the company free of litigation in court or with the regulator that casts doubts on the management's intention?

Yes, the company is free from any material litigation.

16) Is the company's accounting policy stable?

Yes. As per the auditors' report, the accounting policy is stable. However, the statutory auditor has laid emphasis on the treatment of 8,013 equity shares of the company which the management has classified as equity. The auditor has mentioned that per Ind AS, it should be treated as a financial liability as the company has an unconditional obligation to buy back these equity shares.

17) Is the company free of promoter pledging of its shares?

Yes. The company's shares are free of any pledging.

Financials

18) Did the company generate a current and three-year average return on equity of more than 15 per cent and return on capital employed of more than 18 per cent?

Yes, the company managed to generate a three-year (FY19-21) average return on equity of 29.7 per cent and a return on capital employed of 31.5 per cent. For FY21 the company generated a return on equity of 31.2 per cent and a return on capital employed of 34.5 per cent.

19) Was the company's operating cash flow positive during the last three years?

Yes, the company has reported positive operating cash flow during the last three years.

20) Did the company increase its revenue by 10 per cent CAGR in the last three years?

Yes. The company's revenues increased from Rs 178.7 crore in FY19 to Rs 228.9 crore in FY21 at a CAGR of 13.2 per cent.

21) Is the company's net debt-to-equity ratio less than one, or is its interest-coverage ratio more than two?

Yes. The company's net debt-to-equity ratio stood at 0.22 as of September 30, 2021, and its interest-coverage ratio stood at 40.1.

22) Is the company free from reliance on huge working capital for day-to-day affairs?

No, the company has a working capital cycle of 135 days for FY21. While the working capital cycle has decreased from 182 days in FY19 to 135 in FY21, any sudden changes in the debtor or creditor situation may harm the company's day-to-day needs.

23) Can the company run its business without relying on external funding in the next three years?

Yes, the company has planned to utilise its proceeds from IPO for repayment of borrowings and capital expenditure. It also makes adequate profits to self-sustain for the next three years.

24) Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

No. Even though it decreased by 34 per cent from Rs 45.8 crore in FY19 to Rs 30.2 crore in FY21, it has reported Rs 52.4 crore as of June 2021, an increase of 73.7 per cent.

25) Is the company free from meaningful contingent liabilities?

Yes, the company does not have any contingent liabilities.

Stock/valuations

26) Does the stock offer an operating-earnings yield of more than 8 per cent on its enterprise value?

No, the stock will only offer an operating-earnings yield of 3.3 per cent on its enterprise value.

27) Is the stock's price-to-earnings less than its peers' median level?

Not applicable. There are not any listed peers in a similar line of business. Post issue the company will trade at a P/E of 40.6.

28) Is the stock's price-to-book value less than its peers' average level?

Not applicable. There are not any listed peers in a similar line of business. Post issue the company will trade at a P/B of 8.4 times.

Also read about Tarsons Products IPO: Information analysis to learn about key IPO details and important company information.

Disclaimer: The authors may be an applicant in this Initial Public Offering.

Ask Value Research ![]()