Banks borrow money in the form of deposits and then lend it. The difference between borrowing and lending rates earns banks a spread or a margin. Primarily, banks have two types of deposits - term and non-term deposits. The fixed deposit is an example of a term deposit wherein the bank promises a certain interest rate for a certain period of time. On the other hand, non-term deposits refer to the money lying in the current or savings accounts and earns zero or small interest to the depositor. The CASA (current/savings account deposits to total deposits) ratio is an important analytical parameter for banks. The higher this ratio, the lower the bank's borrowing cost is. And lower borrowing costs help the bank earn better margins.

The CASA Winners

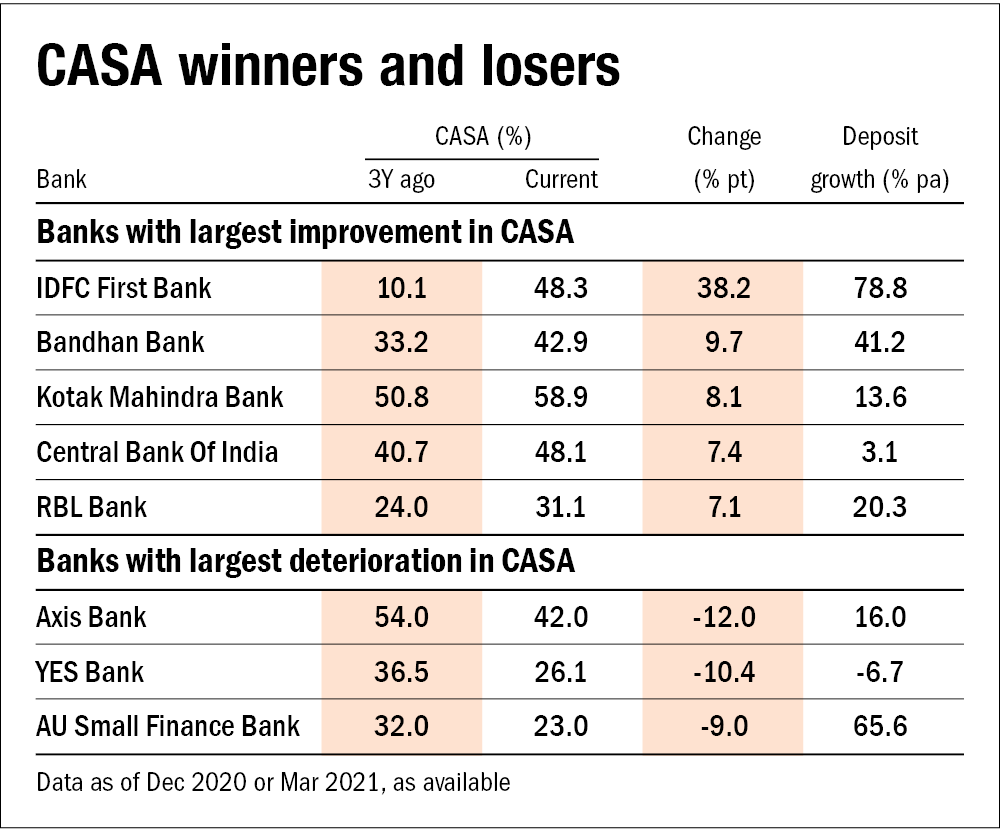

We analysed the listed banks and zeroed in on the ones that have reported an increase in their CASA ratio over the last three years, while expanding their deposit base. IDFC First Bank has emerged as the winner, as it managed to increase its CASA ratio from 10.1 per cent in December 2017 to 48.3 per cent in December 2020. While it was able to show improvement in CASA in every quarter, its deposits grew by 78.8 per cent YoY. Likewise, Bandhan Bank managed to increase its CASA from 33.2 per cent in December 2017 to 42.9 per cent in December 2020, while expanding its deposit base by 41.2 per cent YoY during the same period.

In addition to undertaking measures like opening branches and incorporating salaried accounts, banks also offer higher interest rates on savings accounts to boost their CASA. IDFC First was able to achieve this feat by offering higher interest rates on its savings accounts (6-7 per cent). Although an increase in CASA in such cases does not lead to low borrowing costs immediately as the bank attracts savings by offering higher interest rates. A subsequent decline in the interest rates of savings accounts, coupled with the sticky nature of account holders, can later translate into better spreads.

Consistent CASA

HDFC Bank has maintained a relatively high CASA of 46 per cent as of March 2021 (as compared to 43.5 per cent as of March 2018), while expanding its deposit base by 19.2 per cent YoY. The maintenance of high CASA is the reflection of the bank's service quality, which has resulted in customer stickiness.

The CASA dud

Over the last three years, Axis Bank has seen the maximum erosion in CASA but its deposit growth is in double digit. Next comes YES Bank, which suffered because of its exposure to bad assets. The falling confidence of depositors in the bank led to a decrease of CASA from 38 per cent in December 2017 to 26.1 per cent in March 2021. The bank was saved through capital infusion by other banks and saw an overhaul of its management and the board.

Ask Value Research ![]()