A diversified manufacturing company, Craftsman Automation primarily operates in the auto-ancillary sector. Under its largest division, Automotive-Powertrain, the company produces components like cylinder blocks, camshafts, cylinder heads, bearing caps, etc. This division, which contributed 48 per cent to the company's topline in FY20, supplies these parts to original equipment manufacturers (OEMs) operating in the non-passenger vehicle (PV) sector (tractors, heavy commercial vehicles, off-highway vehicles, etc.) such as Ashok Leyland, JCB India, Daimler India, Escorts, etc. Its second division, Automotive-Aluminium Products, manufactures items like crankcases, gearbox housings, structural parts, cylinder blocks, etc., by using various kinds of die-casting methods (high pressure, low pressure, etc.). This division's products are used in two-wheelers, commercial vehicles and passenger vehicles by leading OEMs, such as Royal Enfield, TVS, etc. This division contributed 17 per cent to the company's FY20 topline. The third division, Industrial and Engineering, undertakes contract manufacturing and high-end sub-assembly for a variety of items, such as gearboxes, milling machines, etc. This division also offers storage solutions to FMCG, e-commerce and pharma players by producing pallets, shelves and automated storage and retrieval systems. It contributed 35 per cent to the company's FY20 topline and is the only segment that has consistently grown in the last three years.

This Coimbatore-based company was founded in 1986 by Mr Srinivasan Ravi, who continues to be the promoter. It has 12 manufacturing facilities across seven cities, with the Coimbatore facility being the major one. Although the company mainly focuses on domestic sales, it also derives a portion of its sales (around 10 per cent) from exports.

Strengths

- Strong position: The company is the largest manufacturer of cylinder blocks and cylinder heads in the construction equipment industry and intermediate, medium & heavy commercial vehicles segments. It is also one of the top four-component manufacturers of cylinder blocks for the tractor segment and has long-term relationships with major OEMs.

- Completion of CAPEX cycle: The company has already incurred a substantial portion of the required capital expenditure for all of its three segments and expects to incur only incremental maintenance-related expenses, going forwards.

- Strong EBITDA margins: The company has one of the highest EBITDA margins in the industry, which the management attributes to its business model. Its business model involves carrying a lesser amount of inventory on its balance sheet than peers.

- High growth in the storage-solutions segment: The company's storage-solution business grew at a CAGR of 204 per cent during the last financial years and contributed around 6 per cent to the company's topline for the nine months during the current fiscal. The storage-solutions industry has grown at a CAGR of 14-16 per cent during the last five financial years and is expected to grow at a CAGR of 19-21 per cent over the next three years. This segment is also very profitable, with an EBITDA margin of around 30 per cent.

Risks & Concerns

- Technological obsolescence: Except for the storage-solutions segment, the company predominantly manufactures components for fossil fuel-based engines (petrol, diesel, etc). As electric vehicles (EVs), which don't rely on traditional Internal Combustion Engines, is gaining more popularity, the company's products risk becoming obsolete. The switch to EVs is not expected to affect the company in the near term, EV technology is expected to gain traction in the non-PV segment (in which the company operates) only after dominating the PV space. But the threat of a faster adoption cannot be ruled out.

- The current downtrend in the auto sector: The sector in which the company operates is cyclical in nature and is currently going through a rough patch. Even before the COVID-19 pandemic, the sector faced headwinds in the forms of BS-VI emission norms, an increase in costs due to longer duration insurance policies and credit problems. Also, the sector was severely affected by COVID-19 and it remains to be seen when the sector will be able to recover. This has clearly impacted the company and its effect is evident in its declining revenue in the last three years.

- High dependence on a few customers: Given the nature of the business, the company has a high reliance on a small number of customers. The top four customers accounted for 43 per cent of the company's revenue in the current fiscal and the top ten customers accounted for nearly 60 per cent. The resulting lower bargaining power is also, perhaps, evidenced by increasing receivables, which shot up from 11 per cent of its revenue in FY19 to 21 per cent in the current fiscal.

IPO Questions

The company/business

1. Are the company's earnings before tax more than Rs 50 crore in the last twelve months?

Yes. The Profit before tax for the last nine months (from April 2020 to December 2020) itself was Rs 76 crore.

2. Will the company be able to scale up its business?

Yes. The capacity utilisation rates at various factories of the company are between 70 per cent and 80 per cent. The company has incurred capital expenditure to the tune of 800 crore in the last four years and is now in a position to cater to the growing demand if it materialises. Also, the company could benefit from the growing demand from the storage-solutions segment.

3. Does the company have recognisable brand/s, truly valued by its customers?

No. The company is involved in manufacturing automobile parts and is predominantly in the B2B space. It has three brands, namely V-Store, Carl Stahl Craftsman and Craftsman Marine, but these are not very significant.

4. Does the company have high repeat customer usage?

Yes. The company has strong relationships with its customers and therefore, has a high repeat customer usage.

5. Does the company have a credible moat?

No. The company does not have any patents or any other unique knowledge in the manufacturing segment. It is also not a unique supplier to any of its customers.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

Yes. But that's because the company operates in a very non-controversial space where the probability of any major geopolitical risks is minimal.

7. Is the business of the company immune from easy replication by new players?

No. The company is not the sole supplier to any of its customers and does not claim to have any unique know-how.

8. Is the company's product able to withstand being easily substituted or outdated?

No. The company is an auto-component manufacturer, which specifically caters to the needs of Internal Combustion Engine manufacturers. Electric vehicle technology, as and when it becomes prominent, is expected to affect the company. Besides, the company's products are not unique and are already manufactured by other players as well.

9. Are the customers of the company devoid of significant bargaining power?

No. The top four customers of the company account for around 43 per cent of its revenues and the top ten customers account for 60 per cent of its revenues. Since they are established manufacturers, the company has no other choice but to sell to them. The lack of bargaining power is also evident from the fact that receivables shot up from 11 per cent of its revenue in FY19 to 21 per cent in the current fiscal.

10. Are the suppliers of the company devoid of significant bargaining power?

Yes. Costs of raw materials have been around 40 per cent of the company's revenue in the last few years and the company sources its raw materials from multiple suppliers.

11. Is the level of competition the company faces relatively low?

No. Manufacturing is, in general, not a very high-margin business. The presence of multiple players in the industry also makes it very competitive.

Management

12. Do any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than 25 per cent stake in the company?

Yes. The promoters will continue to hold around 60 per cent stake in the company, post the IPO.

13. Do the top three managers have more than 15 years of combined leadership at the company?

Yes. The founder-promoter, who is the current managing director of the company, has been associated with the company for the last 35 years.

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with SEBI guidelines?

Yes. We have no reason to believe otherwise.

15. Is the company free of any litigation in court or with the regulator that casts doubts on the intention of the management?

Yes. the company, as well as the management, is free from any material litigation that casts any doubt on the intention of the management.

16. Is the company's accounting policy stable?

Yes. The company has been following a stable accounting policy.

17. Is the company free of promoter pledging of its shares?

Yes. None of the shares of the promoter are pledged.

Financials

18. Did the company generate the current and three-year average return on equity (ROE) of more than 15 per cent and return on capital employed (ROCE) of more than 18 per cent?

No. Although the average three-year (till FY20) ROCE was 15.5 per cent, the ROE for the same period was 9.2 per cent.

19. Was the company's operating cash flow positive during the previous three years?

Yes. The cash flow from operations for FY18, FY19 and FY20 was 282.7 crore, 360 crore and 305.37 crore, respectively.

20. Did the company increase its revenue by 10 per cent CAGR in the last three years?

No. The company's revenue declined from 1,522.86 crore in FY2018 to 1501 crore in FY19-20.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest-coverage ratio more than 2?

No. Although the company's interest-coverage ratio was 3.8, its debt-to-equity ratio was 1.15 as of December 2020.

22. Is the company free from reliance on huge working capital for day-to-day affairs?

Yes. The company does not need a large amount of working capital for its day-to-day affairs.

23. Can the company run its business without relying on external funding in the next three years?

Yes. The bulk of the CAPEX required has already been incurred by the company in the last three to four years. The overall capacity utilisation of the company is between 70 per cent and 80 per cent and the management is expecting to ramp up utilisation, without incurring any new CAPEX in the near future.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

Yes. The company's short-term borrowings have declined from Rs 272 crore in FY 2018 to 156.7 crore as of December 2020. Given that 80 per cent of the IPO proceeds are slated to be used for debt reduction, the outstanding borrowings should reduce further.

25. Is the company free from meaningful contingent liabilities?

Yes. The company does not have any meaningful contingent liabilities. But it has disclosed capital commitments worth Rs 86.5 crore as of December 31, 2020.

Valuations

26. Does the stock offer an operating-earnings yield of more than 8 per cent on its enterprise value?

Yes. Based on the post-IPO enterprise value of Rs 3787 crore and annualised operating earnings of Rs 392 crore for FY21, the yield would be around 10.3 per cent.

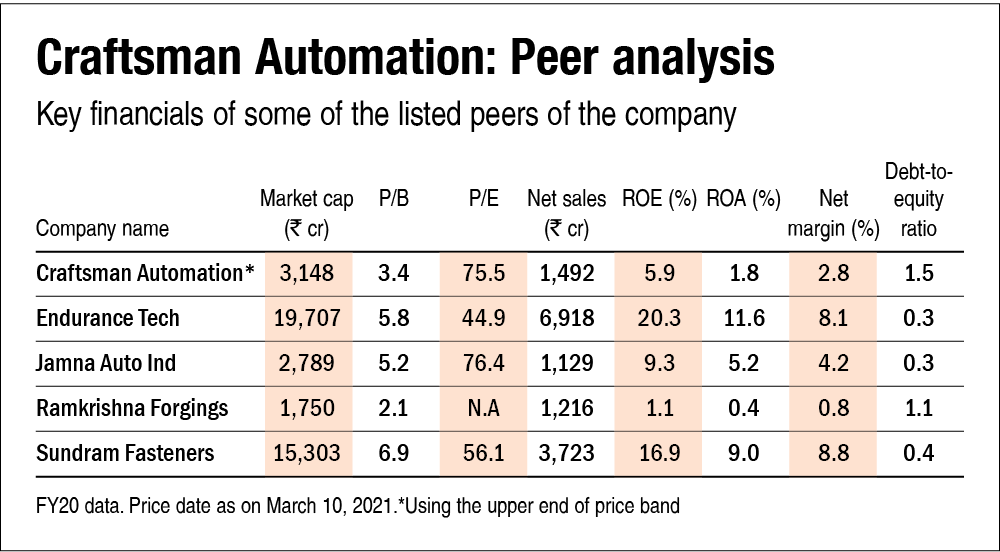

27. Is the stock's price-to-earnings less than its peers' median level?

No. As per FY20 data, the stock would trade at a P/E of around 75, which is higher than its peers' median P/E of 56.

28. Is the stock's price-to-book value less than its peers' average level?

Yes. At the upper end of its price band, the stock's P/B ratio on a post-IPO basis is 3.4, which is lower than its peers' average P/B of 5.0.

Disclaimer: The author may be an applicant in this Initial Public Offering.

Ask Value Research ![]()