Interest-rate risk, also known as the duration risk, is an important factor in debt-fund investing. This is the risk of a sudden drop in the NAV of a debt fund owing to a rise in interest rates. However, a roll-down maturity portfolio can help you reduce this risk. There are many debt funds that deploy it. But before you decide to invest in them, let's first understand what this strategy is and what its pros and cons are.

What is the roll-down strategy?

When a fund manager creates a portfolio and holds underlying securities till maturity, the fund is said to be following a roll-down maturity structure. Effectively, here the maturity period comes down over a period of time. So, the fund sets maturity at the beginning and lets it roll down to zero. Since maturity reduces over a period of time, the interest-rate risk also reduces. Whenever the fund sees inflows and outflows, it buys bonds with a tenure similar to the residual maturity of the fund. As the original maturity remains fixed, the fund is able to provide a predictable return profile.

This is not a new strategy in the mutual fund industry. Fixed maturity plans (FMPs) are based on this premise only. The fund manager here buys and holds securities whose duration is similar to the term of the fund. Therefore, in a five-year FMP, the fund manager buys bonds with a maturity of five years. FMPs are designed like fixed deposits, where investors can take their money out only at maturity.

Earlier, there was a slew of FMP launches. However, now people shy away from FMPs. In the aftermath of the IL&FS crisis, the long-established principles of risk management through diversification were violated by some AMCs in their FMPs. But many fund companies have started pursuing a similar investment strategy in their open-end funds, which can be visualised as open-end FMPs.

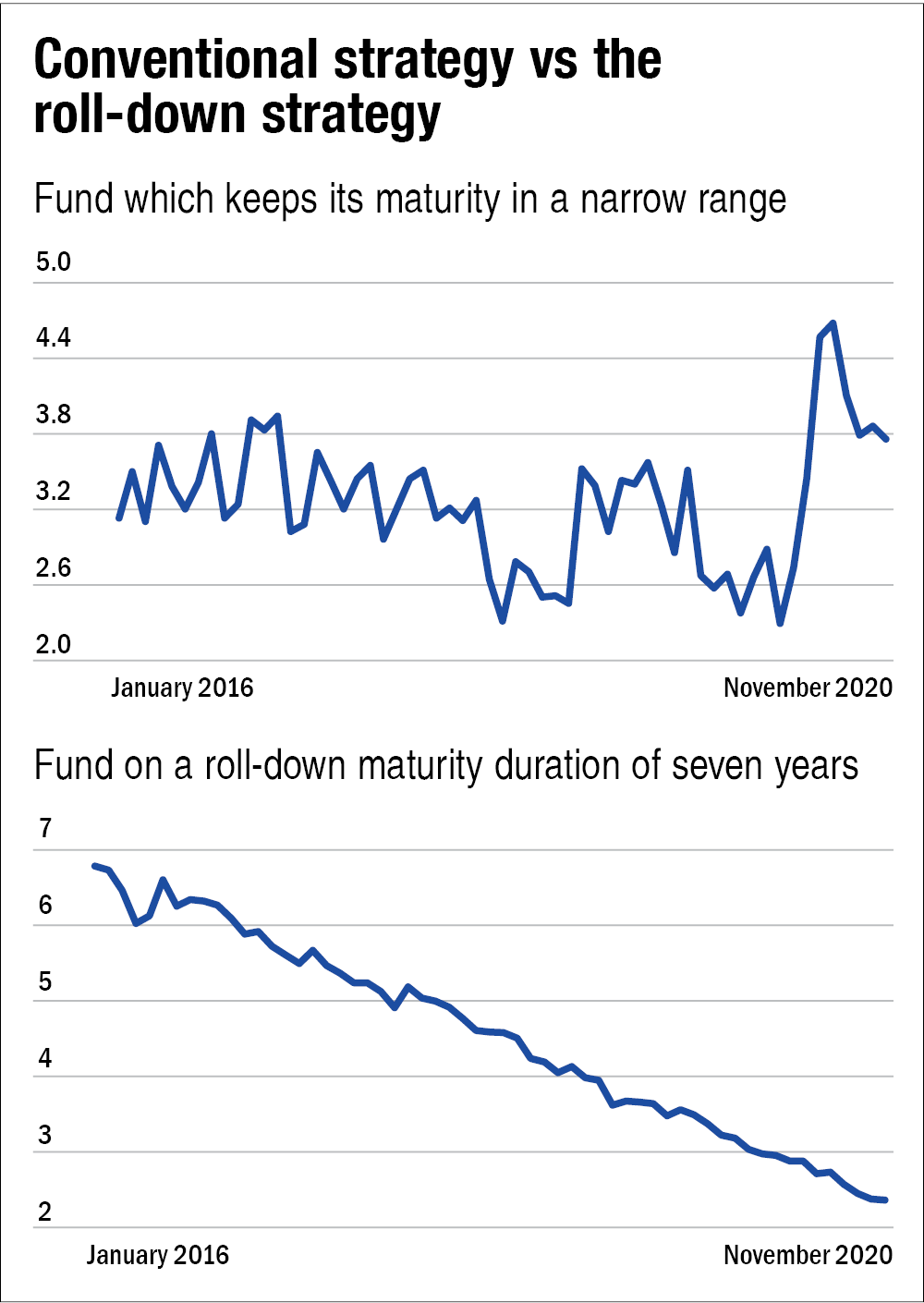

Conventional style vs the roll-down style

Consider two kinds of funds, one that keeps its maturity in a relatively narrow range of, say, two to five years, while the other sets a roll-down duration at let's say seven years (look at the graphs titled 'Conventional strategy vs the roll-down strategy').

In the case of a more conventional fund, the fund manager, in a steady state, keeps buying and selling bonds while keeping the portfolio maturity within this defined range. Based on his/her views on interest rates, the fund manager may buy longer-dated or short-dated bonds. However, the average maturity will oscillate within the band of two to five years. On the contrary, the fund manager following the roll-down strategy will let the portfolio gradually roll down over the set duration of seven years to zero. So, this is the basic difference between the two strategies. Now comes the most important question - what are the implications of the roll-down strategy for an investor?

Advantages and the flip side

Open-end funds running portfolios on the roll-down strategy can act as an alternative to FMPs. If an investor holds a debt fund following the roll-down strategy till maturity, then the intermittent volatility owing to interest rates would reduce proportionately. Further, the investor also gets an additional benefit of liquidity because of the open-end structure.

According to Saurabh Bhatia, Head - Fixed Income at DSP Investment Managers, a fixed-income investor should choose to see through the resets to get the benefit across rate cycles. "As and when the fund gets closer to maturity, the fund manager would initiate deployment for the next phase of roll-down. For an investor who chooses to stay along the full roll-down of the fund, predictability factor for every investment is very close to the yield of deployment/day-end valuation of the respective security," he says.

But there are some limitations as well. In an FMP, an investor can be sure about the returns that he/she will get at the end of the period, provided there are no blow-ups in the portfolio. However, in the case of open-end roll-down strategy, large intermittent inflows and outflows may alter the yields to some extent. This is because the fund manager will have to create liquidity at prevailing yields to deploy the fresh inflows or manage the outflows, thereby impacting the predictability factor.

If you invest in a fund following the roll-down strategy at a time when yields on offer are fairly low (such as the current scenario), that may not be prudent. Further, entering a fund having a longer-duration roll-down maturity at a time of lower yields may also not be wise. Bhatia says that initiating a greater than three-year roll-down strategy at current yields does not provide a favourable risk-reward. "One-year roll-down funds or funds bearing a residual roll-down of about 12-18 months may prove to be more beneficial as they will realign with the change (reversal) in the interest rate cycle," adds Bhatia.

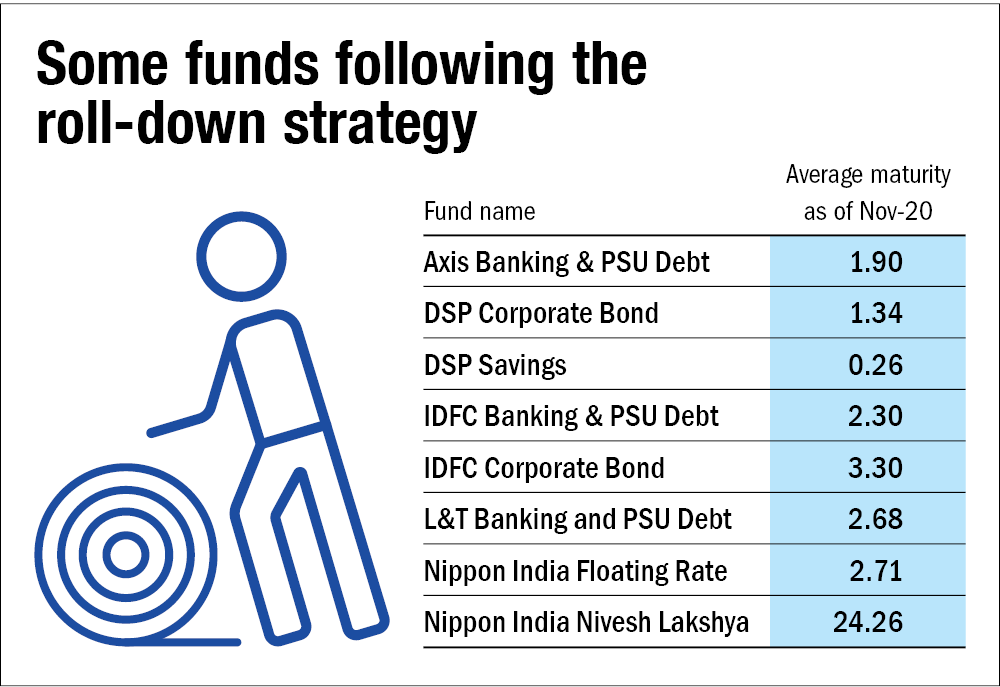

Funds using the roll-down strategy

Apart from the Bharat Bond ETFs, these days, several debt funds, particularly banking and PSU and corporate bond funds, seem to be following the roll-down strategy. While this strategy is followed by some funds, it is not really a part of the mandate. The table 'Some funds following the roll-down strategy' highlights some funds that have mentioned the roll-down strategy as their current investment style in their product brochures/literature. However, this is not an exhaustive list.

For whom are these suitable?

Fixed-income investors who have a very defined investing time frame can consider such funds. One should make sure to choose a fund whose maturity profile matches with one's investment horizon. This contains the intermittent interest-rate risk to a large extent. Having said that, if you opt for the roll-down strategy at this time, it may not be very prudent to go for the one having a very long term.

For investors who don't have a specific time frame, someone like a retiree, the steady fixed-income allocation may find funds that keep their duration in a narrow range of short to medium term, say three-five years, of more liking.

Ask Value Research ![]()