The Union budget for FY19 imposed a 10 per cent long-term capital-gains (LTCG) tax on realised equity gains over Rs 1 lakh in a financial year. Naturally, this tax didn't go down well with investors. Many investors have attributed the subsequent fall in the broader market to the LTCG tax.

However, whenever a policy measure causes disruption, newer ways to get around it also evolve shortly. Since the introduction of the LTCG tax, some advisors have been beating the drum of tax-harvesting as a means of circumventing the LTCG tax.

In this story, we tell you what this practice is and whether it's useful.

What is tax-harvesting?

Tax-harvesting revolves around using the tax-free window of Rs 1 lakh to lower your overall LTCG tax. What you are essentially advised to do is to redeem, and simultaneously re-invest, a portion of your equity investments which are over one year old, and hence are long-term in nature, to the extent that the gains do not exceed Rs 1 lakh in a given financial year. By doing so, your net investment remains unchanged, but you shield Rs 1 lakh worth of long-term capital gains from the taxman each year. Thus, as the argument goes, when you finally sell all your investments, your overall tax liability will be lower.

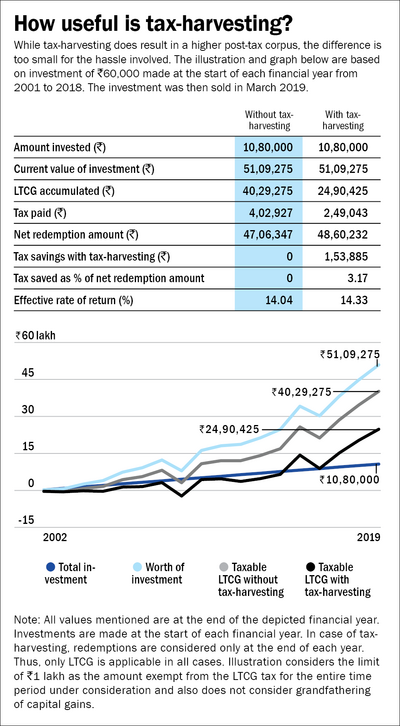

But how does tax-harvesting work in practice? Consider an investor who has invested Rs 5,000/month in a Nifty 50 TRI index fund from March 2001 until March 2018. For ease of understanding, let's assume that for any financial year, the entire investment was done only once in March, at Rs 60,000/year.

Assuming that the current tax rules have been in place all this while, let's see the tax outgo for the investor in two scenarios: (1) the investor simply keeps investing through this period and does nothing to harvest tax and (2) the investor actively deploys the tax-harvesting strategy every year.

The illustration depicts the results in both the scenarios if the investor were to finally sell all his investments in March 2019. As you can see, the realised proceeds are about Rs 1,53,885 (Rs 48,60,232 minus Rs 47,06,347) more when the tax-harvesting strategy is used. While that may seem substantial, when you adjust for the holding period, the difference in the internal rates of returns for the two scenarios is about 0.29 per cent, an insignificant number.

Why tax-harvesting has limited benefits

This is effectively because regardless of the amount invested and the growth in investment value, the savings with tax-harvesting would always be restricted. In any given year, the maximum tax that one can save is limited to 10 per cent (the LTCG tax rate) of Rs 1,00,000 (the exempt limit from the LTCG tax), i.e., Rs 10,000. Effectively, the total gains would be limited to this value multiplied by the total duration of your investment. Over a period of 25 years, for instance, the maximum possible savings would always be lower than or equal to Rs 2.5 lakh (Rs 10,000 multiplied by 25).

Other problems

The tax-harvesting strategy has other complications, too. To maintain continuity of investments, you will need to reinvest in equity funds as soon as you redeem the older units for tax-harvesting. This will require you to maintain a fat balance in your bank account in order to make the buy transaction. After all, the redemption proceeds from the selling of units will be credited to your bank account only on the third day after the transaction. If an investor waits for these to be available for reinvestment, it could cause a significant opportunity loss should the NAV jump in the interim. Apart from this, you also have to undertake the periodic exercise of selling part of your investments in each financial year. This will likely prove to be a recurring hassle for many investors.

Hence, we don't think the gains from tax-harvesting are significant enough to justify the effort. For a small investor with humble contributions as the one in our example, the extra earning is just about 3.17 per cent of the total accumulation, that too over a significantly long period. For a bigger investor, the savings will be even smaller, rendering the whole affair pointless.

This article was originally published on December 23, 2019.

Ask Value Research ![]()