Aditya Roy/AI-Generated Image

Aditya Roy/AI-Generated Image

Summary: SIFs promise to sit neatly between mutual funds and PMS. But what problem are they really solving, and who are they meant for? This piece unpacks where SIFs fit, how they behave and why patience may matter more than excitement right now.

“Have you heard of SIFs?”

I was halfway through my coffee when my friend Rohan dropped this into our WhatsApp group. The message lingered for a moment.

“Another fancy fund category?” someone replied.

Rohan was quick to clarify. “Specialised investment funds. The Securities and Exchange Board of India (SEBI) introduced it last year.”

That only deepened the curiosity. Mutual funds already come with no shortage of labels. Why add one more? And more importantly, what problem is this trying to solve?

To understand SIFs, it helps to step back and look at where traditional mutual funds began to feel constrained and why investors and fund managers alike were asking for something in between.

Why SEBI felt the need for SIFs

Mutual funds in India were designed with a clear philosophy: broad participation, strong safeguards and well-defined limits on risk.

For most investors, that model works exactly as intended. You get diversification, transparency and simplicity. But over time, a gap became evident.

Fund managers found it difficult to run certain strategies within existing categories. Investors who wanted something more nuanced faced a stark choice. Either stay within plain-vanilla mutual funds or move straight to portfolio management services (PMS) or alternative investment funds (AIF), both of which come with high minimum investments (Rs 50 lakh to Rs 1 crore) and fewer guardrails.

“There was no middle ground,” Rohan explained later. “You either stayed simple or jumped straight into expensive complex territory.”

SIFs are SEBI’s attempt to bridge that gap.

The regulator notified the specialised investment fund framework in February 2025, with the regime coming into effect from April 1, 2025. The aim was not to dilute investor protection, but to allow more flexibility within a regulated structure.

So what exactly is an SIF?

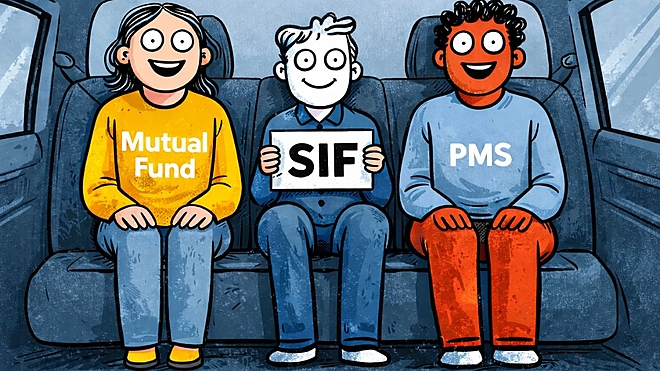

A specialised investment fund is a SEBI-regulated pooled investment product offered by fund houses, created as a distinct bucket between traditional mutual funds and PMS.

SIFs retain the discipline of the mutual fund ecosystem, including regulatory oversight and disclosure norms. But unlike regular mutual fund schemes, they are not forced into rigid category definitions.

This allows fund managers to run more focused portfolios and use strategies that do not fit neatly into existing mutual fund buckets.

“And this is where long-short strategies enter the picture,” Rohan said, anticipating my next question.

In a standard equity mutual fund, a manager can only express a positive view. If they like a stock, they buy it. If they don’t, they simply avoid it.

SIFs allow more precision.

Some SIF strategies can take long positions in stocks they expect to outperform and short exposure, typically through derivatives, in stocks they believe are overvalued or vulnerable. These are commonly referred to as long-short strategies.

The objective is not to predict whether markets will rise or fall, but to benefit from relative performance between securities.

How long-short SIFs actually behave

This is where many investors get tripped up.

A long-short SIF does not behave like a typical equity fund. In strong bull markets, it may even underperform headline indices.

“That sounds counterintuitive,” someone in the group said when Rohan explained it.

But the trade-off is deliberate.

By combining long and short exposures, these strategies aim to reduce reliance on market direction. The intent of some of these schemes is to limit drawdowns during market corrections, reduce volatility during sideways phases and generate returns through stock selection rather than broad market momentum.

Of course, intent does not guarantee outcome.

Performance depends heavily on execution. If a manager gets both the long calls and the short calls wrong, losses can add up quickly. Unlike traditional equity funds, there is no automatic cushion from rising markets.

SEBI has recognised this risk and built in safeguards. For instance, derivative exposure under the SIF framework is capped, limiting the scope for excessive leverage.

“These funds aren’t designed to look impressive in every market phase,” Rohan said. “They’re designed to behave differently.”

Where SIFs sit in an investor’s portfolio

SIFs offer more freedom than traditional mutual funds but retain regulatory discipline. The minimum investment threshold is clearly defined at Rs 10 lakh at the PAN level.

“Should people replace their equity funds with SIFs?” I asked Rohan.

“For most people, no,” he replied.

That framing matters. SIFs are not designed to replace core equity or hybrid funds. For most investors, they are better treated as satellite allocations, if at all.

The bigger picture

SIFs are no longer just a concept on paper. A few strategies have already been launched and have been running for a few months.

But a few months is not a track record.

Specialised strategies, especially those using long-short approaches, reveal their strengths and weaknesses only over full market cycles. Early performance, whether good or bad, says very little about how these funds will behave when conditions change.

From our perspective, this is not the moment to rush in.

Let these funds run longer. Let them navigate different market phases. Let managers show that they can execute consistently, not just explain convincingly.

Until then, tested mutual funds remain the stronger foundation for most investors. They are simpler, better understood and backed by long track records across bull and bear markets alike.

SIFs may eventually earn a place in portfolios. But that place has to be earned, not assumed.

Until then, the smartest move may be the hardest one in investing: doing nothing.

If you’re looking to build a solid, time-tested mutual fund portfolio, Value Research Fund Advisor can help. It gives you expert-guided fund recommendations and portfolio support so you can act with clarity, not noise.

This article was originally published on January 30, 2026.

Ask Value Research ![]()